Sterling rebounds strongly after German Chancellor Angela Merkel expressed her optimism that Irish border backstop solution could be achieved before Brexit date. The Pound is currently the strongest one, followed by Canadian Dollar. On the other hand, cautious risk sentiments keep Australian and New Zealand Dollar as the weakest. Euro is mixed as better than expected PMIs didn’t offer optimism on economic outlook.

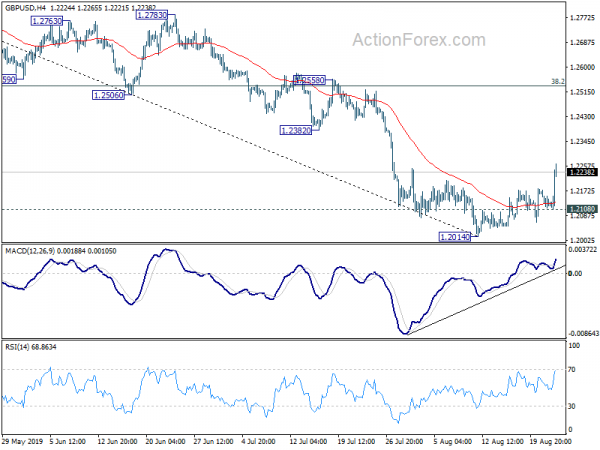

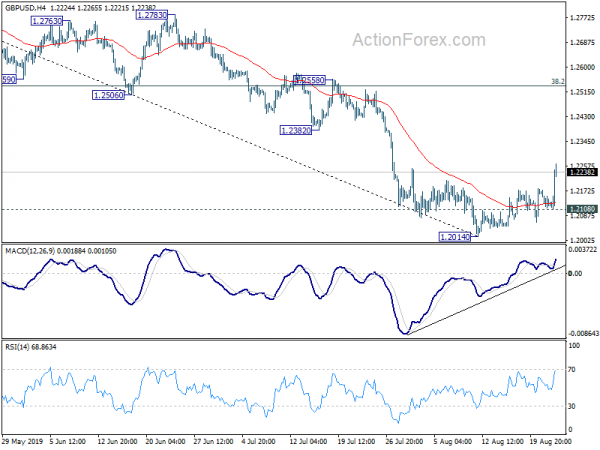

Technically, GBP/USD’s break of 1.2209 and GBP/JPY’s break of 130.06 suggests short term bottoming in both pairs. Stronger rebound should be seen in near term. But these rebounds are viewed as extended corrective move. We’ll assess the structure to confirm this view later. Similarly, EUR/GBP is set to enter key near term support zone of 0.8891/9051. We’d look for bottoming there.

In US, DOW opened higher and is currently up more than 100 pts. In Europe, FTSE is down -0.83%. DAX is up 0.18%. CAC is down -0.19%. German 10-year yield is up 0.036 at -0.634. Earlier in Asia, Nikkei rose 0.05%. Hong Kong HSI dropped -0.84%. China Shanghai SSE rose 0.11%. Singapore Strait Times rose 0.17%. Japan 10-year JGB yield is down -0.0002 at -0.24.

German Merkel said Irish backstop solution could be achieved by Oct 31

Sterling is given a lift after German Chancellor Angela Merkel hinted that the Irish border solution could be achieved within 30 days to avoid no-deal Brexit.

Merkel denied that she’s set a 30-day deadline for UK Prime Minister Boris Johnson to find a solution to remove the Irish backstop from the withdrawal agreement.

Though, she clarified that what one can achieve in three or two years can also be achieved in 30 days. Better said, one must say that one can also achieve it by October 31.”

US initial jobless claims dropped to 209k, vs exp. 217k

US initial jobless claims dropped -12k to 209k in the week ending August 17, below expectation of 217k. Four-week moving average of initial claims rose 0.5k to 214.5k. Continuing claims dropped -54k to 1.674m in the week ending August 10. Four-week moving average of continuing claims dropped -0.75k to 1.697m.

Fed George: July’s rate cut wasn’t required, policy at equilibrium now

Kansas City Fed President Esther George, who dissented the rate cut at July FOMC meeting, repeated her stance that the rate cut “wasn’t required”. She told CNBC that “with this very low unemployment rate, with wages rising, with the inflation rate staying close to the Fed’s target, I think we’re in a good place relative to the mandates that we’re asked to achieve.”

Though, she admitted that risks are tilted to the downside. She noted, “as you look at global growth weakening and as you look at the amount of uncertainty associated with some of these trade issues, I think both of those are weighing on the outlook. Whether they spill over in a way that we see in the real economy is what I’m watching for.”

Separately, she told Bloomberg TV that “We’re at a sort of equilibrium right now and I’d be happy to leave rates here absent seeing either some weakness or some strengthening, some kind of upside risk that would cause me to think rates should be somewhere else.”

ECB accounts: Policy package more effective than a sequence of selective actions

Accounts of the July 24-25 ECB policy meeting showed that members “broadly supported the reintroduction of an easing bias” to the forward guidance. That came in light of “weakness of the economic outlook and the muted inflation developments”.

For further easing, “the view was expressed that the various options should be seen as a package, i.e. a combination of instruments with significant complementarities and synergies”. That’s because “experience had shown that a policy package – such as the combination of rate cuts and asset purchases – was more effective than a sequence of selective actions.”

Eurozone PMIs: Dynamics little changed, indicate 0.1-0.2% GDP growth in Q3

Eurozone PMI Manufacturing rose to 47.0 in August, up from 46.5 and beat expectation of 46.2. PMI |Services rose to 53.4, up from 53.2 and beat expectation of 53.0. PMI Composite rose to 51.8, up fro 51.5.

Andrew Harker, Associate Director at IHS Markit said: “The dynamics of the eurozone economy were little changed in August, with solid growth in services continuing to hold the wider economy’s head above water despite ongoing manufacturing decline. While the rate of overall expansion ticked up, we’re still looking at GDP only rising by between 0.1% and 0.2%, based on the PMI data for the third quarter so far.”

German PMIs: Two-speed economy, threat of GDP contraction in Q3 remains

Germany PMI Manufacturing rose slightly to 43.6 in August, up from 43.2 and beat expectation of 43.0. PMI Services dropped to 54.4, down from 54.5, but beat expectation of 54.0. It’s nevertheless a 7-month low. PMI Composite improved to 51.4, up from 50.9.

Phil Smith, Principal Economist at IHS Markit said: “Germany remains a two-speed economy, with ongoing growth of services just about compensating for the sustained weakness in manufacturing. Although improving slightly, the survey’s output data haven’t changed enough to dispel the threat of another slight contraction in GDP in the third quarter, especially given the deterioration in the forward-looking indicators.”

France PMI composite rose to 52.7, outperformance likely to continue in Q3

France PMI Manufacturing rose to 51.0 in August, up from 49.7 and beat expectation of 49.5, back in expansionary region. PMI Services rose to 53.3, up from 52.6 and beat expectation of 52.5. It’s also a 9-month high. PMI Composite Rose to 52.7, up from 51.9.

Eliot Kerr, Economist at IHS Markit said: “French private sector businesses posted another solid increase in output during August. Service sector expansion continued to surpass manufacturing growth, reflecting the broader trend seen across the eurozone in recent months. “However, in contrast to its peers, economic growth in France has remained solid and the latest set of PMI figures only add weight to the argument that this outperformance is likely to continue in the third quarter.”

Ιαπωνία Motegi: Τα κενά που πρέπει να καλυφθούν στις εμπορικές συνομιλίες των ΗΠΑ

Ο Ιάπωνας υπουργός Οικονομίας Toshimitsu Motegi συνάντησε χθες στην Ουάσιγκτον τον Εμπορικό Αντιπρόσωπο των ΗΠΑ Robert Lighthizer για το εμπόριο. Μετά τη συνάντηση, σημείωσε ότι οι συνομιλίες έχουν «περιοριστεί αρκετά», οι συζητήσεις «βαθαίνουν». Υπάρχουν όμως ακόμα «κενά» που πρέπει να καλυφθούν.

Ο Μοτέγκι είπε: «Τα ζητήματα που πρέπει να διευθετηθούν σε συνομιλίες σε υπουργικό επίπεδο έχουν περιοριστεί αρκετά… Συμφωνήσαμε να επιταχύνουμε τις συζητήσεις και να εργαστούμε για τα υπόλοιπα ζητήματα για την έγκαιρη επίτευξη αποτελεσμάτων… Οι συζητήσεις αναμφίβολα βαθαίνουν. Όμως υπάρχουν ακόμα κενά που πρέπει να καλυφθούν».

Οι συζητήσεις θα συνεχιστούν σήμερα μετά από συνομιλίες σε επίπεδο εργασίας μεταξύ των δύο πλευρών. Οι ομάδες στοχεύουν να θέσουν τις βάσεις για μια πιθανή συνάντηση μεταξύ του Ιάπωνα πρωθυπουργού Σίνζο Άμπε και του προέδρου των ΗΠΑ Ντόναλντ Τραμπ, που θα πραγματοποιηθεί στο περιθώριο της συνόδου κορυφής της G7 αυτό το Σαββατοκύριακο στη Γαλλία.

PMI της Ιαπωνίας: Πολλές υποσχέσεις, οι φόβοι έχουν μετριαστεί προς το παρόν

Ο Ιαπωνικός PMI Manufacturing αυξήθηκε 0.1 στο 49.5 τον Αύγουστο. Η PMI Services αυξήθηκε 1.6 στις 53.4. Το PMI Composite αυξήθηκε 1.1 στο 51.7.

Ο Joe Hayes, Economists της IHS Markit σημείωσε: «Τα προκαταρκτικά στοιχεία PMI του Αυγούστου δίνουν πολλές υπόσχεση ότι η σταθερή τάση ανάπτυξης που παρατηρείται στα αποτελέσματα του ΑΕΠ μέχρι στιγμής φέτος θα μπορούσε πράγματι να εκτείνεται στο τρίτο τρίμηνο, παρέχοντας έγκαιρη ώθηση πριν από το τέταρτο τρίμηνο, το οποίο είναι πιθανό να επηρεαστεί αρνητικά από τις συνέπειες της αύξησης του φόρου επί των πωλήσεων».

«Η κινητήρια δύναμη πίσω από αυτό παραμένει ο τομέας των υπηρεσιών, ο οποίος ενισχύεται από την ανθεκτική ζήτηση στην εγχώρια οικονομία. Τα flash στοιχεία έδειξαν ότι η δραστηριότητα των υπηρεσιών αυξάνεται με τον ταχύτερο ρυθμό σε σχεδόν δύο χρόνια τον Αύγουστο, καθησυχάζοντας τους φόβους, τουλάχιστον προς το παρόν, ότι οι ισχυροί εξωτερικοί αντίθετοι άνεμοι που γίνονται αισθητές εντός της μεταποίησης θα μπορούσαν να εξαπλωθούν σε άλλα μέρη της οικονομίας».

Επίσης από την Ιαπωνία, ο δείκτης δραστηριότητας όλης της βιομηχανίας μειώθηκε -0.8% τον Ιούνιο.

Ο PMI της Αυστραλίας στρέφεται ξανά σε συρρίκνωση, χωρίς ανοσία σε παγκόσμιους κινδύνους

Τον Αύγουστο, η Αυστραλιανή CBA PMI Manufacturing έπεσε από 51.6 σε 51.3. Η CBA PMI Services έπεσε από 52.3 σε 49.2. Η έξοδος PMI μειώθηκε από 52.1 σε 49.5. Το σύνολο των δεδομένων σηματοδότησε την πρώτη μείωση της παραγωγής από τον Μάρτιο, με επίκεντρο τον τομέα των υπηρεσιών. Η CBA σημείωσε ότι «η αδυναμία του νομίσματος οδήγησε σε ταχύτερη άνοδο των τιμών των εισροών της μεταποίησης, αλλά το κόστος των υπηρεσιών αυξήθηκε με πιο αδύναμο ρυθμό, όπως και οι τιμές παραγωγής και στους δύο παρακολουθούμενους τομείς».

Ο επικεφαλής οικονομολόγος της CBA, Michael Blythe, δήλωσε: «Μια επίμονη ανησυχία είναι ότι οι επιπτώσεις από τον εμπορικό πόλεμο ΗΠΑ-Κίνας θα μειώσουν τις παγκόσμιες κεφαλαιουχικές δαπάνες και τις καταναλωτικές δαπάνες καθώς οι προσεκτικές επιχειρήσεις και τα νοικοκυριά αποσύρονται στο περιθώριο. Η στροφή πίσω σε συσταλτικό έδαφος στην μέτρηση του CBA Flash PMI για τον Αύγουστο δείχνει ότι η Αυστραλία δεν έχει ανοσία σε αυτούς τους παγκόσμιους κινδύνους….” Τονίζονται επίσης οι προκλήσεις που αντιμετωπίζει η RBA στις προσπάθειές της να επαναφέρει τον πληθωρισμό στο εύρος στόχου 2-3%. στην έρευνα. Το χαμηλότερο δολάριο Αυστραλίας ασκεί ανοδική πίεση στις τιμές των εισροών. Αλλά το ανταγωνιστικό περιβάλλον συναλλαγών περιορίζει τη ροή προς τις τιμές παραγωγής».

GBP / USD Mid-Day Outlook

Καθημερινές στροφές: (S1) 1.2097; (Ρ) 1.2136. (R1) 1.2160. Περισσότερο….

GBP/USD’s strong rise and break of 1.2209 minor resistance suggests short term bottoming at 1.2014. Intraday bias is back on the upside for 55 day EMA (now at 1.2380) and above. But upside should be limited by 38.2% retracement of 1.3381 to 1.2014 at 1.2536. On the downside, break of 1.2108 minor support will turn bias to the downside for 1.2014. Break will resume larger decline for 1.1946 low.

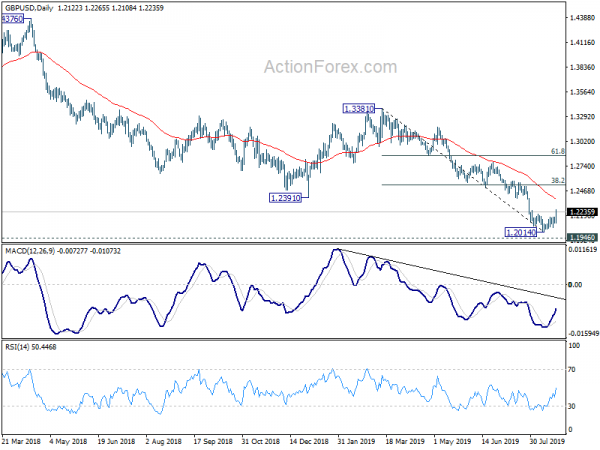

Στη μεγαλύτερη εικόνα, η τάση προς τα κάτω από το 1.4376 (υψηλό 2018) επεκτείνεται προς το χαμηλό 1.1946. Θα είμαστε προσεκτικοί στο κάτω μέρος. Αλλά το αποφασιστικό διάλειμμα θα επαναλάβει την τάση από 2.1161 (2007 high) σε προβολή 61.8% 1.7190 σε 1.1946 από 1.4376 στο 1.1135. Εν πάση περιπτώσει, οι μεσοπρόθεσμες προοπτικές θα παραμείνουν μέτριες καθ 'όλη τη διάρκεια της αντοχής του 1.3381, σε περίπτωση ισχυρής ανάκαμψης.

Ενημέρωση οικονομικών δεικτών

| GMT | Ccy | Εκδηλώσεις | Πραγματικός | Πρόβλεψη | Προηγούμενο | αναθεωρημένη |

|---|---|---|---|---|---|---|

| 23:00 | AUD | CBA PMI Manufacturing Aug P | 51.3 | 51.6 | ||

| 23:00 | AUD | Υπηρεσίες CBA PMI Aug P | 49.2 | 52.3 | ||

| 00:30 | JPY | PMI Manufacturing Aug P | 49.5 | 49.8 | 49.4 | |

| 04:30 | JPY | Δείκτης δραστηριότητας όλης του κλάδου M/M Ιουν | -0.80% | -0.80% | 0.30% | |

| 07:15 | EUR | Γαλλία PMI βιομηχανικής παραγωγής Aug P | 51 | 49.5 | 49.7 | |

| 07:15 | EUR | Γαλλία Υπηρεσίες PMI Aug P | 53.3 | 52.5 | 52.6 | |

| 07:30 | EUR | Γερμανία PMI βιομηχανικής παραγωγής Aug P | 43.6 | 43 | 43.2 | |

| 07:30 | EUR | Γερμανία Υπηρεσίες PMI Aug P | 54.4 | 54 | 54.5 | |

| 08:00 | EUR | PMI βιομηχανικής παραγωγής στην ευρωζώνη Aug P | 47 | 46.2 | 46.5 | |

| 08:00 | EUR | Υπηρεσίες Ευρωζώνης PMI Aug P | 53.4 | 53 | 53.2 | |

| 10:00 | GBP | Η CBI ανέφερε πωλήσεις Αύγ | -49 | -15 | -16 | |

| 11:30 | EUR | Λογαριασμοί συνεδρίασης νομισματικής πολιτικής της ΕΚΤ Ιουλ | ||||

| 12:30 | CAD | Πωλήσεις χονδρικής M / M Ιουν | 0.60% | -0.10% | -1.80% | -1.90% |

| 12:30 | USD | Αρχικές Απαιτήσεις Ανεργίας (AUG 17) | 209K | 217K | 220K | 221K |

| 13:45 | USD | PMI βιομηχανικής παραγωγής Aug P | 50.5 | 50.4 | ||

| 13:45 | USD | Υπηρεσίες PMI Aug P | 52.8 | 53 | ||

| 14:00 | USD | Κύριος Δείκτης Ιουλ | 0.20% | -0.30% | ||

| 14:00 | EUR | Καταναλωτική Εμπιστοσύνη της Ευρωζώνης Αύγουστος Αύγουστος | -7 | -6.6 | ||

| 14:30 | USD | Αποθήκευση φυσικού αερίου | 49B |

Signal2forex.com - Τα καλύτερα ρομπότ Forex και τα σήματα

Signal2forex.com - Τα καλύτερα ρομπότ Forex και τα σήματα