Ny tsenan'i Aziatika dia mihamafy amin'ny ankapobeny rehefa mametraka ny fifanolanana ao Hong Kong ny mpampiasa vola amin'izao fotoana izao. Somary nisondrotra ihany koa ny fihetseham-po satria nanome toky ny PBoC fa hanohy ny fepetra fanalefahana nokendrena. Ny sandam-bola amin'ny ankapobeny dia ambony noho ny notarihan'ny New Zealand Dollar amin'izao fotoana izao. Yen sy Dollar no malemy indrindra, arahin'ny Swiss Franc. Ny fikorontanana bebe kokoa dia mety ho hita rehefa miverina amin'ny fialantsasatra i UK sy Etazonia.

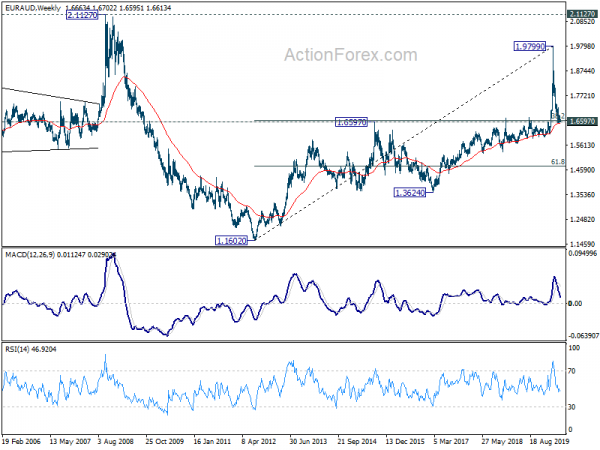

Ara-teknika, ny EUR / USD, EUR / JPY ary EUR / CHF dia miverina aorian'ny fanohanan'ny 4 ora 55 EMA, mitazona ny fankasitrahana amin'ny fotoana fohy kokoa. Na izany aza, ny EUR/AUD dia miverina manindry ny faritra fanohanana fototra amin'ny 1.6538/6597. Ny fiatoana maharitra eo dia hitondra fiantraikany lehibe kokoa ary mikendry ny faritra fanohanana 1.5962.6085 manaraka. Raha mitranga izany, dia mety ho famantarana ny tanjaky ny Aussie, noho ny fahalemen'ny Euro. Mety ho hitantsika fa ny AUD / USD dia mamakivaky ny 0.6618 ambony vonjimaika mba haka ny haavon'ny fanoherana lehibe amin'ny 0.6670 mifanaraka amin'izany.

Any Azia, amin'izao fotoana izao, Nikkei dia niakatra 2.34%. Hong Kong HSI dia niakatra 1.90%. China Shanghai SSE dia niakatra 0.71%. Singapore Strait Times dia niakatra 1.40%. Ny vokatra JGB 10 taona Japana dia nidina -0.0042 amin'ny 0.001.

Ny PBoC dia hanohy ny fanalefahana nokendrena rehefa mihatsara ny toe-karena anatiny

Nilaza ny governoran'ny PBoC Yi Gang fa ny lamosina afovoany Shinoa dia hitohy amin'ny fanalefahana nokendrena amin'izao fotoana izao, na dia mihatsara aza ny toe-karena anatiny. Ny fepetra nokendrena dia hiantoka ny famatsiam-bola ampy, ny fampidinana ny vidin'ny fampindramam-bola ary ny fanomezana crédit mora. Nandeha tsara ny fepetra ary mikasa ny hanao ny politika mazava kokoa ny PBoC.

Nanampy i Yi fa ny PBoC dia hampitombo ny fanavaozana ny tahan'ny fampindramam-bola, ary ny tahan'ny fampindramam-bola, mba hanampiana ny fampidinana ny tahan'ny fampindramam-bola tena izy. Ary koa, hampitambatra tsy tapaka ny petra-bola, ny tahan'ny fampindramam-bola ary ny tahan'ny zanabola.

Na izany aza dia mbola nampitandrina ihany izy fa miatrika fanamby goavana ny toekarena manerantany. Ny fihemorana amin'izao fotoana izao dia "mety ho ratsy kokoa noho ny krizy ara-bola eran-tany tamin'ny 2008 ary na dia ny Fihemorana lehibe aza."

BoJ Kuroda: Toe-karena ao anatin'ny toe-javatra mihasarotra, mety hijanona ho toy izany

Ao amin'ny Tatitra Semiannual momba ny Fanaraha-maso ny Vola sy ny Vola, nilaza ny Governemanta BoJ Haruhiko Kuroda fa ny "fepetra fanalefahana ara-bola mahery vaika" dia hanohana ny hetsika ara-toekarena sy ara-bola, miaraka amin'ny fepetra coronavirus an'ny governemanta. Naveriny ihany koa ny toky hanara-maso ny fiantraikan'ny coronavirus ary ny BoJ dia "tsy hisalasala handray fepetra fanalefahana fanampiny raha ilaina."

Nomarihiny indray fa ny toe-karena dia ao anatin'ny "toe-javatra mihamafy" ary "azo inoana fa hitoetra ho toy izany". Saingy avy eo. "Azo inoana fa hihatsara" ny toe-karena tohanan'ny fepetra ara-bola sy ny fepetran'ny governemanta, ary koa amin'ny alàlan'ny "fanantenana ho tonga amin'ny fitakiana tsy mitsaha-mitombo sy ny famerenana amin'ny laoniny ny famokarana avy amin'ny fihenan'ny fiparitahan'ny COVID-19."

Na izany aza, ny fijery dia "tsy mazava loatra" miankina amin'ny "fotoan'ny fihanaky ny fiparitahan'ny COVID-19 ary ny halehiben'ny fiantraikany amin'ny toe-karena ao an-toerana sy any ivelany". Ny risika dia “mivadika amin'ny lafy ratsiny.

BoC Poloz: Ny risika ambany sy ny mety hisian'ny deflation ny ahiahy lehibe amin'ny valin'ny coronavirus

Ny governoran'ny BoC Stephen Poloz dia nanao ny lahateniny farany omaly, talohan'ny nialany tamin'ny herinandro ho avy. Nanamarika izy fa ny "fanahy lehibe" amin'ny valin'ny krizy coronavirus dia "miaraka amin'ny risika ambany sy ny mety hisian'ny deflation."

"Ny deflation dia mifandray amin'ny trosa efa misy, ireo singa roa lehibe amin'ny fahaketrahana taloha," hoy izy nanampy. "Raha ny tena izy, dia nilaza izahay fa ny risika mitongilana dia tena mampatahotra fa tsy misy fifanakalozam-bola mifandraika amin'ny mpandinika ny vola."

Niaiky izy fa ireo hetsika ireo dia "hiteraka mazava ho amin'ny trosa ambony kokoa, indrindra ho an'ny governemanta". Ny famerenana ny toe-karena ho amin'ny fivoarany no "fomba azo antoka indrindra amin'ny fanompoana ireo trosa ireo rehefa mandeha ny fotoana".

Na izany aza, miaraka amin'ny toe-javatra "mihoatra ny loza noho ny fihemorana", ny fahatokisana dia antenaina fa "hohamafisin'ny fanohanana ara-bola" ary "fiverenana haingana amin'ny fitomboana". Saingy, "izay fahasimbana ara-drafitra rehetra, toy ny tsy fahombiazan'ny orinasa sy ny fahasimban'ny tsenan'ny asa, dia mazava ho azy fa haharitra ela ny fanamboarana."

ECB Villeroy: PEPP no fitaovana krizy tiana indrindra noho ny fahaizany

Ny mpikambana ao amin'ny Filankevitry ny Governemanta ECB Francois Villeroy de Galhau dia nanamarika fa ny banky foibe dia mety hampiakatra ny EUR 750B Pandemic Emergency Purchase Program mialoha. "Amin'ny anaran'ny fe-potoam-piasantsika no tena mila mandroso kokoa isika", hoy izy nandritra ny fihaonambe tany Pari. "Ny fahafaha-manaony indrindra no tokony hahatonga ny programa fividianana vonjy maika ho an'ny valan'aretina ho fitaovana an-jorom-bala ho an'ny fiatrehana ny vokatry ny krizy."

Miaraka amin'ny programa, ny fividianana taolana dia mety hikendry ireo firenena manana fiakarana maranitra kokoa amin'ny taham-bolam-bola. "Miankina amin'ny dinamika amin'ny tsena sy ny fepetra momba ny liquidity - ary ny toerana misy ireo banga tsy misy dikany na misy ny loza ateraky ny fikorontanana be loatra - ny banky foibe nasionaly sasany dia tsy maintsy afaka mividy betsaka kokoa, ary ny hafa dia kely kokoa, raha miantoka ny tsy fitoviana ny loza," hoy i Villeroy. .

Ao amin'ny front data

Nitombo hatrany amin'ny NZD 1257m ny ambim-bolan'i Nouvelle Zélande tamin'ny volana aprily, mifanaraka amin'ny andrasana. Nidina -4.0% yoy ny fanondranana entana ho NZD 5.3B. Nidina -22% yoy ny fanafarana entana ho NZD 4.0B. Ny vidin'ny vidin'ny serivisy Japoney dia niakatra 1.0% yoy tamin'ny volana aprily raha oharina amin'ny andrasana amin'ny 1.3% yoy.

Mitodika any aoriana, ny fihetseham-pon'ny mpanjifa Alemana Gfk, ny fifandanjana ara-barotra Soisa ary ny UK CBI dia nahatsapa fa ny fivarotana dia hasongadina amin'ny fivoriana eoropeana. Hivoaka ihany koa ny vidin'ny trano amerikana sy ny fivarotana trano vaovao. Fa ny tena hifantoka amin'ny fahatokiana.

GBP / USD Daily Outlook

Daily Pivots: (S1) 1.2165; (P) 1.2184; (R1) 1.2205; Bebe kokoa….

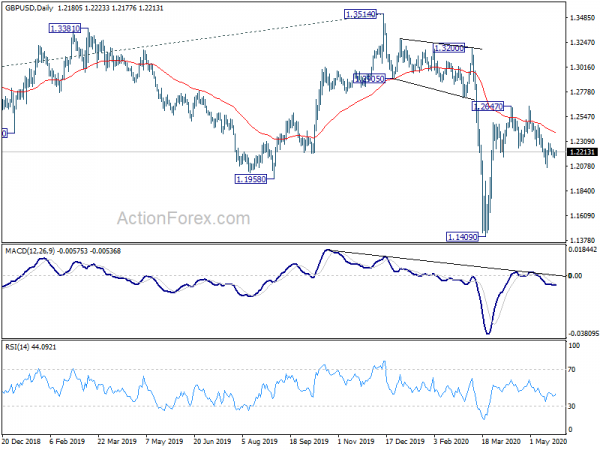

Ny fitongilanana intraday amin'ny GBP / USD dia mijanona ho tsy miandany na dia eo aza ny fanarenana ankehitriny. Miverina amin'ny fanoherana 1.2296 ny fifantohana. Ny fiatoana mafy dia tokony ho tonga miaraka amin'ny varotra maharitra mihoatra ny 4 ora 55 EMA. Izany dia manondro ny fahavitan'ny fianjeran'ny 1.2642, ary milaza fa tsy vita ny fiverenana avy amin'ny 1.1409. Ny fitongilanana intraday dia hiverina amin'ny fanoherana 1.2647. Na izany aza, raha mbola mitazona ny fanoherana 1.2296, ny fianjerana iray hafa dia hijanona ho malefaka. Ny fiatoana amin'ny 1.2065 dia mikendry fitsapana amin'ny ambany 1.1409.

Amin'ny sary lehibe kokoa, raha matanjaka ny fiverenana avy amin'ny 1.1409, dia tsy mbola misy famantarana ny fiverenan'ny fironana. Ny fironana midina avy amin'ny 2.1161 (avo 2007) dia tokony mbola hitohy na ho ela na ho haingana. Ny tanjona antonony manaraka dia ho 61.8% projection amin'ny 1.7190 mankany 1.1946 avy amin'ny 1.3514 amin'ny 1.0273. Na izany na tsy izany, ny fijery dia hitoetra ho manjavozavo raha mbola mitazona ny fanoherana 1.3514, raha toa ka misy rebound mahery.

Fampitandremana ara-toekarena

| GMT | Ccy | Events | Actual | Forecast | Previous | nohavaozina |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Apr | 1267M | 1270M | 672M | 722M |

| 23:50 | JPY | Fanondroana vidin'ny serivisy Y/Y Apr | 1.00% | 1.30% | 1.60% | |

| 04:30 | JPY | Tondron'ny hetsika indostria rehetra M/M Mar | -3.90% | -0.60% | ||

| 06:00 | EUR | Alemaina Gfk Consumer Confidence Jun | -18.6 | -23.4 | ||

| 06:00 | CHF | Trade Balance (CHF) Apr | 4.02B | |||

| 10:00 | GBP | Ny CBI dia nahatontosa ny varotra May | -50% | -55% | ||

| 13:00 | USD | S&P/Case-Shiller 20-Cities House Vidin'ny Y/Y Mar | 3.20% | 3.50% | ||

| 13:00 | USD | Fanondroana vidin'ny trano M/M Mar | 0.60% | 0.70% | ||

| 14:00 | USD | Consumer Consumer May | 87.1 | 86.9 | ||

| 14:00 | USD | Varotra trano vaovao Apr | 492K | 627K |

Signal2forex.com - Best robots Forex sy famantarana

Signal2forex.com - Best robots Forex sy famantarana