Dollar and Yen staged strong rebounds overnight, as stocks tumbled after US President Donald Trump halted stimulus talks abruptly. Though, markets somewhat stabilized in Asian session. Swiss Franc and Euro remain the strongest ones for the week for far but both have already pared back much of earlier gains. Australian and New Zealand Dollars are currently the weakest ones. More volatility are still anticipated ahead with eyes on US politics and coronavirus infections. It’s just early in October and more surprises could be lying ahead for us.

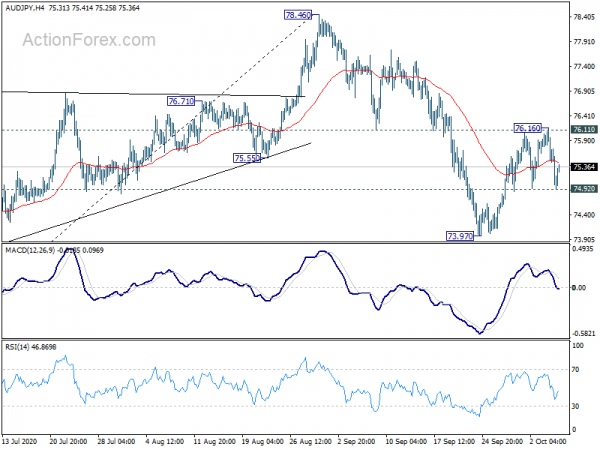

Technically, Gold’s breach of 1881.30 support is taken as a sign that Dollar might be coming back. Indeed, even Euro and Swiss Franc couldn’t take out near term resistance level against Dollar cleanly after yesterday’s decline. Focuses are now turning back to 1.1695 support in EUR/USD, 0.9218 resistance in USD/CHF to gauge the change for Dollar to resume recent rebound. The same goes for Yen. Break of 74.92 minor support in AUD/JPY would firstly indicate completion of rebound form 73.97 after rejection by 76.11 support. Secondly, the corrective fall from 78.46 is likely resuming through 73.97 in this case.

In Asia, DOW closed down slightly by -0.05%. Hong Kong HSI is up 0.73%. China is still on holiday. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is flat at 0.035. Overnight, DOW dropped -1.34%. S&P 500 dropped -1.40%. NASDAQ dropped -1.57%. 10-year yield dropped slight by -0.020 to 0.742, staying resilient.

US stocks tumbled as Trump pulled out of stimulus talks

US stocks staged a reversal and tumbled sharply overnight after US President Donald Trump halted stimulus negotiations with Democrats, until after election. He revealed in a tweet “I have instructed my representatives to stop negotiating until after the election when, immediately after I win, we will pass a major Stimulus Bill that focuses on hardworking Americans and Small Business.” The USD 2.2 trillion price tag is an issue that some Republicans explicitly opposed to. Besides, they’re also against the bailout of state and local governments. Separately, Trump urged immediately approval of USD 25 billion bailout for airline and small businesses, with the unused funds from the Cares Act.

DOW closed down -1.34% or 375.88 pts at 37772.76, nearly all of Monday’s gains. Our overall view on DOW is unchanged. Current rise from 26537.01 is seen as the second leg of the consolidation pattern from 29199.35 high. While further rise cannot be ruled out, we wouldn’t expect a clean break of 29199.35. Another falling leg is expected before the consolidation completes. Sustained break of 55 day EMA (now at 27407.26) will suggest that the third leg has started towards 38.2% retracement of 18213.65 to 29199.35 at 25002.81.

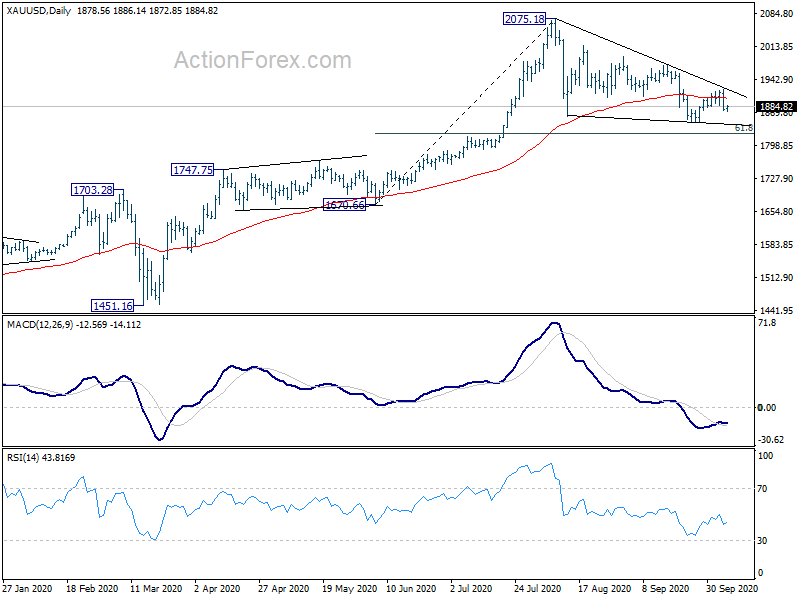

Gold rejected by trend line resistance, heading back to 1848 support

Gold’s sharp fall and breach of 1681.30 support suggests that recovery from 1848.38 has completed at 1921.01, after rejection by near term falling trend line resistance. Further fall is now in favor to 1828.39 support. Break there will extend the correction from 2075.18 to 61.8% retracement of 1670.6 to 2075.18 at 1825.18. This will remain the favored case now as long as 1921.01 resistance holds. Also, such development, if happens this way, will likely be accompanied by stronger rebound in Dollar.

Fed Powell: Risk of policy intervention still asymmetric

Fed Chair Jerome Powell said in a speech that the economic expansion is “still far from complete”. “At this early stage I would argue that the risks of policy intervention are still asymmetric,” he added. “Too little support would lead to a weak recovery, creating unnecessary hardship for households and businesses.”

Powell also noted, “the risks of overdoing it seem, for now, to be smaller. Even if policy actions ultimately prove to be greater than needed they will not go to waste. The recovery will be stronger and move faster.”

On the economy, Powell also said that the improvement has “moderated” and “risk that the rapid initial gains from reopening may transition to a longer-than-expected slog back to full recovery.”

On the data front

Australia AiG Performance of Services index dropped to 36.2 in September, down from 42.5. Japan leading indicator rose to 88.8 in August, up fro 86.9, below expectation of 89.4. Germany industrial production dropped -0.2% mom in August, below expectation of 1.5% mom rise. France trade balance, Swiss foreign currency reserves and Italy retail sales will be released in European session. Canada Ivey PMI and FOMC minutes are the main features in US session.

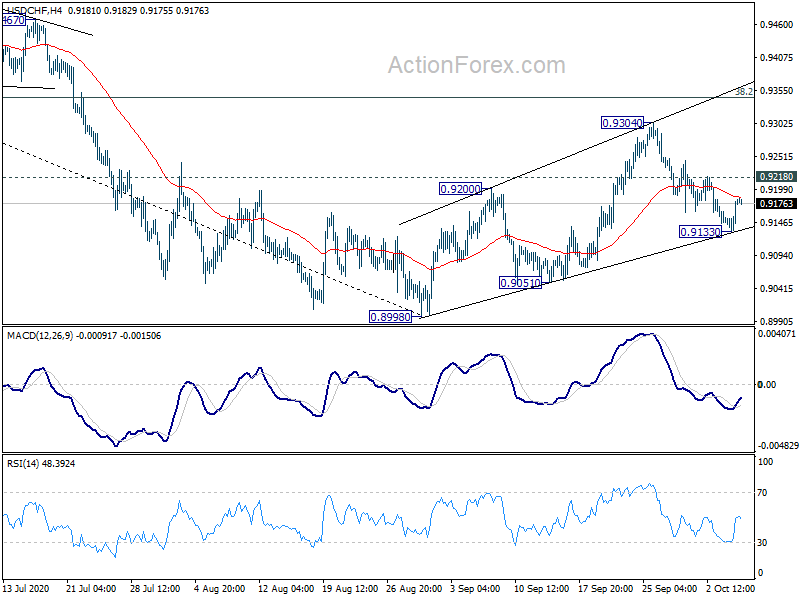

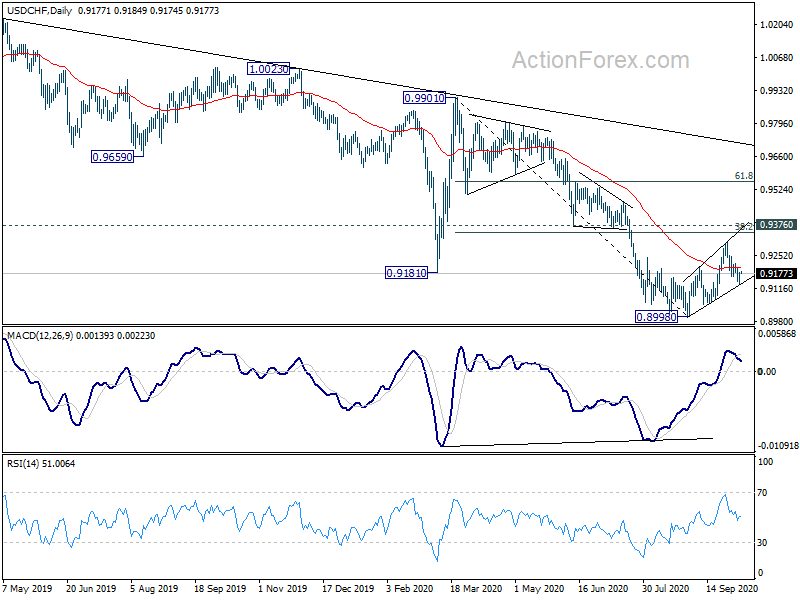

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9147; (P) 0.9163; (R1) 0.9194; More…

Intraday bias in USD/CHF is turned neutral with 4 hour MACD crossed above signal line. Further fall is mildly in favor as long as 0.9218 minor resistance holds. Below 0.9133 will target a test on 0.8998 low. However, on the upside, break of 0.9218 minor resistance will argue that corrective rebound from 0.8998 is not completed yet. In this case, intraday bias will be turned back to the upside for 0.9304 resistance instead.

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 high). There is no clear sign of completion yet. On resumption, next target will be 138.2% projection of 1.0342 to 0.9186 from 1.0237 at 0.8639. Nevertheless, strong break of 0.9376 support turned resistance will be an early sign of trend reversal and turn focus back to 0.9901 key resistance for confirmation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Services Index Sep | 36.2 | 42.5 | ||

| 5:00 | JPY | Leading Economic Index Aug P | 88.8 | 89.4 | 86.9 | 86.7 |

| 6:00 | EUR | Germany Industrial Production M/M Aug | -0.2% | 1.50% | 1.20% | 1.4% |

| 6:45 | EUR | France Trade Balance (EUR) Aug | -6.5B | -7.0B | ||

| 7:00 | CHF | Foreign Currency Reserves (CHF) Sep | 848B | |||

| 8:00 | EUR | Italy Retail Sales M/M Aug | 3.80% | -2.20% | ||

| 14:00 | CAD | Ivey PMI Sep | 67.8 | |||

| 14:30 | USD | Crude Oil Inventories | -2.0M | |||

| 18:00 | USD | FOMC Minutes |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals