Insider trading remains a rampant problem on Wall Street, with new research finding that the nation’s largest financial institutions pocket hefty sums with the help of nonpublic information.

A study from the University of Cambridge and Stanford holds that well-informed insiders at major U.S. banks bolstered profits thanks to advanced knowledge of government programs during the financial crisis.

Specifically, the economists found “strong evidence” of a relationship between political connections and informed trading, especially during the period in which Troubled Asset Relief Program funds were distributed. The findings were reported in The Economist.

TARP, signed into law in 2008, allowed the U.S. Treasury to buy or insure up to $700 billion in toxic assets and equity, $250 billion of which flowed into banks. So important was this cash infusion that the nation’s nine largest banks were required to participate, with deliberations on the intervention taking place in private meetings between the government and financial insiders.

“Political connections appear to have played a role in the allocation of these funds,” wrote Alan Jagolinzer, professor at the University of Cambridge’s Judge Business School. “Thus, politically connected insiders at leading financial institutions were in a position to be disproportionately privately informed about the scope of government intervention.”

“Our findings suggest that politically connected insiders had an information advantage during the Crisis and traded to exploit this advantage,” he added.

Consistent with their hypothesis, Jagolinzer and his colleagues found no evidence that insider trades boosted performance in the two years prior to the crisis and the creation of TARP. In contrast, however, in the nine months after the program’s creation, insiders seemed much better at positioning themselves.

There was no difference in the returns of insiders who had political connections and those who didn’t in the period before the crisis, the researchers found. However, within the period TARP funds were distributed, the one-month returns of insiders with political connections and those without them were both economically and statistically significant, 8.89 percent versus 2.81 percent, respectively.

Jay Clayton, the attorney tapped last year by President Donald Trump to lead the Securities and Exchange Commission, argued that the agency doesn’t need Congress’ help in prosecuting insider trading.

“I look at it this way,” Clayton said in September. “I think we do a pretty good job in this space as I compare it to other jurisdictions.”

The SEC recently notched a major victory against inside traders with a court decision upholding the 2014 conviction of former SAC Capital Advisors portfolio manager Mathew Martoma.

The Second U.S. Circuit Court of Appeals concluded last August that federal prosecutors no longer need to show a “meaningfully close personal relationship” between the provider of insider intel and the recipient of the tip.

While the first paper restricted itself to TARP, a second paper from Harvard Business School found that large investors tend to trade more in periods ahead of portfolio liquidation announcements, giving select clients a competitive advantage over retail investors.

That study used a detailed trade-level dataset from Abel Noser Holdings that reported information on the institutional investors and brokers involved in each trade between 1999 and 2014.

“Aware” brokers may have an incentive to tip off their larger clients about an impending portfolio liquidation, giving predatory traders a chance to sell the same assets, the study said.

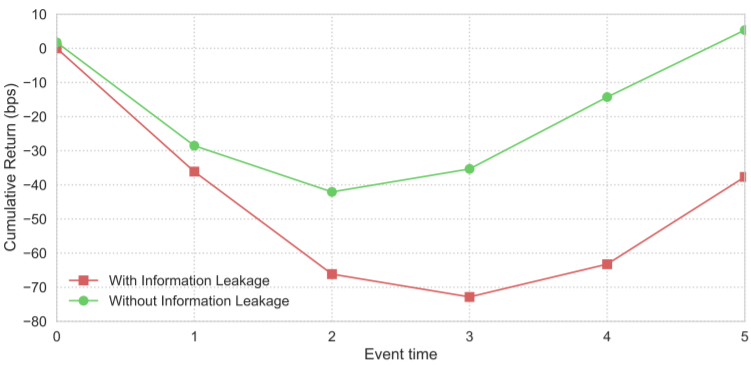

Source: Di Maggio et al., 2017

“The main result of this analysis is that the best clients of the aware brokers are significantly more likely than other clients to sell the stocks that the liquidating manager is offloading during the fire sale,” wrote Marco Di Maggio, assistant professor at Harvard Business School. “The predatory trades generate at least 50 basis points over 10 days and causes the liquidation costs for the distressed fund to almost double.”

“We find that the clients who are more likely to receive order flow information tend to increase their commissions to the brokers,” Di Maggio added, “which strongly suggests a quid pro quo between these parties.”

Link to the source of information: www.cnbc.com

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals