Sterling remains the strongest one as markets is now preparing for inflation data from UK today. The progress in Brexit negotiation removed one key obstacle for BoE to hike again in May. And CPI data will be a key factor for MPC’s consideration. Hence, any upside surprise would likely lead to further rally in the Pound. Yen trades broadly lower this week even though stock markets were generally in risk averse mode. But it should be noted that Yen was actually not that weak considering that it’s staying well inside last week’s range. And Dollar is not performing much better. In addition to economy data, G20 communique on trade will be watched today as trade war remains a concern of investors.

UK CPI might prompt BoE hawks’ comeback

The BoE rate decision this Thursday becomes lively as the transition deal is done. UK CPI data to be released today will be the first key factor. Headline CPI is expected to slow from 3.0% yoy to 2.8% yoy in February. Core CPI is expected to slow from 2.7% yoy to 2.5% yoy. On the one hand, the deal should give BoE policymakers some comfort to restart lifting interest rate from the current ultra low level at 0.50%. On the other hand, any upside surprise in today’s inflation data would indeed give some pressure for BoE to act again.

And for the meeting, ahead, while BoE is still expected to stand pat, the statement could turn more relaxed and optimistic given that the Brexit picture is slightly clearer. And more importantly hawks like Ian McCafferty and Michael Saunders might come back to vote for rate hike.

According to a Bloomberg survey, majority of economists expected BoE to vote 9-0 to keep interest rate unchanged at 0.50% later this week on Thursday. And, 54% of economists expected BoE to hike interest rate in May. That’s a slight adjustment from 51% at prior survey. However, the data was taken as of March 19. And it’s unsure how much regarding the Brexit transition deal was taken into consideration. And that could only be reflected in the next survey.

Recap on Brexit transition deal

To recap, the transition period will last from Brexit day on March 29, 2019 to December 31, 2020. The key terms in the agreement include the followings: EU citizens arriving in the UK between these two dates will enjoy the same rights and guarantees as those who arrive before Brexit. The same will apply to UK expats on the continent; The UK will be able to negotiate, sign and ratify its own trade deals during the transition period; The UK will still be party to existing EU trade deals with other countries The UK’s share of fishing catch will be guaranteed during transition but UK will effectively remain part of the Common Fisheries Policy, yet without a direct say in its rules, until the end of 2020;

Northern Ireland will effectively stay in parts of the single market and the customs union in the absence of other solutions to avoid a hard border with the Republic of Ireland. Indeed, UK Prime Minister Theresa May has described the arrangement for Northern Ireland as “unacceptable” as it would effectively shift the existing land border to the Irish Sea and compromise UK sovereignty. Yet, the EU suggested this “backstop option” was a key part of December’s phase one agreement with the UK and this would remain effective “unless and until another solution is found”.

EU Moscovici at G20: We must absolutely avoid trade wars

European Economics Commissioner Pierre Moscovici he’s “cautiously optimistic” that there could be an agreement on the language on trade out of G20 meeting. And he hoped that the G20 communique will show that “how that protectionism is not the solution and we must absolutely avoid that.” He warned that “the first risk is the risk of inward looking policies and protectionism.”

Regarding US requests to omit the term “multilateral” from there statement, Moscovici blasted that “avoiding multilateralism in a multilateral organization makes no sense.” He further added that “a trade war would be stupid. There would be damage on both sides of the Atlantic.” Moscovici also reiterated that EU is prepared for counter-measures to US if it’s not exempted from the steel and aluminum tariffs. Moscovici noted “but we think the best is to avoid a scale up” because “we must absolutely avoid trade wars.”

On the other hand, US Treasury Secretary Steven Mnuchin emphasized in an email statement that “The trip to the G-20 will focus on advancing the Trump administration’s global economic agenda to level the playing field for U.S. companies and workers.”

Trump to announce USD 60b tariff against China on Friday

It’s known that Trump is preparing to impose a package of USD 60b in tariffs against China. It’s reported that the package would apply to over 100 products. These products are believed by Trump to use trade secretes stolen from US companies, or forced to hand over in exchange for market access. The theme appears to be consistent with Section 301 intellectual property theft investigation and actions. But no one knows how relevant is that until there a a published list of products. Trump is planning to announce the action by Friday.

China Premier Li pledges to open market

China Premier Li Keqiang said today after a press conference that there is no forced transfer of technology. But he pledged that China will better protect intellectually property. Also, China will further open up the economy, lower import tariffs and allow foreign and domestic companies to compete on equal ground. China commerce ministry said that there is WTO ruling against tariffs directed only at them. And it urged the US to correct the abuse of trade measures. But the MOFCOM didn’t comment directly on the reported USD 60b tariff package.

ECB Mersch: Prerequisites there for inflation, but easy policy still needed

ECB Executive Board member Yves Mersch sounded upbeat on his comments yesterday. He said that “all prerequisites for a sustainable adjustment of inflation to our objective are given.” The central bank could continue to cut down its asset purchases gradually as inflation outlook improves. He’s concerned that there could be excessive market reactions if the asset purchases are reduced too quickly. And that would undo ECB’s hard work in the past few years. Overall, for the time being, easy monetary policy is still needed to support inflation.

Little surprise from RBA minutes

The RBA minutes for the March contained little surprise. Policymakers remained concerned about the soft inflation outlook, noting faster wage growth is needed to assure a stronger and more sustainable improvement on inflation. As suggested in the minutes, “employment had grown strongly and the unemployment rate had fallen over the preceding year. However, the improvement in overall conditions had not yet translated into a definitive pick-up in wages growth, which remained low”. It added that “further progress on these goals [reducing the unemployment rate and bringing inflation closer to target] was expected over the period ahead, but this process was likely to be gradual”.

Also from Australia, house price index rose 1.0% qoq in Q4 versus expectation of 0.0% qoq.

Looking ahead

The European session is very busy today. UK CPI will take center stage while PPI and house price index will also be featured. Germany will release ZEW economic sentiment and PPI. Swiss will release trade balance. Later in the day Canada will release wholesale sales.

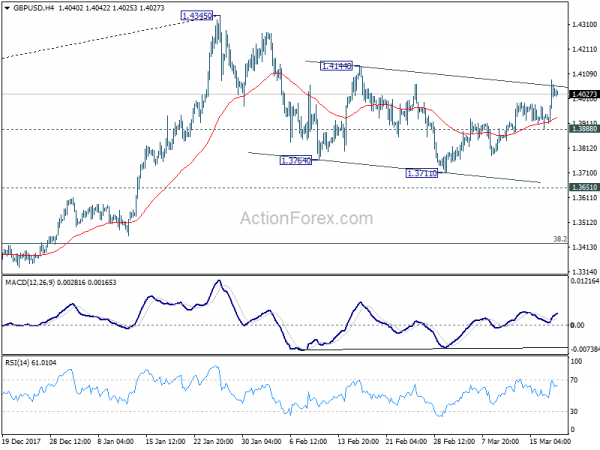

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3927; (P) 1.4008; (R1) 1.4103; More….

At this point, intraday bias in GBP/USD remains on the upside as the rebound from 1.3711 is in progress. As noted before, current development affirms the case that correction from 1.4345 has completed at 1.3711 already. Break of 1.4144 should confirm this bullish view and target 1.4345 and above. The larger up trend from 1. 1946 might be ready to resume. ON the downside, however, break of 1.3888 minor support will dampen this bullish view. Intraday bias would be turned back to the downside to extend the decline from 1.4345 through 1.3711 instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | House Price Index Q/Q Q4 | 1.00% | 0.00% | -0.20% | |

| 0:30 | AUD | RBA March Meeting Minutes | ||||

| 6:45 | CHF | SECO Economic Forecasts March | ||||

| 7:00 | EUR | German PPI M/M Feb | 0.10% | 0.50% | ||

| 7:00 | EUR | German PPI Y/Y Feb | 2.00% | 2.10% | ||

| 7:00 | CHF | Trade Balance (CHF) Feb | 1.87B | 1.32B | ||

| 9:30 | GBP | CPI M/M Feb | 0.50% | -0.50% | ||

| 9:30 | GBP | CPI Y/Y Feb | 2.80% | 3.00% | ||

| 9:30 | GBP | Core CPI Y/Y Feb | 2.50% | 2.70% | ||

| 9:30 | GBP | RPI M/M Feb | 0.80% | -0.80% | ||

| 9:30 | GBP | PPI Input M/M Feb | -0.90% | 0.70% | ||

| 9:30 | GBP | PPI Input Y/Y Feb | 3.80% | 4.70% | ||

| 9:30 | GBP | PPI Output M/M Feb | 0.10% | 0.10% | ||

| 9:30 | GBP | PPI Output Y/Y Feb | 2.70% | 2.80% | ||

| 9:30 | GBP | PPI Output Core M/M Feb | 0.20% | 0.30% | ||

| 9:30 | GBP | PPI Output Core Y/Y Feb | 2.40% | 2.20% | ||

| 9:30 | GBP | House Price Index Y/Y Jan | 5.00% | 5.20% | ||

| 10:00 | EUR | German ZEW (Economic Sentiment) Mar | 13 | 17.8 | ||

| 10:00 | EUR | German ZEW Current Situation Mar | 90 | 92.3 | ||

| 10:00 | EUR | Eurozone ZEW (Economic Sentiment) Mar | 28.1 | 29.3 | ||

| 12:30 | CAD | Wholesale Trade Sales M/M Jan | 0.40% | -0.50% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Mar A | 0 | 0.1 |

Link to the source of information: www.actionforex.com

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals