Dollar’s corrective pull back yesterday was rather brief and shallow. EUR/USD reached 1.1995 but failed to break through 1.2 handle. It’s now back at 1.1930. USD/CHF breached parity briefly to 0.9956 and is back above 1.0000 now. GBP.USD continued to stay in tight range above 1.3459 and failed even to take out 1.3617 minor resistance. The greenback is staying in corrective mode in general, awaiting some fresh stimulus.

There are a couple of market moving events today. UK employment data is a notable one in the European session. The timing of the next BoE rate hike, be it August or November or next year, is very much data dependent. Sterling has been so far resilient but it will be vulnerable should there be another downside surprise in wage growth released today.

Also featured in European session are Eurozone GDP and industrial production and Germany GDP. But ZEW economic sentiment could be the market moving one. ECB is unsure whether the slowdown in Q1 is due to temporary factors only. And policymakers will continue to look at incoming economic data to get a clearer picture. Whether ECB could stop the asset purchase program after September will depend on ECB’s interpretation of the data.

– advertisement –

Later in the day, US will release retail sales, business inventories, Empire state manufacturing index and NAHB housing index. We’d not expecting much inspirations from these data. While retail sales is always seen as an important one, the impact on Dollar is seldom long lasting. Instead, the focus will firstly be on US-China trade talks. And secondly, 10 year yield is back pressing 3% level yesterday, hitting as high as 2.997, closing at 2.995. We’ll see if there is sustainable strength in yield that could give Dollar a lift.

RBA minutes reiterated no strong case for near term hike

RBA May meeting minutes reiterated that central bank’s stance that it’s not in rush to lift interest rates. The minuted noted that “stronger growth was expected over the following couple of years, which could reduce spare capacity in the economy and lead to a further gradual decline in the unemployment rate.” But, “the increase in wages growth and inflation was expected to be gradual however because spare capacity in the economy was expected to be reduced only slowly.” And, “as progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy.”

RBA Debelle: 2% is the focal point for wage outcomes now

RBA Deputy Governor Guy Debelle delivered a speech titled “The Outlook for the Australian Economy” at the CFO Forum in Sydney today, where he talked about wages. He noted that “the experience of other countries with labour markets closer to full capacity than Australia’s is that wages growth may remain lower than historical experience would suggest.”

Currently in Australia “2% seems to have become the focal point for wage outcomes, compared with 3–4% in the past.” Even so, “”there is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2% focal point evident in many wage outcomes today”.

Trump’s tweet on ZTE prompted bipartisan criticism

Trump’s tweet regarding helping China telecoms company ZTE prompted bipartisan criticism and concerns on his softening stance. Republican Senator Marco Rubio said he hoped “this isn’t the beginning of backing down to China.” Democrat Senator Chuck Schumer said “this leads to the greatest worry, which is that the president will back off on what China fears most – a crackdown on intellectual property theft – in exchange for buying some goods in the short run.”

On the other hand, Trump defended with another tweet saying that “ZTE, the large Chinese phone company, buys a big percentage of individual parts from U.S. companies. This is also reflective of the larger trade deal we are negotiating with China and my personal relationship with President Xi”.

US Ambassador to China Branstad: Trump wants a “dramatic increase” in food exports to China

US Ambassador to China Terry Branstad said in Tokyo today that both countries are still “very far apart” on resolving trade frictions. Branstad, was present at the meeting between Treasury Secretary Steven Mnuchin and Chinese Vice Premier Liu He in Beijing earlier this month. He noted that “there are many areas where China has promised to do but haven’t. We want to see a timetable. We want to see these things happen sooner or later.” He added that Trump would like to see a “dramatic increase” in food exports to China” and “we’d like to see China being just as open as the United States.”

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1903; (P) 1.1950 (R1) 1.1975; More….

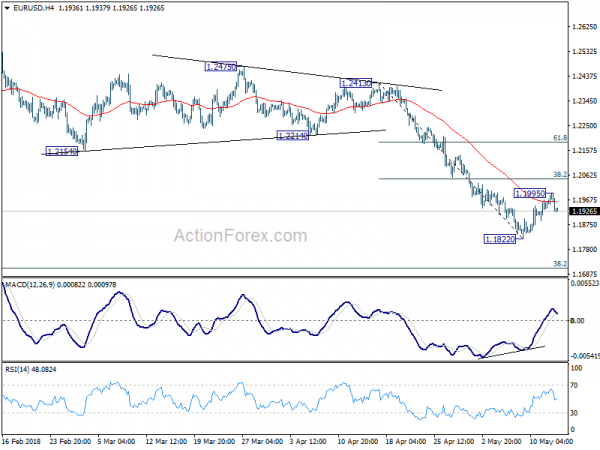

EUR/USD’s recovery from 1.1822 short term bottom could have completed at 1.1995 already, ahead of 38.2% retracement of 1.2413 to 1.1822 at 1.2048. Intraday bias is turned back to the downside for retesting 1.1822 first. Break there will resume whole decline from 1.2555 and target 1.1708 medium term fibonacci level next. In case of another recovery as the correction extends, upside should be limited by 1.2048 to bring fall resumption eventually.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2179) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:30 | AUD | RBA May Meeting Minutes | ||||

| 2:00 | CNY | Retail Sales Y/Y Apr | 9.40% | 10.00% | 10.10% | |

| 2:00 | CNY | Industrial Production Y/Y Apr | 7.00% | 6.40% | 6.00% | |

| 4:30 | JPY | Tertiary Industry Index M/M Mar | -0.20% | 0.00% | ||

| 6:00 | EUR | German GDP Q/Q Q1 P | 0.40% | 0.60% | ||

| 7:15 | CHF | Producer & Import Prices M/M Apr | 0.30% | -0.20% | ||

| 7:15 | CHF | Producer & Import Prices Y/Y Apr | 3.00% | 2.00% | ||

| 8:30 | GBP | Jobless Claims Change Apr | 13.3K | 11.6K | ||

| 8:30 | GBP | Claimant Count Rate Apr | 2.40% | |||

| 8:30 | GBP | Average Weekly Earnings 3M/Y Mar | 2.60% | 2.80% | ||

| 8:30 | GBP | ILO Unemployment Rate 3Mths Mar | 4.20% | 4.20% | ||

| 9:00 | EUR | Eurozone Industrial Production M/M Mar | 0.70% | -0.80% | ||

| 9:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.40% | 0.40% | ||

| 9:00 | EUR | German ZEW Economic Sentiment May | -8.2 | -8.2 | ||

| 9:00 | EUR | German ZEW Current Situation May | 85.2 | 87.9 | ||

| 9:00 | EUR | Eurozone ZEW Economic Sentiment May | 2 | 1.9 | ||

| 12:30 | USD | Empire State Manufacturing May | 15 | 15.8 | ||

| 12:30 | USD | Retail Sales Advance M/M Apr | 0.30% | 0.60% | ||

| 12:30 | USD | Retail Sales Ex Auto M/M Apr | 0.50% | 0.20% | ||

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.60% | ||

| 14:00 | USD | NAHB Housing Market Index May | 70 | 69 | ||

| 20:00 | USD | Net Long-term TIC Flows Mar | 49.0B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals