Global markets are blessed by strong risk appetite this week so far. DOW closed up 298.2 pts or 1.21% at 25013.29. S&P 500 also gained 0.74% while NASDAQ jumped 0.54%. FTSE jumped to record high at 7859.17 while CAC 40 also extended recent up trend to 5637.5. These were in response to positive developments out of US-China trade talks. Though, risk appetite eased a bit in Asian session as Nikkei is trading slightly in red, down -0.13% at the time of writing. In other markets, US 10 year yield dipped mildly overnight to close down -0.002 at 3.065. WTI crude oil extended recent rise and closed at 72.24. Meanwhile, gold is trying to draw support from 1280 but failed to grab 1290 again.

In the currency markets, Yen recovers mildly today as risk appetite eased. But it’s staying as the second weakest one for the week, next to Sterling. Commodity currencies are generally strong, with Australian Dollar leading the way up, followed by Canadian Dollar and New Zealand Dollar.

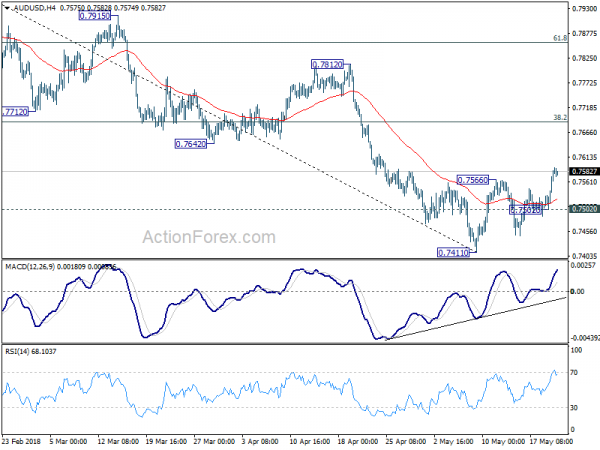

Technically, EUR/USD is trying to draw support from key fibonacci level at 1.1708. But it will have to overcome 1.1821 minor resistance to form a short term bottom first. USD/CHF’s corrective move from 1.0056 is set to extend and could gyrate lower. AUD/USD’s break of 0.7566 minor resistance suggests that corrective rebound from 0.7411 is extending. GBP/USD is staying bearish with downside bias.

– advertisement –

Philadelphia Fed Harker: Appropriate to continue rate hikes judiciously

Philadelphia Fed President Patrick Harker said yesterday that he sees two more rate hike this year. He noted it’s “prudent to continue to move away from the zero lower bound”. And Inflation “does seem to be moving toward 2%”. He added that there is “not much slack in the labor markets”. Hence, it’s appropriate to continue rate hikes “judiciously”.

And if there is an “acceleration of inflation”, then he “supportive of a third”. Though, he is not yet seeing a “rapid acceleration” in inflation yet.

Minneapolis Fed Kashkari: Fed should hike only to neutral policy stance

Minneapolis Fed President Neel Kashkari said in a article that “inflation and wage growth have been surprisingly low” despite tight job market. Now, wages is only growing at 2.7% annually, comparing to 3.5% before the financial crisis.

He pointed out that the headline unemployment rate in the US “captures” only those who are actively looking for jobs. Therefore, the 3.9% unemployment rate may not “capture the true slack” in the market. And “hidden slack” could explain the modest wage growth.

And Kashkari concluded that Fed should hike “only to a neutral policy stance, and not move too quickly”. And that’s until there are more evidence of wage growth and the US is “really” at maximum employment.

US Pompeo outlined steep demand for Iran, or the strongest sanctions in history

US Secretary of State Mike Pompeo outlined a list of demand for Iran to comply to, and threatened the country with “the strongest sanctions in history” if Iran doesn’t change course. Some of the demand include stopping enrichment of uranium, allowing unqualified access to all sites throughout the country, declare all previous nuclear weapon efforts, end support for Shiite Houthi rebels in Yemn, withdraw all forces from Syria, etc.

Pompeo also added that “I know our allies in Europe may try to keep the old nuclear deal going with Tehran. That is their decision to make.” But, ‘they know where we stand.” It’s seen that Iran is highly unlikely to meet these demands. Meanwhile, EU is expected to keep their pledge to retain the current JCoPA Iran. Comments from EU officials would be noted in the coming days.

Italian President Mattarella called meeting of political leaders after getting Prime Minster nomination

Italian President Sergio Mattarella called the leaders of the lower and upper houses of the parliament for a meeting today. That came after meeting with anti-establishment 5-Star Movement and far-right League, who have agreed on a deal to form a coalition government.

5-Star leader Luigi Di Maio said after meeting with Mattarella that Giuseppe Conte, a law professor but a political novice, “will be the prime minister of a political government”. Maio hailed that Conte is “a person that can carry out the government contract” and he’s “proud” of this choice. Leader of the League Matto Salvini also confirmed the name.

For now, it’s uncertain whether Mattarella will appoint Conte as the Prime Minister, or he’d prefer a more high-profile figure.

BoJ Kuroda to patiently pursue powerful monetary easing

BoJ Governor Haruhiko Kuroda reiterated to the parliament today that the central bank “won’t end the ultra-easy policy before inflation reaches 2 percent”. And BoJ will “patiently pursue powerful monetary easing”. Though, Kuroda also noted policymakers will take into account the “side effects” such as the “impact of financial institutions, particularly regional banks”.

Regarding the economy, Kuroda said it’s expanding moderately, with consumption helped by loose monetary policy. While there is sustaining momentum in growth, prices lack so. And there is still some distance to inflation target. BoJ will remain mindful of uncertainties on economic and price outlook.

Deputy Governor Masazumi Wakatabe said that BoJ can achieve the inflation target “with the current policy”. Though, “if conditions change and our current policy becomes inappropriate, we may need to change policy.”

Light economic calendar with BoE inflation report hearing

Looking ahead, the economic calendar remains rather light today. UK will release public sector net borrowing and CBI trends total orders. Canada will release Wholesale trade sales. Though, a major focus will be on BoE inflation report hearing.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7527; (P) 0.7558; (R1) 0.7612; More…

AUD/USD’s rebound from 0.7411 resumed by breaking 0.7566 and reaches as high as 0.7592 so far. Intraday bias is mildly on the upside for further rise, possibly to 55 day EMA (now at 0.7633). But strong resistance should be seen at 38.2% retracement of 0.8135 to 0.7144 at 0.7688 to limit upside and bring decline resumption eventually. On the downside, below 0.7502 minor support will turn intraday bias back to the downside for 0.7411 short term bottom first. Break will resume the fall from 0.8135 and target cluster support at 0.7328 (61.8% retracement of 0.6826 to 0.8135 at 0.7326).

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. Break of 0.7500 key support suggests that such correction is completed at 0.8135. Deeper decline would be seen back to retest 0.6826 low. In case of another rise, we’d expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption eventually.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | GBP | Public Sector Net Borrowing Apr | 7.2B | -0.3B | ||

| 10:00 | GBP | CBI Trends Total Orders May | 2 | 4 | ||

| 12:30 | CAD | Wholesale Trade Sales M/M Mar | 0.80% | -0.80% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals