Canadian Dollar, Euro, to a lesser extend Sterling, are the clear losers today. The Loonie is dragged down by oil price as WTI drops through 70 handle. It reaches as low as 68.96 so far on news that OPEC and Russia are considering to raise production. On the other hand, concerns over Italy’s new Eurosceptic government sent Italy-Germany yield spread to above 200pts for the first time. German 10 year bund yield dives to as low as 0.422, down more than -0.050 today.

For the week, Yen is emerging as the strongest on as helped by risk aversion, and more so by falling major global treasury yields. It should be noted that US 10 year yield dropped below 3% handle earlier this week and there is no strength for a rebound yet. Aussie is being very resilient, with lack of any news, and would likely end as the second strongest one. Sterling and Euro are the weakest while Dollar is just mixed.

Technically, near term declines in EUR/USD, EUR/JPY, EUR/AUD are extending in early US session. Focuses will be on whether GBP/USD will take out 1.3303 temporary low, and whether GBP/JPY will break 145.67 temporary low. Also, with current upside momentum, USD/CAD could finally take out 1.2996 near term resistance to confirm bullishness.

– advertisement –

Released from US, durable goods orders dropped -1.7% in April, below expectation of -1.4%. Ex-transport orders rose 0.9%, above expectation of 0.5%.

WTI oil price drops below 70 as OPEC and Russia consider lifting production

WTI crude oil drops below 70 handle on reports that Saudi Arabia and Russia are going to push for lifting production later in the year. The total of boost in production from OPEC and non-OPEC countries could add up to as high as 1 million barrels a day.

Saudi Arabia a Energy Minister Khalid al-Falih is quoted saying in St. Petersburg that the easing of restriction on production would be gradual, so as to avoid shocking the markets. He also added that “all options are on the table” regarding output cuts.

Meanwhile USD 80 a barrel seems to be a psychological level that the oil producing countries want to avoid. The decision could be made as soon as during the next OPEC meeting on June 22 in Vienna.

No revision in UK Q1 GDP

UK Q1 GDP was left unrevised at 0.1% qoq meeting market consensus, but probably not BoE Governor Mark Carney’s expectation. Index of services rose 0.3% mom in March. BBA mortgage approvals rose to 38.0k in April.

German Ifo stopped declining trend

German Ifo business climate rose to 102.2 in May, up from 102.1 and beat expectation of 102.0. Expectations gauge dropped to 98.5, down fro 98.7, met consensus. Current assessment gauge rose to 106.0, up from 105.7, beat expectation of 105.5.

Ifo President Clemens Fuest noted in the release that “the declining trend in the ifo Business Climate has stopped.” And, “the current business survey and other indicators point to economic growth of 0.4 percent in the second quarter.”

North Korea’s response to Trump’s “sudden and unilateral” cancellation of summit with Kim

North Korean Vice Foreign Minister Kim Kye Gwan responded today to the Trump’s pull out from the June 12 summit in a statement carried by state media. Kim said that Trump’s “sudden and unilateral” announcement to cancel the summit is unexpected. And she added that “we cannot but feel great regret for it”. Kim also noted North Korea remained open to dialogue with the US “regardless of ways at any time”. Also, “the first meeting would not solve all, but solving even one at a time in a phased way would make the relations get better rather than making them get worse.” And, the US should “ponder over it”.

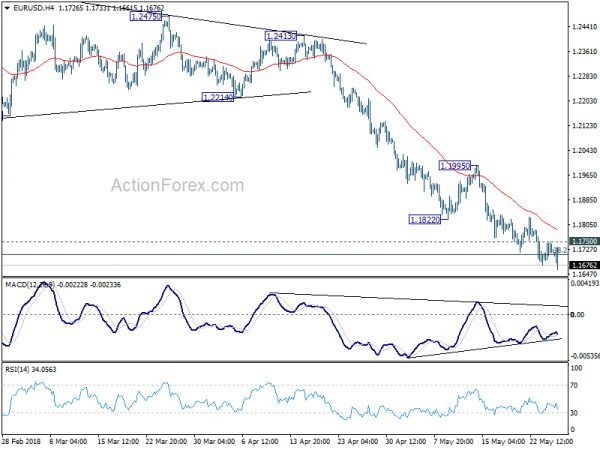

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1691; (P) 1.1720 (R1) 1.1750; More…..

EUR/USD’s decline is still in progress and reaches as low as 1.1661 so far. Intraday bias remains on the downside and the fall from 1.2555 should extend to 50% retracement of 1.0339 to 1.2555 at 1.1447 next. On the upside, above 1.1750 minor resistance will turn intraday bias neutral first. Further break of 1.1822 support turned resistance will indicate short term bottoming and bring lengthier consolidation.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will pave the way to 61.8% retracement at 1.1186. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2049) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y May | 0.50% | 0.60% | 0.60% | |

| 08:00 | EUR | German IFO Business Climate May | 102.2 | 102 | 102.1 | |

| 08:00 | EUR | German IFO Expectations May | 98.5 | 98.5 | 98.7 | |

| 08:00 | EUR | German IFO Current Assessment May | 106 | 105.5 | 105.7 | |

| 08:30 | GBP | BBA Loans for House Purchase Apr | 38.0K | 37.5K | 37.6K | |

| 08:30 | GBP | Index of Services 3M/3M Mar | 0.30% | 0.30% | 0.40% | 0.50% |

| 08:30 | GBP | GDP Q/Q Q1 P | 0.10% | 0.10% | 0.10% | |

| 12:30 | USD | Durable Goods Orders Apr P | -1.70% | -1.40% | 2.60% | |

| 12:30 | USD | Durables Ex Transportation Apr P | 0.90% | 0.50% | 0.10% | |

| 14:00 | USD | U. of Mich. Sentiment May F | 98.8 | 98.8 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals