Euro recovers broadly today as markets digest the over-stretched decline. Negative sentiments over Italian political turmoil recedes mildly as there is revived hope of a non-anti-euro government. Italy 10 year yield pull back below 3% handle while German bund yields is back above 0.35 at the time of writing. But it should be noted that German-Italian spread remains above 250bps, suggesting much nervousness among investors. Nonetheless, the common is also supported by a batch of robust economic data. In particular, German CPI accelerated much more than expected in May and that should ease some of ECB policymakers’ worries.

Dollar, on the other hand is broadly pressured together with the Japanese yen. Markets won’t forget that the US is in trade tension with many other countries/regions, even its own allies. NAFTA talk is going nowhere and there is no positive news regarding trade talk with EU. The steel tariff temporary exemption is going to expire on Friday and retaliations from Canada, Mexico and the EU are waiting on the line. Trump also made an about turn and issued a strong statement regarding China yesterday, indicating very little intention to carry on with negotiation. Or at least, trade war is suddenly back on after US put it on hold for just two weeks.

BoC is widely expected to keep interest rate unchanged at 1.25% today. Given the uncertainty around NAFTA, steel tariffs and the upcoming auto tariffs, the central is unlikely to give any hint on the timing of the next hike. Governor Stephen Poloz possibly doesn’t have a clue himself too.

– advertisement –

Quick update: BoC stands pat and maintains interest rate unchanged at 1.25% as widely expected. The most important part of the statement is that “developments since April further reinforce Governing Council’s view that higher interest rates will be warranted to keep inflation near target.” This is more hawkish than generally expected and shows that BoC is rather confident to continue with tightening, even though the timing of the next hike is still uncertain. Full statement here.

Five-Star is finding a point of compromise for economy minister

Reuters reported that a source close to the anti-establishment 5-Star Movement that it’s trying to find “a point of compromise on another name” as economy minister. The rejection by President Sergio Mattarella on anti-euro Paolo Savona as economy minister triggered this week’s political turmoil. If 5-Star can find someone acceptable by pro-Euro Mattarella, with far-right League or not, there is a possibility of finally forming a government. And it should be recalled while being highly critical, 5-Star has never committed themselves to leaving Euro. And its leader Luigi Di Maio said they never sought to leave the Euro via facebook comments earlier this week.

Prime Minister-designate Carlo Cottarelli is currently the technocrat that’s supposed to lead the government until a new election. He also said that “new possibilities have emerged for the birth of a political government.” And, “these circumstances, also considering the market tensions, have caused me to wait for further developments.”

On the other hand, League leader Matteo Salvini poured cold water on the notion and urged another election. He said, “the earlier we vote the better because it’s the best way to get out of this quagmire and confusion.” The news that anti-euro League is not interested, but is pushing for election again is also sentiment supportive.

German CPI accelerated to 2.2%, unemployment rate hit record low

Data from Eurozone are generally positive today. German CPI accelerated to 0.5% mom, 2.2% yoy in May, up from 0.0% mom, 1.6% yoy, and beat expectation of 0.3% mom, 1.9% yoy. Retail sales rose much more than expected by 2.3% mom in April versus consensus of 0.5% mom. Import price index rose 0.6%, below expectation of 0.7% mom.

German unemployment dropped -11k in May. Unemployment rate dropped to 5.2%, hitting the lowest level on record since reunification in 1990. Labour Office head Detlef Scheele said in a statement that “unemployment and underemployment have decreased again, employment within the scope of the social security system keeps rising and labour demand is still high.” And, “the upward trend on the labour market is continuing, albeit at a slower pace than in the winter months.”

Eurozone business climate rose to 1.45 in May, up from 1.39 and beat expectation of 1.30. Economic confidence dropped to 112.5, down from 112.7 but beat expectation of 112.0. Industrial confidence dropped to 16.8, down from 7.3 but met expectation. Services confidence dropped to 14.3, down from 14.7 but met expectation. Consumer confidence was finalized at 0.2.

French GDP was the main disappointment as it’s revised down to 0.2% qoq in Q1, down from 0.3% qoq. But that’s considered the “past” already.

For Q2, the set German data are rather robust and should ease much concerns of ECB policy makers, in particular the CPI figure.

Swiss KOF dropped to 100, back at long term average

Swiss KOF economic barometer dropped to 100 in May, down from 103.3 and missed expectation of 104.7. KOF noted that the Barometer is back at its “long-term average after over two years of above average values”. And that “indicates a normalization of economic development”. The decline was “mainly driven by the negative development of the indicators for manufacturing and the construction sector.”

Dollar receives no special support from a batch of mixed data.

ADP report showed private sector jobs grew 178k in May, below expectation of 190k. Prior month’s figure was also revised down from 204k to 163k. Q1 GDP growth was revised down from 2.3% to 2.2% qoq. GDP price index was revised down from 2.0% to 1.9%. Wholesale inventories rose 0.0% versus expectation of 0.5% in April. Trade deficit narrowed slightly to USD -68.2B, from USD -68.3B.

From Canada, IPPI rose 0.5% mom in April while RMPI rose 0.7% mom. Current account deficit widened to CAD -19.5B in Q1. Focus will turn to BoC rate decision.

China warns to take resolute and forceful measures if Trump insists on being arbitrary and reckless

Chinese Foreign Ministry spokeswoman Hua Chunying responded to the strong US statement released yesterday. She said “we urge the United States to keep its promise, and meet China halfway in the spirit of the joint statement.” In addition, Hua warned to take “resolute and forceful” measures to protect its interests if Trump insists on being “arbitrary and reckless” She added that “when it comes to international relations, every time a country does an about face and contradicts itself, it’s another blow to, and a squandering of, its reputation.”

The White House issued strong worded statement regarding trade relationship with China yesterday. From a fact sheet titled “President Donald J. Trump is Confronting China’s Unfair Trade Policies“, it’s said that “China has consistently taken advantage of the American economy with practices that undermine fair and reciprocal trade.” And it accused that “China has aggressively sought to obtain technology from American companies and undermine American innovation and creativity.” Simultaneously, there’s another statement outlining the Steps to Protect Domestic Technology and Intellectual Property from China’s Discriminatory and Burdensome Trade Practices.

OECD projects G20 2018 growth to be 4.0%

In the latest economic outlook report released today, OECD projects 2018-19 global growth to be at around 3.8% while G20 growth would be 4.0%. It noted in the release that “the global economy is experiencing stronger growth, driven by a rebound in trade, higher investment and buoyant job creation, and supported by very accommodative monetary policy and fiscal easing.”

However, OECD also warned of “significant risks posed by trade tensions, financial market vulnerabilities and rising oil prices loom large”. And it urged that “more needs to be done to secure a strong and resilient medium-term improvement in living standards.”

OECD Secretary-General Angel Gurria said that “the economic expansion is set to continue for the coming two years, and the short-term growth outlook is more favourable than it has been for many years.” However, “the current recovery is still being supported by very accommodative monetary policy, and increasingly by fiscal easing”. Hence, “strong, self-sustaining growth has not yet been attained.”

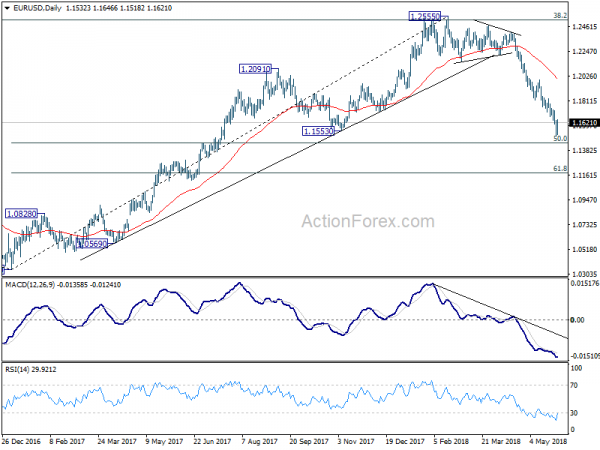

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1485; (P) 1.1563 (R1) 1.1616; More…..

Breach of 1.1639 minor resistance indicates temporary bottoming in EUR/USD at 1.1509. Intraday bias is turned neutral for consolidation. Stronger recovery could be seen to 4 hour 55 EMA (now at 1.1700) and possibly above. But upside should be limited by 1.1822/1995 resistance zone to bring fall resumption. Below 1.1509 will target 50% retracement of 1.0339 to 1.2555 at 1.1447 first. break will target 61.8% retracement at 1.1186 next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 1.1995 resistance holds..

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:00 | NZD | RBNZ Financial Stability Report | ||||

| 22:45 | NZD | Building Permits M/M Apr | -3.70% | 14.70% | 13.00% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y May | -1.10% | -1.00% | ||

| 23:50 | JPY | Retail Trade Y/Y Apr | 1.60% | 0.90% | 1.00% | |

| 01:30 | AUD | Building Approvals M/M Apr | -5.00% | -3.00% | 2.60% | 3.50% |

| 05:00 | JPY | Consumer Confidence May | 43.8 | 43.9 | 43.6 | |

| 06:00 | EUR | German Retail Sales M/M Apr | 2.30% | 0.50% | -0.60% | |

| 06:00 | EUR | German Import Price Index M/M Apr | 0.60% | 0.70% | 0.00% | |

| 06:45 | EUR | French GDP Q/Q Q1 P | 0.20% | 0.30% | 0.30% | |

| 07:00 | CHF | KOF Leading Indicator May | 100 | 104.7 | 105.3 | 103.3 |

| 07:55 | EUR | German Unemployment Change May | -11K | -10K | -7K | -8K |

| 07:55 | EUR | German Unemployment Claims Rate May | 5.20% | 5.30% | 5.30% | |

| 09:00 | EUR | Eurozone Business Climate Indicator May | 1.45 | 1.3 | 1.35 | 1.39 |

| 09:00 | EUR | Eurozone Economic Confidence May | 112.5 | 112 | 112.7 | |

| 09:00 | EUR | Eurozone Industrial Confidence May | 6.8 | 6.8 | 7.1 | 7.3 |

| 09:00 | EUR | Eurozone Services Confidence May | 14.3 | 14.3 | 14.9 | 14.7 |

| 09:00 | EUR | Eurozone Consumer Confidence May F | 0.2 | 0.2 | 0.2 | |

| 12:00 | EUR | German CPI M/M May P | 0.50% | 0.30% | 0.00% | |

| 12:00 | EUR | German CPI Y/Y May P | 2.20% | 1.90% | 1.60% | |

| 12:15 | USD | ADP Employment Change May | 178K | 190k | 204k | 163K |

| 12:30 | CAD | Current Account Balance Q1 | -19.50B | -$18.15b | -$16.35b | |

| 12:30 | CAD | Industrial Product Price M/M Apr | 0.50% | 0.60% | 0.80% | |

| 12:30 | CAD | Raw Materials Price Index M/M Apr | 0.70% | 2.10% | ||

| 12:30 | USD | Wholesale Inventories M/M Apr P | 0.00% | 0.50% | 0.30% | |

| 12:30 | USD | GDP Annualized Q/Q Q1 S | 2.20% | 2.30% | 2.30% | |

| 12:30 | USD | GDP Price Index Q1 S | 1.90% | 2.00% | 2% | |

| 12:30 | USD | Advance Goods Trade Balance Apr | -68.2B | -71.2B | -68.3B | |

| 14:00 | CAD | BoC Rate Decision | 1.25% | 1.25% | ||

| 18:00 | USD | Federal Reserve Beige Book |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals