Dollar stays firm in early US session after US delivered a solid yet unspectacular GDP report. While the greenback attempts strengthen today, so far, it’s held in range against all other major currencies. There is no committed buying in Dollar up to this point. Yen is trading as the strongest for today as 10 year JGB yield closed solidly at 0.1000, up 0.0087. For the week, Canadian Dollar is the strongest one. On the other hand, Swiss Franc is the weakest one for today, following the strong rally in European stocks. But for the week, Euro is the weakest one after uninspiring ECB press conference yesterday.

Technically, USD/CHF’s break of 0.9957 minor resistance suggests that recent pull back from 1.0067 has completed. More upside is now in favor to retest 1.0067 high. GBP/USD is still having its sight on 1.3070 minor support but there is no determined selling in the pair yet. EUR/USD and AUD/USD are also staying in familiar range as recent consolidation could extend. USD/JPY and USD/CAD are both held below 111.53 minor resistance and 1.3114 minor resistance respectively. More downside is in favor in these two pairs.

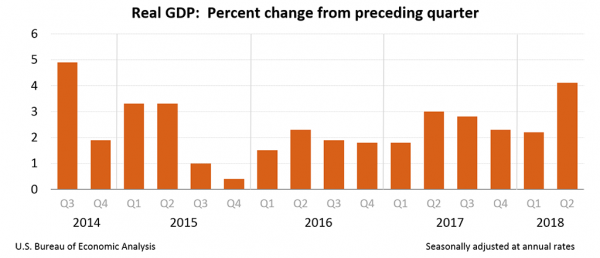

U.S. Economy Grew 4.1% Rate in Q2

US GDP grew 4.1% annualized in Q2, much better than prior quarter’s 2.0% but slightly missed expectation of 4.2%. GDP price index rose 3.0%, way above expectation of 2.3%. The growth was was highest since Q4 2014. But it’s way off the 5% finalized annual rate in Q3 2014, and can’t even match the 4.6% rate back in Q2 2014. The data is solid but unspectacular comparing to recent history.

It’s noted in the release that “The acceleration in real GDP growth in the second quarter reflected accelerations in PCE and in exports, a smaller decrease in residential fixed investment, and accelerations in federal government spending and in state and local spending.” But “these movements were partly offset by a downturn in private inventory investment and a deceleration in nonresidential fixed investment. Imports decelerated.”

Professionals revised up inflation forecast in ECB survey

ECB released the latest Survey of Professional Forecasters (SPF) today. On Eurozone inflation, SPF respondents raised their headline HICP inflation forecast to 1.7% in 2018 (from 1.5%) , 1.7% in 2019 (from 1.6%) and 1.7% in 2010 (unchanged). They now matched Eurosystem staff projection of 1.7% through 2018 to 2020.

On Core HICP inflation, SPF projections were unchanged at 1.2% in 2018, 1.5% in 2019 and 1.7% in 2020. That compares to Eurosystem staff forecasts of 1.1% in 2018, 1.6% in 2019 and 1.9% in 2020. That is, SPF respondents expect faster pickup in core inflation in 2018 but the slowed the rise slows quickly.

On growth, SPF respondents revised down GDP forecast to 2.2% in 2018 (from 2.4%), 1.9% in 2019 (from 2.0%) and 1.6% in 2020 (unchanged). That compares to Eurosystem staff projections of 2.1% in 2018, 1.9% in 2019 and 1.7% in 2020.

Majority of British voters want a referendum on the final Brexit deal

According to a YouGov poll for the Times, 42% British voters would like to have a referendum on the final terms of Brexit deal with the EU. Only 40% said there should not be, and the rest didn’t know.

Among the votes, 58% of labor supporters, 67% of Lib-dem supporters and 21% of Conservative supported wanted a second referendum on the terms.

In the event of another referendum on Brexit tomorrow, 45% said they would vote to remain, 42% would vote to leave, 4% wouldn’t vote and 9% said they didn’t know.

It’s a poll of 1653 adults in the UK conducted on Wednesday and Thursday this week.

IMF: Shift from high-speed to high-quality growth in China key for decades to come

IMF said in a report that China’s economy continues to “perform strongly”, with growth projected at 6.6% this year. But it also warned that the country is at a “historic juncture”. The shift from “high-speed” to “high-quality” growth will determine China’s “development path for decades to come”. Risk of “near-term abrupt adjustment” was reduced by recent strong growth momentum and “significant financial de-risking progress”. While there were accelerated rebalancing in some dimensions, “progress slowed” in many other dimensions. Also, while credit growth has slowed, “it remains excessive.

In the latest projections, IMF projected China GDP growth to be at 6.6% in 2018, slow to 6.4% in 2019, 6.3% in 2020, 6.0% in 2021, 5.7% in 2022 and 5.5% in 2023. Current account surplus as to GDP is projected to be at 0.9% in 2019, to close to 0.8% in 2019, at 0.8% in 2020, then slow to 0.7% in 2021, 0.5% in 2022 and 0.4% in 2023.

IMF also summarized the report in six charts. – China’s strong GDP growth continues. – A focus on high-quality growth. – Credit growth has slowed but remains too fast. – China, a global digital leader. – Rebalancing efforts should be accelerated. -6. The benefits of faster reform.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9899; (P) 0.9925; (R1) 0.9942; More…

USD/CHF’s rebound and break of 0.9957 minor resistance suggests that pull back from 1.0067 has completed at 0.9900. More importantly, the actions from 0.9787 maintain a higher-low, higher-high pattern and near term bullishness is retained. Intraday bias is back on the upside for retesting 1.0067 first. Break will resume whole rally from 0.9186.

In the bigger picture, as long as 0.9787 support holds, we’re still favoring the bullish case. That is, rise fro 0.9787 is resuming the whole up trend from 0.9186 and should target 1.0342 key resistance on resumption. However, break of 0.9787 will indicate medium term reversal and turn outlook bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Jul | 0.80% | 0.70% | 0.70% | |

| 01:30 | AUD | PPI Q/Q Q2 | 0.30% | 0.60% | 0.50% | |

| 01:30 | AUD | PPI Y/Y Q2 | 1.50% | 1.70% | ||

| 05:30 | EUR | French GDP Q/Q Q2 A | 0.20% | 0.30% | 0.20% | |

| 12:30 | USD | GDP Annualized Q/Q Q2 A | 4.10% | 4.20% | 2.00% | |

| 12:30 | USD | GDP Price Index Q2 A | 3.00% | 2.30% | 2.20% | |

| 14:00 | USD | U. of Mich. Sentiment Jul F | 97.1 | 97.1 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals