Canadian Dollar remains firm on the USMCA trade deal but it’s waiting for fresh stimulus to extend rally against Dollar and Yen. Australian Dollar is also steady after RBA stands pat and published a neutral statement as widely expected. Meanwhile, Euro is suffering some fresh selling on persistent worries over Italy, which is heading for a budget clash with EU for sure. Sterling also turned mixed after another Brexit rumor faded without follow up news.

Overnight, DOW closed up 0.73% at 26551.21 after the USMCA news. But that came after hitting as high as 26737.98 and paring much gain. Similarly, S&P 500 hit as high as 2937.06 but ended up only 0.36% at 2924.59. Nasdaq closed down -09.11% at 8037.30. Treasury yield actually showed a bit more strength as 10 year yield rose 0.024 to 3.080 after hitting day high at 3.086. 30 year yield was strongly and added 0.035 to 3.232. Again, yield was stronger at the longer end. In Asia, Japanese Nikkei is trading up 0.46%, extending medium term up trend. However, Singapore Strait Times is down -0.19% at the time of writing. Hong Kong HSI is worse, down -1.64%. China remains on holiday.

Technically, Yen is regaining some strengthen in Asian session after rebound in EUR/JPY and GBP/JPY lost steam. Recent consolidation in two crosses is set to extend. Dollar is picking up some strength against Euro, Swissy, Sterling and Aussie as markets enter into European session. We’d probably see EUR/USD have a take on 1.1525 support and USD/CHF on 0.9866 resistance. GBP/USD’s recovery overnight was rather weak and brief and it should revisit 1.2999 temporary low soon.

RBA left cash rate unchanged at 1.50%, maintained neutral stance

The accompanying statement is very much a carbon copy of the prior one. A change is in noting the cause of pickup in global inflation on higher oil prices and wage growth. And further pickup is expected on tightening labor markets and the sizeable fiscal stimulus of the US. But RBA also reiterated that risk to global outlook from “direction of international trade policy in the United States.”

Domestically, RBA said latest data confirmed strong growth in the past year. And GDP is expected to average a bit above 3% in 2018 and 2019. Meanwhile, “one continuing source of uncertainty is the outlook for household consumption. Labor market outlook remains “positive” and lift in wage growth will be a “gradual process”. Inflation is expected to decline in September quarter due to once-off factors, but should climb to above 2% in 2019 and 2020.

Overall, the RBA maintained a neutral stance with the statement and hinted again that it’s in no rush to rate hike.

EU Juncker: One crisis in Greece was enough, not another in Italy

European Commission President Jean-Claude Juncker said yesterday that “Italy is distancing itself from the budgetary targets we have jointly agreed at EU level.” He warned “one crisis was sufficient, one crisis was enough” and “after the toughest management of the Greece crisis, we have to do everything to avoid a new Greece — this time an Italy — crisis.” He added “we have to prevent Italy from being able to get a special treatment here that, if everybody were to get it, would mean the end of the euro.”

The chairman of Eurozone finance ministers Mario Centeno said after the group’s meeting that “recent announcements by the Italian government have raised concerns over its budgetary course, concerns that need to be addressed soon.” He added “we are all bound by the euro and we need sound policies to protect it. It is up to the Italian government to show it has a sustainable and credible budgetary plan.”

On the other hand, Italian Deputy Prime Minister Luigi Di Maio insisted the government “will never sacrifice workers on the altar of the spread and of the crazy rules which have been imposed on us” And, “this government doesn’t butcher people, the music has changed.”

Fed Rosengren sees yellow lights in inflation, Kashkari sees bond flashing yellow too

Boston Fed President Eric Rosengren warned that tight labor market could push the economy towards unexpected inflation and other problems. He argued that Fed should continuing rate hikes “until monetary policy becomes mildly restrictive.”

And he emphasized that “the further we get from full employment the further risk there is.” Also, he added “pushing the economy too hard risks inflationary concerns or financial-stability risks”. Either of these outcomes “might necessitate a more forceful monetary policy response.”

While there are no “alarm going off” for now, he said “there are a bunch of yellow lights”. these include commercial housing estate boom that could push prices beyond what market demand could sustain.

On the other hand, Minneapolis Fed President Neel Kashkari saw “flashing yellow” signals in the bond market, which suggested there is no need for any more rate hikes for now. He said “the bond market is saying, ‘hey we’re not so sure that the U.S. economic growth is going to be very strong in the future years,’ so that’s a nervousness for me.”

Kashkari added yield curve is “a measure of giving us feedback as to are we running accommodative monetary policy or contractionary monetary policy, and I don’t see any reason yet that we should be moving interest rates up and tapping the brakes.”

IMF Lagarde hinted at global outlook downgrade on trade disputes

IMF Managing Director Christine Lagarde hinted yesterday that the organization may downgrade growth outlook next week. She said, “In July, we projected 3.9 percent global growth for 2018 and 2019. The outlook has since become less bright, as you will see from our updated forecast next week.”

Lagarde added “A key issue is that rhetoric is morphing into a new reality of actual trade barriers. This is hurting not only trade itself, but also investment and manufacturing as uncertainty continues to rise.” Though she also tried to tone down and said “we are not seeing broader financial contagion — so far — but we also know that conditions can change rapidly. If the current trade disputes were to escalate further, they could deliver a shock to a broader range of emerging and developing economies.”

On WTO reform, she said “The immediate challenge is to strengthen the rules. This includes looking at the distortionary effects of state subsidies, preventing abuses of dominant positions and improving the enforcement of intellectual property rights.”

On the data front

Japan monetary base rose 5.9% yoy in September versus expectation of 5.4% yoy. Consumer confidence rose 0.1 to 43.4 in September. UK will release construction PMI today while Eurozone will release PPI.

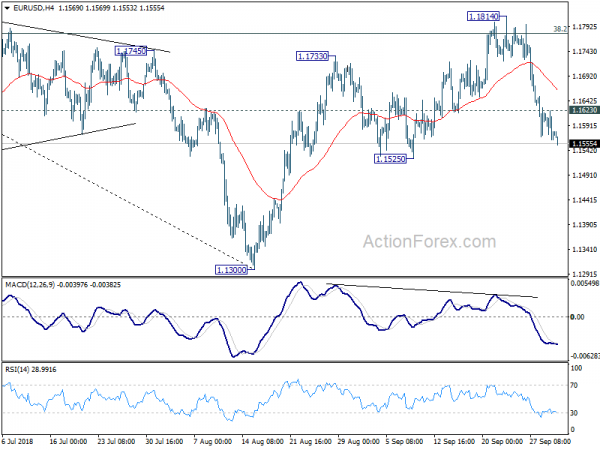

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1552; (P) 1.1588; (R1) 1.1616; More…..

EUR/USD’s fall from 1.1814 continues today and reaches as low as 1.1553 so far. Intraday bias remains on the downside for 1.1525 support. Decisive break there will confirm that corrective rise from 1.1300 has completed at 1.1814. In such case, deeper fall should be seen back to retest 1.1300. On the upside, above 1.1650 minor resistance will turn intraday bias neutral and bring recovery. But upside should be limited well below 1.1814 to bring fall resumption.

In the bigger picture, a medium term bottom should be in place at 1.1300, on bullish convergence condition in daily MACD and some consolidations would be seen. But still, note that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. That carries some long term bearish implications. Thus, we’d expect fall from 1.2555 high to resume after consolidation completes. Below 1.1300 should send EUR/USD through 61.8% retracement of 1.0339 to 1.2555 at 1.1186. And, in that case, EUR/USD would head to retest 1.0339 (2017 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Sep | 5.90% | 5.40% | 6.90% | |

| 4:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 5:00 | JPY | Consumer Confidence Index Sep | 43.4 | 43.4 | 43.3 | |

| 8:30 | GBP | Construction PMI Sep | 52.6 | 52.9 | ||

| 9:00 | EUR | Eurozone PPI M/M Aug | 0.00% | 0.40% | ||

| 9:00 | EUR | Eurozone PPI Y/Y Aug | 3.90% | 4.00% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals