The finance markets turned mixed in Asian session today. Yen was sold off overnight, following the strong rebound in US treasury yields. In particular 30-year yield staged the biggest rise in a about a month and looks completed the consolidation from 3.109. But there is no follow through selling in Yen so far. Nevertheless, Yen remains the weakest one for the week. Sterling is the strongest one on fading risk of no-deal Brexit.

While the events in the past 24 hours were rather high profile, little reactions were triggered. USTR Robert Lighthizer’s testimony on China trade talk, Fed Chair Jerome Powell’s testimony and Trump-Kim summit in Vietnam are shrugged off. Swiss Franc was briefly shot up by Pakistan-India tensions but there was no follow through buying. Markets could be awaiting Q4 GDP from the US for the next move.

Technically, Sterling aside, direction in the forex markets is not clear. Dollar weakened this week against Euro, and Swissy but downside momentum looks to be diminishing. USD/JPY and EUR/JPY remains bounded in tight range. AUD/USD and USD/CAD are also staying in familiar range too. Again, US GDP could be the trigger for breakouts.

In Asia, Nikkei is down -0.35%. Hong Kong HSI is up 0.10%. China Shanghai SSE is down -0.35%. Singapore Strait Times is down -0.57%. Japan 10-year JGB yield is up 0.0002 at -0.024. Overnight, DOW dropped -0.28%. S&P 500 dropped -0.05%. NASDAQ rose 0.07%. 10-year yield rose 0.057 to 2.693. 30-year yield rose 0.063 to 3.069.

USTR Lighthizer: Market outcomes to determine winners, not state-capitalism and technology theft

In his testimony to House Ways and Means Committee on China trade negotiation, US Trade Representative Robert Lighthizer laid down the principle that the US “can compete with anyone in the world”. But he emphasized “we must have rules, enforced rules”. And “market outcomes” rather than “state-capitalism” and “technology theft” determine winners. China’s unfair trade practices are “major threats to our economy”.

Lighthizer said there were “very intense, extremely serious, and very specific negotiation with China on crucial structural issues for several months” and “real progress” were made. US could “turn the corner” in the economic relationship with China “if” they can reach a satisfactory solution to the all-important outstanding issue of enforceability as well as some other concerns. But “much still needs to be done” before an agreement is reached, and “more importantly, after it is reached.”

He also emphasized that the administration is “pressing for significant structural changes” rather than “soybean solution”. The US is “very aware of ” the history with China and the “disappointments that have resulted from promises that were not kept” And, “the reality is this is a challenge that will go on for a long, long time.” He added that “if there is disagreement at my level, the U.S. would expect to act proportionately but unilaterally.”

Meanwhile, as the agreements are settlements of China’s violations of Section 301 of the Trade Act of 1974. So they are executive actions that do not require Congress’ approval. China talks are more in common with a sanctions-monitoring regime than a traditional trade pact.

Fed Powell: Balance runoff likely settles at around 16-17% of GDP

In the second day of Congressional Testimony, Fed Chair Jerome Powell said Fed will stop the balance sheet runoff this year. The balance sheet will then be at around 16-17% of GDP, up from 6% before the financial crisis. Considering that the US GDP is currently at around USD 20T, the balance sheet would eventually be between USD 3.2T and USD 3.4T. The Balance sheet is currently just over USD 4T.

Powell said “we’ve worked out, I think, the framework of a plan that we hope to be able to announce soon that will light the way all the way to the end of balance sheet normalization”. And, “we going to be in a position … to stop runoff later this year.”

He also bluntly noted that Fed is “not looking at a higher inflation target, full stop”, even if Fed is rethinking its policy framework for this year.

China PMI manufacturing dropped to 49.2, new export orders hit decade low

The official China PMI manufacturing dropped to 49.2 in February, down from 49.5 and missed expectation of 49.5. That’s the third straight month of sub-50 reading. Looking at the details new export orders index dropped -1.7 to 45.2, its lowest level in 10 years, suggesting trade war with the US continues to have an impact on exports. Production dropped -1.4 to 49.5. Employment dropped -0.3 to 47.5. PMI services dropped to 54.3, down from 54.7, missed expectation of 54.5.

However, analyst Zhang Liqun tried to talk down the deterioration in the statement. He noted that the decline in PMI was mainly due to Lunar New Year factor. He pointed to the significant decline in the production, the purchase volume, and the raw material inventory as indications.

Also from Asia, Japan industrial production dropped -3.7% mom in January versus expectation of -2.5% yoy. Japan retail sales rose 0.6% yoy in January, below expectation of 1.5% yoy.

ANZ business confidence dropped to -30.9, RBNZ to cut in November

New Zealand ANZ Business Confidence dropped to -30.9 in February, down from -24.1. Activity Outlook dropped to 10.5, down fro 13.6. ANZ noted that recent improvement in business activity stalled. Export intentions fell to the weakest since March 2009. Pricing intentions remain range-bound.

ANZ also noted that “Clearly the economy is stretched at the moment, but it does appear that momentum has waned markedly over the last six months.” And it expects RBNZ to become “less certain that core inflation will continue rising towards the midpoint of the target band”. ANZ forecasts a cut in OCR in November.

Also from down under, Australia private capital expenditure rose 2.0% in Q4 versus expectation of 1.0%. Private sector credit rose 0.2% mom in January versus expectation of 0.3% mom.

Looking ahead

The calendar is rather busy today. Swiss will release GDP and KOF. Germany will release import price and CPI. France will release GDP. Later in the day, US will finally release Q4 GDP. jobless claims and Chicago PMI will be featured. Canada will release current account, IPPI and RMPI.

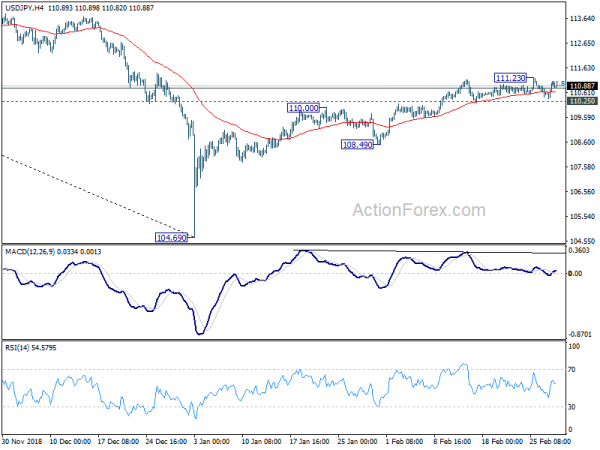

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.53; (P) 110.81; (R1) 111.26; More…

USD/JPY recovered ahead of 110.25 minor support but upside is held below 111.23 resistance. Intraday bias remains neutral first. On the downside, break of 110.25 minor support will suggest rejection by 61.8% retracement of 114.54 to 104.69 at 110.77. And in that case, the rebound from 104.69 has likely completed. Intraday bias will be turned back to the downside for 108.49 support for confirmation. Nevertheless, firm break of 111.23 should confirm resumption of rise from 104.69 for 114.54 resistance.

In the bigger picture, while the rebound from 104.69 was stronger than expected, it’s struggle to get rid of 55 day EMA completely. Outlook is turned mixed first. On the downside, break of 108.49 support will revive that case that such rebound was a correction. And, larger down trend is still in progress for another low below 104.62. But sustained trading above 55 day EMA will turn focus to 114.54. Decisive break there will confirmation completion of the decline from 118.65 (2016 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jan P | -3.70% | -2.50% | -0.10% | |

| 23:50 | JPY | Retail Trade Y/Y Jan | 0.60% | 1.50% | 1.30% | |

| 00:00 | NZD | ANZ Business Confidence Feb | -30.9 | -24.1 | ||

| 00:01 | GBP | GfK Consumer Confidence Feb | -13 | -15 | -14 | |

| 00:30 | AUD | Private Capital Expenditure Q4 | 2.00% | 1.00% | -0.50% | 0.00% |

| 00:30 | AUD | Private Sector Credit M/M Jan | 0.20% | 0.30% | 0.20% | |

| 01:00 | CNY | Manufacturing PMI Feb | 49.2 | 49.5 | 49.5 | |

| 01:00 | CNY | Non-manufacturing PMI Feb | 54.3 | 54.5 | 54.7 | |

| 05:00 | JPY | Housing Starts Y/Y Jan | 10.30% | 2.10% | ||

| 06:45 | CHF | GDP Q/Q Q4 | 0.40% | -0.20% | ||

| 07:00 | EUR | German Import Price Index M/M Jan | 0.20% | -1.30% | ||

| 07:45 | EUR | French GDP Q/Q Q4 P | 0.30% | 0.30% | ||

| 08:00 | CHF | KOF Leading Indicator Feb | 96 | 95 | ||

| 13:00 | EUR | German CPI M/M Feb P | 0.50% | -0.80% | ||

| 13:00 | EUR | German CPI Y/Y Feb P | 1.50% | 1.40% | ||

| 13:30 | CAD | Current Account Balance Q4 | -$14.01b | -$10.34b | ||

| 13:30 | CAD | Industrial Product Price M/M Jan | 0.30% | -0.70% | ||

| 13:30 | CAD | Raw Materials Price Index M/M Jan | 4.10% | 3.80% | ||

| 13:30 | USD | Initial Jobless Claims (FEB 23) | 221K | 216K | ||

| 13:30 | USD | GDP Annualized Q/Q Q4 A | 2.50% | 3.40% | ||

| 13:30 | USD | GDP Price Index Q4 A | 1.70% | 1.80% | ||

| 14:45 | USD | Chicago PMI Feb | 57.8 | 56.7 | ||

| 15:30 | USD | Natural Gas Storage | -177B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals