Cross-border instant payments are transforming how money moves around the world. This comprehensive guide explains what cross-border instant payments are, how they work, who the key players are, and what the future holds for real-time global transactions in 2026 and beyond.

1. What Are Cross-Border Instant Payments?

Cross-border instant payments are real-time international money transfers that settle within seconds or minutes, rather than the traditional 1–5 business days. They represent a fundamental shift in how value moves across borders, enabled by modern payment infrastructure and technology.

Unlike traditional cross-border payments that rely on correspondent banking networks and batch processing, instant payments use real-time settlement systems that provide immediate confirmation and finality. This means that funds are available to the recipient almost instantly, with full transparency and tracking throughout the transaction lifecycle.

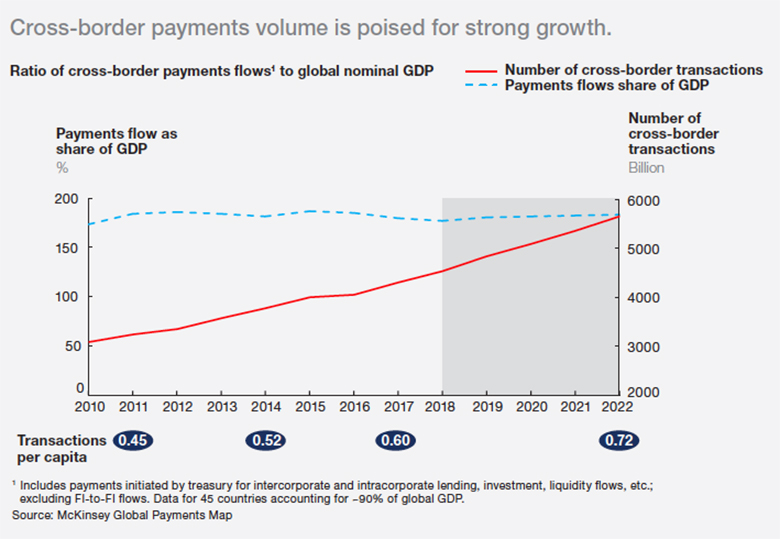

The global push toward instant cross-border payments has accelerated significantly in recent years, driven by consumer demand for faster transfers, competition from fintech companies, and central bank initiatives to modernise payment systems. As of 2026, over 70 countries operate domestic instant payment systems, and efforts to connect these systems internationally are gaining momentum.

📌 Key Definition: Cross-border instant payments are real-time international transactions that settle within seconds or minutes, offering speed, transparency, and lower costs compared to traditional wire transfers.

2. How Do Cross-Border Instant Payments Work?

Cross-border instant payments rely on a combination of advanced payment infrastructure, messaging standards, and connectivity between domestic payment systems. The technology behind these payments has evolved significantly over the past decade.

Key components of cross-border instant payment infrastructure:

- SWIFT GPI (Global Payments Innovation): SWIFT’s initiative to improve cross-border payments with end-to-end tracking, faster settlement, and transparency. As of 2026, over 4,000 financial institutions have adopted SWIFT GPI, which processes approximately 50% of all SWIFT cross-border payments.

- SEPA Instant: The Single Euro Payments Area Instant system enables real-time payments within Europe, with 36 countries participating and 24/7/365 availability.

- FedNow: The US Federal Reserve’s instant payment service launched in 2023, providing real-time settlement for US domestic payments and a foundation for future cross-border connectivity.

- ISO 20022: The global standard for financial messaging that enables richer data in payments, improving automation and straight-through processing.

The technology stack includes:

- API integration: Application Programming Interfaces allow banks and fintechs to connect payment systems seamlessly

- Interlinking: Connecting domestic instant payment systems across borders to enable real-time cross-border transfers

- Distributed ledger technology: While still emerging, blockchain-based solutions are being explored for settlement efficiency

- Artificial intelligence: AI is increasingly used for fraud detection, compliance screening, and transaction routing optimisation

💡 How It Works: A cross-border instant payment typically flows through multiple layers: the sender’s bank → domestic payment system → SWIFT GPI or correspondent banking → destination payment system → recipient’s bank. Each step is optimised for real-time processing and full transparency.

3. Key Players in Cross-Border Instant Payments

The cross-border instant payments ecosystem is diverse, comprising traditional banks, fintech companies, payment networks, and technology providers. Each plays a distinct role in enabling real-time global transactions.

Traditional Banks

JPMorgan Chase, Deutsche Bank, Bank of America, and Citi are among the leading banks investing heavily in real-time payment infrastructure. They leverage their extensive correspondent banking networks and SWIFT GPI connectivity to offer faster cross-border services to corporate and retail clients. These institutions bring trust, scale, and regulatory compliance to the ecosystem.

Fintech Companies

Wise (formerly TransferWise), WorldRemit, Payoneer, and Revolut have disrupted the cross-border payments market by offering faster, cheaper transfers using innovative business models. They aggregate demand, leverage local payment systems, and use API connectivity to provide near-instant transfers at lower costs than traditional banks.

Payment Networks

- SWIFT: The global messaging network that connects over 11,000 financial institutions worldwide. SWIFT GPI has transformed cross-border payments with real-time tracking.

- Visa Direct and Mastercard Send: Card network-based push payment solutions enabling real-time funds transfers to cards and bank accounts globally.

- The Clearing House (TCH): Operator of the RTP network in the US, providing real-time settlement for domestic payments.

📌 Market Insight: The competition between traditional banks and fintechs has accelerated innovation in cross-border payments. Banks are modernising their infrastructure, while fintechs are building new networks from the ground up. Both approaches are contributing to the global shift toward instant payments.

4. Benefits of Cross-Border Instant Payments

Cross-border instant payments offer significant advantages over traditional international transfers. These benefits are driving adoption across businesses, financial institutions, and consumers.

- ⚡ Speed: Transactions settle in seconds or minutes instead of days. Funds are available to recipients almost immediately, eliminating the waiting period that has long been a frustration in cross-border payments.

- 👁️ Transparency: Real-time tracking provides full visibility into the transaction lifecycle. SWIFT GPI’s tracking feature, for example, allows senders to monitor their payment at every stage.

- 💰 Lower Costs: Instant payments reduce operational costs through automation and straight-through processing, which can lead to lower fees for end-users. Fintech-driven solutions have already demonstrated significant cost reductions.

- 📈 Improved Cash Flow: For businesses, faster settlement means better cash flow management and reduced working capital requirements. This is particularly valuable for SMEs operating across borders.

- 🔄 24/7/365 Availability: Unlike traditional payments limited to business hours, instant payment systems operate around the clock, enabling transfers at any time.

✅ Key Advantage: Cross-border instant payments eliminate the uncertainty and delay that have historically plagued international transfers. For businesses, this means faster payment cycles, improved supplier relationships, and better financial planning.

5. Challenges and Risks of Instant Cross-Border Payments

Despite their benefits, cross-border instant payments face significant challenges that must be addressed for widespread adoption. Understanding these challenges is essential for businesses and financial institutions planning to leverage real-time payments.

- 🏦 Liquidity Management: Real-time settlement requires banks to maintain sufficient liquidity to settle payments instantly. This can be challenging, especially for smaller institutions and during volatile market conditions.

- 🛡️ Fraud and Compliance: The speed of instant payments makes fraud detection and anti-money laundering (AML) screening more challenging. Transactions must be screened in real-time, requiring advanced AI and machine learning capabilities.

- 📋 Regulatory Differences: Cross-border payments must navigate different regulatory regimes, including data privacy laws, sanctions screening, and currency controls. These differences can create friction and complexity.

- 🔧 Infrastructure Limitations: Not all countries have instant payment systems, and those that do often operate with different technical standards. Interlinking these systems is a complex and resource-intensive process.

- ⏳ Patchy Global Coverage: While over 70 countries have domestic instant payment systems, the connectivity between these systems is still limited. True global coverage remains a work in progress.

⚠️ Important: The transition to instant cross-border payments requires significant investment in technology, compliance, and liquidity management. Financial institutions must balance the benefits of speed with the risks of fraud and regulatory non-compliance.

6. Cross-Border Instant Payments Trends 2026

The landscape of cross-border instant payments is evolving rapidly. Several key trends are shaping the future of real-time global transactions in 2026 and beyond.

- 🌍 Interlinking of National Systems: Efforts to connect domestic instant payment systems across borders are accelerating. The BIS (Bank for International Settlements) is actively working on cross-border payment connectivity, and projects like Project Nexus are demonstrating the feasibility of interlinking multiple systems.

- 🤖 AI and Automation: Artificial intelligence is increasingly used for fraud detection, compliance screening, and transaction routing. AI-powered systems can screen instant payments in milliseconds, enabling real-time compliance without delaying transactions.

- 📊 ISO 20022 Adoption: The migration to ISO 20022 messaging standards is enabling richer data in payments, improving straight-through processing and enabling new use cases such as invoice reconciliation and supply chain finance.

- 🔗 SWIFT GPI Evolution: SWIFT continues to enhance GPI with new features, including payment pre-validation and case resolution. Over 4,000 financial institutions now use GPI.

- 💳 CBDC Integration: Central Bank Digital Currencies (CBDCs) are being explored for cross-border payments. China’s e-CNY and other CBDC projects are testing cross-border use cases that could further accelerate instant payments.

- 📱 Fintech Innovation: Fintech companies continue to push the boundaries of speed and cost, with some offering near-instant transfers at a fraction of traditional bank fees. Competition is driving innovation across the entire ecosystem.

📊 Market Outlook: Industry analysts project continued growth in cross-border instant payments, with transaction volumes expected to increase significantly by 2030. The convergence of technology, regulation, and consumer demand is creating a powerful tailwind for real-time global payments.

7. Cross-Border Instant Payments Reference Table

Use this reference table to quickly understand key terms, compare payment systems, and identify key players in the cross-border instant payments ecosystem.

Part 1: Key Terms & Definitions

Part 2: Comparison of Payment Systems

| Feature | SWIFT GPI | SEPA Instant | FedNow |

|---|---|---|---|

| Region | Global (200+ countries) | Europe (36 countries) | United States |

| Settlement Speed | Minutes to hours | Seconds | Seconds |

| Launched | 2017 | 2017 | 2023 |

| Key Feature | End-to-end tracking | 24/7/365 availability | Fed-backed real-time settlement |

Part 3: Key Players Comparison

| Player Type | Examples | Key Strengths | Weaknesses |

|---|---|---|---|

| Traditional Banks | JPMorgan, Deutsche Bank, BofA, Citi | Trust, compliance, scale, existing networks | Slower innovation, higher costs |

| Fintechs | Wise, WorldRemit, Payoneer, Revolut | Speed, low cost, user experience | Limited reach, regulatory challenges |

| Payment Networks | SWIFT, Visa Direct, Mastercard Send | Global infrastructure, reliability | Legacy systems, slower evolution |

Part 4: Pros and Cons

| Pros ✅ | Cons ❌ |

|---|---|

| Near-instant settlement (seconds vs days) | Requires significant infrastructure investment |

| Full transparency with real-time tracking | Cross-border regulatory differences |

| Lower transaction costs | Liquidity management challenges |

| Improved cash flow for businesses | Fraud and compliance risks |

| 24/7/365 availability | Patchy global coverage |

Part 5: Quick Reference Checklist

8. Frequently Asked Questions (FAQ)

What are cross-border instant payments?

Real-time international payments that settle within seconds or minutes, using modern payment infrastructure and technology to enable faster, more transparent transactions.

How do cross-border instant payments differ from traditional transfers?

Traditional transfers take 1-5 business days to settle and offer limited tracking. Instant payments settle in seconds with full transparency and end-to-end tracking.

What is SWIFT GPI?

SWIFT’s Global Payments Innovation — a service that enables faster, more transparent cross-border payments with end-to-end tracking and pre-validation of payment details.

What is SEPA Instant?

The Single Euro Payments Area Instant system enables real-time payments within Europe, with 36 countries participating and 24/7/365 availability.

Which countries have instant payment systems?

Over 70 countries now operate domestic instant-payment systems, including the US (FedNow), Europe (SEPA Instant), the UK (Faster Payments), Australia (NPP), and Singapore (FAST).

What are the benefits of instant cross-border payments?

Speed, transparency, lower costs, improved cash flow for businesses, and 24/7/365 availability are the key benefits driving adoption.

What are the main challenges?

Liquidity management, fraud prevention, regulatory differences between jurisdictions, infrastructure costs, and patchy global coverage.

How is technology changing cross-border payments?

AI, API integration, ISO 20022 messaging standards, and blockchain are driving innovation in real-time payments, enabling faster processing, better compliance, and lower costs.

What is the future of cross-border instant payments?

Increased interlinking of national systems, wider adoption of ISO 20022, integration of AI for fraud detection, and potentially CBDC integration for cross-border transactions.

How can businesses benefit from instant cross-border payments?

Faster settlement, better cash flow visibility, reduced transaction costs, improved supplier relationships, and enhanced customer experience through faster delivery of goods and services.

9. Conclusion: The Future of Cross-Border Instant Payments

Cross-border instant payments are no longer a vision for the future — they are a reality that is transforming how money moves around the world. With over 70 countries now operating domestic instant payment systems and initiatives like SWIFT GPI, SEPA Instant, and FedNow gaining momentum, the infrastructure for real-time global payments is rapidly maturing.

Key takeaways from this guide:

- ✅ Cross-border instant payments settle in seconds or minutes, compared to days for traditional transfers

- ✅ Key technologies include SWIFT GPI, ISO 20022, API integration, and AI

- ✅ Major players include traditional banks, fintechs, and payment networks

- ✅ Benefits include speed, transparency, lower costs, and 24/7 availability

- ✅ Challenges remain: liquidity, fraud, regulation, and infrastructure

- ✅ The future will see interlinking of national systems, wider adoption, and lower costs

📌 Final Advice: Cross-border instant payments are transforming global commerce. Whether you are a business owner, financial professional, or individual, understanding this technology is essential for staying competitive in an increasingly connected world. Stay informed, evaluate the options, and embrace the future of real-time payments.

Continue your financial education — explore the guides below to deepen your understanding of trading, technical analysis, and payment systems.

📚 Further Reading

Explore these guides to deepen your understanding of technical analysis, trading strategies, and financial markets:

- 200-Day Moving Average: Complete Guide & Trading Strategies Learn how to use the 200-day moving average as a trend filter, dynamic support and resistance, and in crossover strategies like the Golden Cross and Death Cross. Essential knowledge for identifying long-term trends in forex and stock markets.

- Top 8 Forex Trading Strategies: Pros, Cons & Timeframes Compare the 8 most popular forex trading strategies — from scalping to position trading. Discover which strategy matches your trading style, time availability, and risk tolerance. Includes detailed analysis of each strategy with pros, cons, and key indicators.

- What Is Forex Trading? — Understanding the Global Currency Market Master the basics of forex trading — the world’s largest financial market. Learn about currency pairs, pips, leverage, and how the global currency market operates.

- Free Expert Advisors (EAs) — Automate Your Forex Trading Automate your forex trading with our collection of free Expert Advisors. Save time, eliminate emotional decisions, and execute trades with precision and consistency.

📞 Need Help? Contact Us

Our support team is ready to assist you with any questions about forex trading, technical analysis, or our products and services.

📌 Support Hours: Our team is available 24/5 via WhatsApp, Telegram, and Live Chat. We respond to all inquiries within 24 hours on business days.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals