Dollar trades broadly lower in relatively quiet markets today. Trading is rather subdued firstly due to quarter end effect. More importantly, traders are awaiting the highly anticipated Trump-Xi meeting. It’s cautiously optimistic that some form of agreement would be made to avert further tariff escalations. But this is far from being certain.

Staying in the currency markets, Australian Dollar is the second weakest for today, then Yen. Sterling is the strongest, followed by Swiss Franc and Euro. Over the week, Yen is the weakest one, followed by Sterling, and then Dollar. Commodity currencies are broadly higher, led by New Zealand Dollar.

In Europe, FTSE is up 0.27%. DAX is up 0.53%. CAC is up 0.40%. German 10-year yield is down -0.001 at -0.319. Earlier in Asia, Nikkei dropped -0.29%. Hong Kong HSI dropped -0.28%. China Shanghai SSE dropped -0.60%. Singapore Strait Times dropped -0.21%. Japan 10-year JGB yield dropped -0.213 to -0.163.

Trump denies six-month reprieve on new China tariffs

Ahead of tomorrow’s meeting with Chinese President Xi Jinping, Trump denied today on offering Xi a six-month reprieve on new tariffs. He expected the meeting to “productive” at a minimum, but didn’t elaborate further. Xi, on the hand, warned of “bullying practices” in his remarks to African leaders. And he said “any attempt to put one’s own interests first and undermine others’ will not win any popularity”, without directly mentioning Trump’s “America First” policies.

Japan & US agreed to speed up trade negotiation, but no time frame assigned

Japan Economy Minister Toshimitsu Motegi said US and Japan agreed to speed up trade negotiations. He noted that after meeting US Trade Representative Robert Lighthizer in Osaka as sideline of G20 leaders summit. Working level meetings will be held starting next month, towards a bilateral trade agrement.

However, Motegi also said there is no time frame for completing the deal. He said noted “we share understanding of each other’s thinking and stance and where our gap lies. Based on that, we are discussing ways to narrow our differences.”

US personal income rose 0.5%, spending rose 0.4%, core PCE unchanged at 1.6%

In May, US personal income rose 0.5% or USD 88.6B, above expectation of 0.3%. Personal spending rose 0.4% or USD 59.7B, below expectation of 0.5%. Headline PCE deflator slowed to 1.5% yoy, down from 1.6 yoy but matched expectations. Core PCE was unchanged at 1.6% yoy, also matched expectations. While core PCE inflation remained below Fed’s 2% target, there is no clear deterioration that could force Fed for an immiedate rate cut in July.

Canada GDP rose 0.3% in April, above expectation of 0.2%

Canada GDP rose 0.3% mom in April, above expectation of 0.2% mom. Goods-producing industries rose 0.4%, while services producing industries increased 0.2%. The 20 industrial sectors were nearly evenly split between gains and losses. On three-month rolling basis, GDP grew 0.3%, up from 0.1% in the three months to March.

Also from Canada, IPPI rose 0.1% mom in May versus expectation of 0.0% mom. RMPI dropped -2.3% mom, versus expectation of -3.0% mom.

Eurozone CPI unchanged at 1.2%, but core CPI jumped to 1.1%

Eurozone CPI was unchanged at 1.2% yoy in June, matched expectations. However, CPI core accelerated to 1.1% yoy, up from 0.8% yoy and beat expectation of 0.9% yoy. Looking at the main components of euro area inflation, ‘food, alcohol & tobacco’, ‘energy’ and ‘services’ are expected to have an annual rate of 1.6% in June. The annual rate of ‘non-energy industrial goods’ is expected to be 0.2%

Also released, Germana import price dropped -0.1% mom in May, above expectation of -0.2% mom.

UK Q1 GDP finalized at 0.5%, services the largest contributor

UK Q1 GDP was finalized at 0.5% qoq, 1.8% yoy, unrevised. Services output rose 0.4%, production rose 1.1% while construction rose 1.4%. Services sector provided the largest contribution to growth in the output approach to measuring GDP, while production also contributed positively, due largely to growth of 1.9% in manufacturing output. Household expenditure, government consumption and investment contributed positively to GDP growth in Quarter 1 2019, while net trade contributed negatively.

Gfk consumer confidence dropped to -13 in June, down from -10 and missed expectations of -11. Current account deficit widened to GBP -30.0B in Q1, less than expectation of GBP-32.0B.

Swiss KOF dropped to 93.6, downward tendency flattening out

Swiss KOF Economic Barometer dropped to 93.6 in June, down from 93.8 and missed expectation of 94.9. KOF said “the downward tendency that has been present since the beginning of the year is now flattening out.” But economic outlook “remains dampened” in the middle of 2019.

The almost unchanged reading is primarily due to balancing tendencies in foreign demand, the goods producing sector (manufacturing and construction) and private consumption. While indicators show a positive tendency with regard to foreign demand, the joint indicators of the goods producing sector and private consumption point in the opposite direction with almost equal magnitude. In addition, there is a slight slowdown in the banking and insurance sector.

BoJ: All policy measures should be considered if baseline scenario changes

In the summary of opinions at June 19-20 BoJ meeting, it’s noted that Japan’s economy is “likely to continue on a moderate expanding trend”. And “year-on-year rate of change in the consumer price index (CPI) is likely to increase gradually toward 2 percent”. Although “downside risks warrant attention”, it’s “appropriate” to continue with “current monetary policy stance”.

However, there was “an increase in uncertainties regarding overseas economies. US-China trade conflicts and threat of no-deal Break has “started to affect Japan’s economy and people’s sentiment”. The schedule consumption tax hike could “exert downward pressure on economic activity and prices.”

It’s argued that it’s important for BoJ to take “some kind of policy responses if some changes emerge in the baseline scenario of the outlook for prices”. And, “all policy measures — including adjustments in short- and long-term interest rates, an acceleration in the pace of expansion in the monetary base, and an increase in the amount of assets to be purchased — should be deliberated when considering additional easing.”

Additionally, it’s also argued that considering growing expectation for easing by Fed and ECB, BoJ “also needs to strengthen monetary easing”. And, “it is necessary to further consider in depth the feasibility of a wide range of additional easing measures, as well as their effects and side effects.”

Released in Asian session, Japan Tokyo CPI core slowed to 0.9% yoy in June, down from 1.1% yoy and missed expectation of 1.0% yoy. Industrial production rose 2.3% mom in May, above expectation of 0.7% mom. Unemployment rate was unchanged at 2.4% in May, matched expectations. Housing starts dropped -8.7% yoy, below expectation of -4.2% yoy. Australia private sector credit rose 0.2% mom in May, matched expectations.

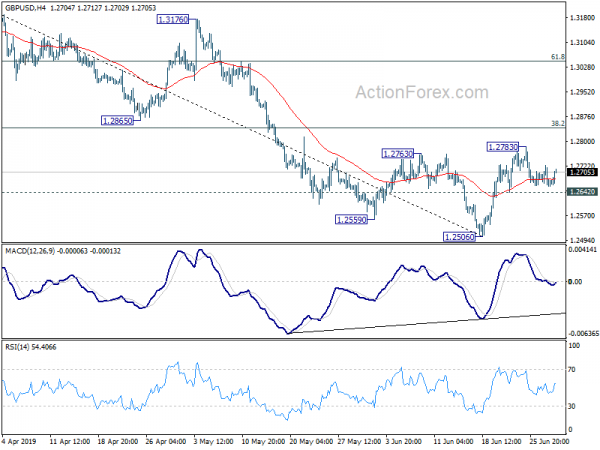

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2647; (P) 1.2686; (R1) 1.2710; More….

GBP/USD recovers mildly but stays below 1.2783 resistance. Intraday bias remains neutral first. With 1.2642 minor support intact, corrective rebound from 1.2506 could still extend higher. But upside should be limited by 38.2% retracement of 1.3381 to 1.2506 at 1.2840. On the downside, break of 1.2642 minor support will turn intraday bias back to retest 1.2506 low. However, sustained break of 1.2840 will bring stronger rise to 61.8% retracement at 1.3047 next.

In the bigger picture, down trend from 1.4376 (2018 high) is still in progress. Break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence, focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | GfK Consumer Confidence Jun | -13 | -11 | -10 | |

| 23:30 | JPY | Unemployment Rate May | 2.40% | 2.40% | 2.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jun | 0.90% | 1.00% | 1.10% | |

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M May P | 2.30% | 0.70% | 0.60% | |

| 01:30 | AUD | Private Sector Credit M/M May | 0.20% | 0.20% | 0.20% | |

| 05:00 | JPY | Housing Starts Y/Y May | -8.70% | -4.20% | -5.70% | |

| 06:00 | EUR | German Import Price Index M/M May | -0.10% | -0.20% | 0.30% | |

| 07:00 | CHF | KOF Leading Indicator Jun | 93.6 | 94.9 | 94.4 | 93.8 |

| 08:30 | GBP | GDP Q/Q Q1 F | 0.50% | 0.50% | 0.50% | |

| 08:30 | GBP | Current Account Balance (GBP) Q1 | -30.0B | -32.0B | -23.7B | |

| 09:00 | EUR | Eurozone CPI Estimate Y/Y Jun | 1.20% | 1.20% | 1.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun A | 1.10% | 0.90% | 0.80% | |

| 12:30 | CAD | GDP M/M Apr | 0.30% | 0.20% | 0.50% | |

| 12:30 | CAD | Industrial Product Price M/M May | 0.10% | 0.00% | 0.80% | |

| 12:30 | CAD | Raw Materials Price Index M/M May | -2.30% | -3.00% | 5.60% | 5.70% |

| 12:30 | USD | Personal Income May | 0.50% | 0.30% | 0.50% | |

| 12:30 | USD | Personal Spending May | 0.40% | 0.50% | 0.30% | 0.60% |

| 12:30 | USD | PCE Deflator M/M May | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | PCE Deflator Y/Y May | 1.50% | 1.50% | 1.50% | 1.60% |

| 12:30 | USD | PCE Core M/M May | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | PCE Core Y/Y May | 1.60% | 1.60% | 1.60% | |

| 13:45 | USD | Chicago PMI Jun | 54 | 54.2 | ||

| 14:00 | USD | U. of Mich. Sentiment Jun F | 97.9 | 97.9 | ||

| 14:30 | CAD | BoC Business Outlook Survey |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals