Following mild pull back in US equities overnight, Asian markets are mixed. Though, apparent weakness in China and Hong Kong stocks are dragging down Australian Dollar, which is the weakest one for today so far. Sterling is the next weakest as data showed retail sales suffered the worst June in decades. Dollar, Euro and Yen are the firmer ones. Trading in the currency markets are generally muted as focus remain on Fed Chair Jerome Powell’s testimony, which starts tomorrow. He comments will, hopefully, clear the picture on whether Fed will cut interest rates this month.

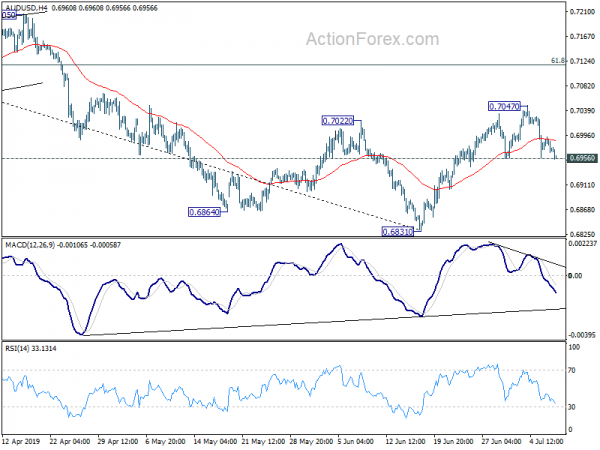

Technically, USD/JPY’s breach of 108.80 suggests near term bullish reversal. But sustained trading above this resistance is needed to confirm. AUD/USD is back pressing 0.6956 support again and firm break will confirm completion of rebound from 0.6831. USD/CAD is still bounded in tight range around 1.3052/68 cluster support. It remains to be seen if such cluster support could be defended successfully.

In Asia, currently, Nikkei is up 0.07%. Hong Kong HSI is down -0.74%. China Shanghai SSE is down -0.52%. Singapore Strait Times is up 0.04%. Japan 10-year JGB yield is up 0.0061 at -0.143. Overnight, DOW dropped -0.43%. S&P 500 dropped -0.48%. NASDAQ dropped -0.78%. 10-year yield dropped -0.014 to 2.034, staying above 2% handle.

Australia NAB Business confidence unwound post election spike

Australia NAB Business Conditions improved from 1 to 3 in June, but remain below average. Business Confidence dropped from 7 to 2, largely unwound the bounce from 0 to 7 in May. NAB said “the recent run of results also suggest that the economy is unlikely to record a significant pickup in growth in Q2.” Further, “forward orders also remain below average (and are negative), suggesting a near-term turn around in business activity is unlikely.”

According to Alan Oster, NAB Group Chief Economist, “Business confidence appears to have unwound its spike in May, which we think was driven by a short-term election bounce and increased optimism around a renewed interest rate easing cycle by the RBA. While business conditions increased slightly in the month, they remain well below average after trending lower for over a year now. The decrease in conditions has been relatively broad-based across states and industries – suggesting that there has been sector wide loss of momentum over the past year”.

UK retail sales picture bleak on Brexit uncertainty

UK BRC like-for-like sales dropped -1.6% yoy in June, below expectation of -1.5% yoy. Total sales dropped -1.3% yoy. The data were worst in record for June since 1995. Helen Dickinson, Chief Executive of BRC, noted, “overall, the picture is bleak: rising real wages have failed to translate into higher spending as ongoing Brexit uncertainty led consumers to put off non-essential purchases.”

She added: “Businesses and the public desperately need clarity on Britain’s future relationship with the EU. The continued risk of a No Deal Brexit is harming consumer confidence and forcing retailers to spend hundreds of millions of pounds putting in place mitigations – this represents time and resources that would be better spent improving customer experience and prices. It is vital that the next Prime Minister can find a solution that avoids a No Deal Brexit on 31st October, just before the busy Black Friday and Christmas periods.”

Elsewhere

Japan labor cash earnings dropped -0.2% yoy in May, better than expectation of -0.6% yoy. Japan M2 rose 2.3% yoy in June, below expectation of 2.6% yoy. Swiss will release unemployment rate in European session. Later in the day, Canada will release housing starts and building permits.

But major focus will firstly be on Fed chair Jerome Powell’s opening remarks on “stress testing” at the Federal Reserve Board Conference. Though, it’s unsure if he will save the comments on monetary policy for tomorrow’s Congressional testimony. Fed Vice Chair Randal Quarles and St. Louis Fed James Bullard will also speak.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.6963; (P) 0.6978; (R1) 0.6990; More…

Intraday bias in AUD/USD remains neutral with focus on 0.6956 minor support. Firm break there will indicate completion of the rebound from 0.6831. Intraday bias will be turned back to the downside for retesting 0.6831 low. On the upside, above 0.7047 will resume the rebound to 61.8% retracement of 0.7295 to 0.6831 at 0.7118.

In the bigger picture, with 0.7393 key resistance intact, medium term outlook remains bearish. The decline from 0.8135 (2018 high) is seen as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Jun | -1.60% | -1.50% | -3.00% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y May | -0.20% | -0.60% | -0.10% | -0.30% |

| 23:50 | JPY | Japan Money Stock M2+CD Y/Y Jun | 2.30% | 2.60% | 2.70% | 2.60% |

| 1:30 | AUD | NAB Business Conditions Jun | 3 | 3 | 1 | |

| 1:30 | AUD | NAB Business Confidence Jun | 2 | 2 | 7 | |

| 5:45 | CHF | Unemployment Rate Jun | 2.40% | 2.40% | ||

| 6:00 | JPY | Machine Tool Orders Y/Y Jun P | -27.30% | |||

| 10:00 | USD | NFIB Small Business Optimism Jun | 103.1 | 105 | ||

| 12:15 | CAD | Housing Starts Jun | 209K | 202K | ||

| 12:30 | CAD | Building Permits M/M May | 14.70% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals