Risk aversion is back in the markets after taking a breather yesterday, as there remains no sign of containment of China’s coronavirus. Yen and Swiss Franc are the strongest ones today, with Yen pressing this week’s high against other major currencies. Dollar is mixed shrugging off the non-eventful FOMC rate hold. Commodity currencies are broadly under pressure naturally. Sterling is not too far away as markets await BoE rate decision.

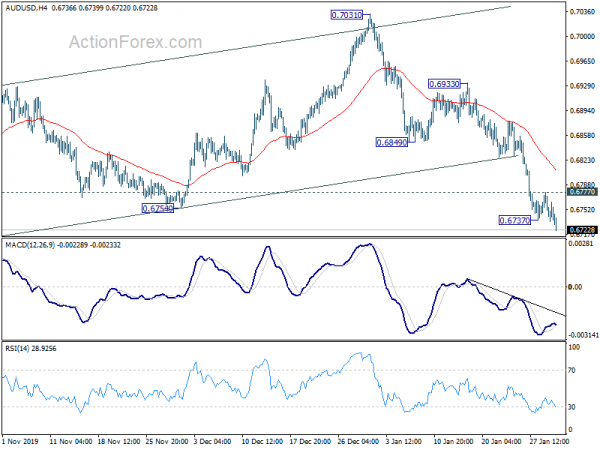

Technically, AUD/USD’s decline resumes after brief consolidation. Current fall from 0.7031 is on track to retest 0.6670 low. USD/CAD also resume rise from 1.2951 after brief consolidation, and it’s on track to 1.3327 resistance next. Both USD/JPY and EUR/JPY might quickly break through 108.73 and 119.80 temporary low too.

In Asia, Nikkei dropped -1.72%. Hong Kong HSI is down -2.37%. Singapore Strait Times is down -0.62%. China remains on holiday. Japan 10-year JGB yield is down -0.0229 at -0.059. Overnight, DOW rose 0.04%. S&P 500 dropped -0.09%. NASDAQ rose 0.06%. 10-year yield dropped -0.047 to 1.594, losing 1.6 handle.

China’s coronavirus cases jump to 7711

China’s National Health Commission reported that, as of January 29, number of confirmed coronavirus case in the country rose 1737 from 1459 to 7711. Serious cases rose from 1239 to 1370. Death toll rose from 132 to 170. Suspected cases rose from 9239 to 12167. Number of people being tracked rose from 65537 to 88693.

WHO chief Tedros Adhanom Ghebreyesus said in Geneva, “in the last few days the progress of the virus especially in some countries, especially human-to-human transmission, worries us.” “Although the numbers outside China are still relatively small, they hold the potential for a much larger outbreak.”

Fed stood pat, carefully monitoring coronavirus

Fed left interest rate unchanged at 1.50-1.75% overnight as widely expected, by unanimous vote. Chair Jerome Powell said in the post meeting press conference that current monetary stance is “appropriate”. He added that global growth stabilizing and trade uncertainties receded.

However, “uncertainties about the outlook remain, including those posed by the new coronavirus.” “China’s economy is very important in the global economy now, and when China’s economy slows down we do feel that – not as much though as countries that are near China, or that trade more actively with China, like some of the Western European countries”. He added that Fed is “very carefully monitoring the situation” regarding the coronavirus, but it’s “too early” to assess the impact.

Here are some reviews:

BoE to stand pat on a close call

BoE rate decision is a major focus today and it will be Mark Carney’s last meeting as Governor. The central bank is more likely to keep Bank rate unchanged at 0.75%. Markets are just pricing in around 45% chance for a cut as of yesterday. Bets on a cut receded sharply last week after data showed strong improvement in business optimism. But the decision would be a close call.

Here are some suggested previews:

On the data front

New Zealand trade surplus came in larger than expected at NZD 547m in December, versus expectation of NZD 110m. Australia import price index rose 0.7% qoq in Q4, above expectation of 0.4% qoq.

Looking ahead, Swiss KOF, Germany unemployment and CPI flash, Eurozone unemployment and confidence indicators, will be featured in European session. US will release Q4 GDP and jobless claims later in the day.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6732; (P) 0.6755; (R1) 0.6774; More…

AUD/USD’s decline resumes after brief consolidations and intraday bias is back on the downside. Fall form 0.7031 is expected to retest 0.6670 low next. On the upside, above 0.6777 minor resistance will turn intraday bias neutral first. But recovery should be limited below 0.6849 support turned resistance to bring another fall.

In the bigger picture, with 0.7082 resistance intact, there is no clear confirmation of trend reversal yet. That is, down trend from 0.8135 (2018 high) is still expect to continue to 0.6008 (2008 low). However, decisive break of 0.7082 will confirm medium term bottoming and bring stronger rally back to 55 month EMA (now at 0.7484).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance (NZD) Dec | 547M | 100M | -753M | -791M |

| 0:30 | AUD | Import Price Index Q/Q Q4 | 0.70% | 0.40% | 0.40% | |

| 8:00 | CHF | KOF Leading Indicator Jan | 96.5 | 96.4 | ||

| 8:55 | EUR | Germany Unemployment Change Dec | 5K | 8K | ||

| 8:55 | EUR | Germany Unemployment Rate Dec | 5% | 5% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Dec | 7.50% | 7.50% | ||

| 10:00 | EUR | Eurozone Economic Sentiment Jan | 102 | 101.5 | ||

| 10:00 | EUR | Eurozone Business Climate Jan | -0.26 | -0.25 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Jan | -9 | -9.3 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Jan | -8.1 | -8.1 | ||

| 10:00 | EUR | Eurozone Services Sentiment Jan | 12.2 | 11.4 | ||

| 12:00 | GBP | BoE Rate Decision | 0.75% | 0.75% | ||

| 12:00 | GBP | BoE Asset Purchase Target Jan | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 0–3–6 | 0–2–7 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | ||

| 13:00 | EUR | Germany CPI M/M Jan P | -0.70% | 0.50% | ||

| 13:00 | EUR | Germany CPI Y/Y Jan P | 1.70% | 1.50% | ||

| 13:30 | USD | Initial Jobless Claims (Jan 24) | 218K | 211K | ||

| 13:30 | USD | GDP Annualized Q4 P | 2.10% | 2.10% | ||

| 13:30 | USD | GDP Price Index Q4 P | 1.90% | 1.80% | ||

| 15:30 | USD | Natural Gas Storage | -92B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals