Asian markets went wild today, on the back of acceleration in coronavirus spread in Europe, as well as free falling oil on price war. Sentiments have never been hit that had for quite some time. Commodity currencies, as led by Australian Dollar, are the biggest casualties in the massive selloff. Yen and Swiss, to a slightly lesser extent Euro, record strong gains on safe haven flow. Dollar and Sterling are somewhat stuck in between. Gold struggles to gain and sustain above 1700 handle.

Technically, the spikes break in AUD/USD and NZD/USD should be disregarded first. Focus remains on 0.6433 in AUD/USD and 0.6191 in NZD/USD. Firm break of these levels will confirm down trend resumption. AUD/JPY and NZD/JPY, however, are viewed slightly differently as both has resumed medium term down trend. Meanwhile, 1.1456 fibonacci resistance in EUR/USD and 0.8786 resistance in EUR/GBP will be the strong tests for the persistence of Euro’s rally.

In Asia, currently, Nikkei is down -5.64%. Hong Kong HSI is down -3.65%. China Shanghai SSE is down -2.73%. Singapore Strait Times is down -4.62%. Japan 10-year JGB yield is down -0.0289 at -0.175. DOW future is down over -1200 pts.

Economic data are taking a back seat today and will continue to do so for the retest of the day. Japan Q1 GDP contracted more than expected by -1.8% qoq. Bank lending rose 2.1% yoy in February versus expectation of 1.9% yoy. Currenct account surplus narrowed to JPY 1.63T in January. Swiss unemployment rate, Germany industrial production and trade balance, Eurozone Sentix investor confidence will released in European session. Canada will release housing starts and building permits.

Coronavirus spreading quickly in Europe, new cases in China and South Korea slow

Coronavirus in situation China, the origin of the global outbreak, continues to stabilize, with just 40 new cases and 22 deaths reported for Sunday. Total accumulated cases now stands at 80738, with 3120 deaths. New cases in South Korea also slowed some what, as total stands at 7382 with 53 deaths. Italy (7375 cases, 366 deaths) and Iran (6566 cases, 194 deaths) are quickly catching up and will likely surpass South Korea very soon.

Situation in Europe is very worrying with 1209 cases in France, 1040 in Germany, 674 in Spain, 332 in Swiss, 278 in UK, 265 in the Netherlands, 203 in Sweden, 200 in Belgium, 176 in Norway, 104 in Austria. US, with 554 cases, will be the next point of focus regarding the coronavirus spread.

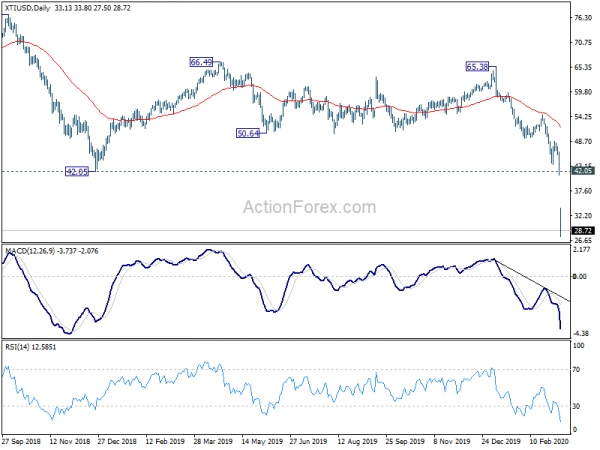

Oil price in worst decline since 90s on price war

Oil price is having the worst loss since Gulf War in 1991, on fear of price war after OPEC+ talks ended in dramatic failure. It’s reported that Saudi Arabia wanted to slash production to offset the steep decrease in demand due to coronavirus pandemic. But Russia rejected the idea, arguing that cheap crude will help wipe out competition from US shale.

As the talks collapsed, it’s reported that Saudi Arabia plans to boost output next month to well above 10 million barrels a day, or even to 12 million barrels. That’s seen as an act of a full price war between OPEC and Russia, to force the latter to go back to the negotiation table.

WTI crude oil hits as low as 27.50 today, breaching 2016 low of 27.69. At this point, we’re not expecting sustainable trading below 27.69 yet, unless the situation worsen dramatically. There is prospect of a rebound should Russia comes back to negotiation. But any rebound attempt will likely be capped below prior resistance at 42.05.

AUD/JPY slaughtered again in thin panic market, still heading to 60 anyway

AUD/JPY suffered another wild ride in thin, panic, early Asian session again today. It’s a move that resembles what happened early last year. On January 3, 2013, AUD/JPY hit as low as 70.2 (depending which chart you’re reading), but recovered strongly to close at 76.05. The fate of the cross, however, will likely be different considering the material risks the world is facing.

From a technical point of view, outlook with remain bearish as long as 71.50 resistance holds. 100% projection of 80.71 to 69.96 from 76.54 at 65.78 will remain the focus after today’s “false break”. Sustained trading below this level will pave the way to 161.8% projection at 59.13.

That will coincide with 100% projection of 102.83 to 72.39 from 90.29 at 59.85, as well as 60 round number. We’d expect enough support only from there to bring sustainable rebound.

ECB rate decision as a focus this week

ECB rate decision is the major focus in a relatively light week. There are speculations that the central bank would cut deposit rate by -0.10%, in response to coronavirus risks in Eurozone. Yet, with deposit already at -0.50%, it’s rather unsure if any further cut would be effect, not to mention that it might do more harm than good. Hence, some believed that ECB could opt for targeted liquidity measures to help the companies affected by the outbreak.

UK will also be another focus with GDP, productions and trade balance featured. These batch of January data would review how well the economy rebounded after eliminating election risk totally. Meanwhile, there are speculations that BoE could deliver an emergency policy action, ahead of the regular meeting the week after.

Here are some highlights for the week:

- Monday: Japan Q4 GDP final, current account; Swiss unemployment rate; Germany industrial production, trade balance; Eurozone Sentix investor confidence; Canada housing starts, building permits.

- Tuesday: Australia NAB business confidence; China CPI, PPI; Japan machine tool orders; France industrial production, Italy industrial production; Eurozone Q4 GDP revision, employment change.

- Wednesday: Australia Westpac consumer sentiment; UK GDP, productions, trade balance; US CPI.

- Thursday: Japan BSI manufacturing, PI; UK RICS house price balance; Eurozone industrial production, ECB rate decision, US PPI, jobless claims.

- Friday: New Zealand BusinessNZ manufacturing; Japan tertiary industry index; German CPI final; US import prices, U of Michigan sentiment.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3389; (P) 1.3414; (R1) 1.3449; More….

USD/CAD breaks through 1.3464 resistance decisively today and hits as high as 1.3761 so far. Near term outlook will remain bullish as long as 1.3464 resistance turned support holds. Further rally should be seen to 161.8% projection of 1.2951 to 1.3329 from 1.3202 at 1.3814 next.

In the bigger picture, price actions from 1.3664 (2018 high) are seen as a corrective move that has completed at 1.2951. Rise from 1.2061 (2017 low) should be ready to resume. Decisive break 1.3664 will target 61.8% projection of 1.2061 to 1.3664 from 1.2951 at 1.3941 next. For now, this will remain the favored case as long as 1.3202 support holds, in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Feb | 2.10% | 1.90% | 1.90% | |

| 23:50 | JPY | GDP Q/Q Q4 | -1.80% | -1.70% | -1.60% | |

| 23:50 | JPY | GDP Deflator Y/Y Q4 | 1.20% | 1.30% | 1.30% | |

| 23:50 | JPY | Current Account (JPY) Jan | 1.63T | 1.66T | 1.71T | 1.85T |

| 5:00 | JPY | Eco Watchers Survey: Current Feb | 27.4 | 35.6 | 41.9 | |

| 6:45 | CHF | Unemployment Rate Feb | 2.30% | 2.30% | ||

| 7:00 | EUR | Germany Industrial Production M/M Jan | 1.50% | -3.50% | ||

| 7:00 | EUR | Germany Trade Balance (EUR) Jan | 18.8B | 19.2B | ||

| 9:30 | EUR | Eurozone Sentix Investor Confidence Mar | -11 | 5.2 | ||

| 12:15 | CAD | Housing Starts Feb | 205.0K | 213.2K | ||

| 12:30 | CAD | Building Permits M/M Jan | 2.30% | 7.40% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals