Markets are rather quiet in Asia today. Nikkei is pressured after poor trade data from Japan. But movements in other major Asian centers are muted. New Zealand Dollar appears to be lifted by the country’s plan to exit top level lockdown. Dollar is currently the second strongest. On the other hand, Canadian dollar is the weakest one as oil price extends decline. Yen is the second weakest so far.

Technically, though, there is no new development. A focus today would be 1.4182 in USD/CAD. Break will revive the case that correction 1.4667 has completed and pave the way to retest this high at a later stage. As for AUD/USD, break of 0.6213 resistance turned support will suggest that rebound from 0.5506 has completed and target 0.5979 support for confirmation. 1.0768 in EUR/USD is a level to watch too, as break will bring 1.0635 low into focus.

In Asia, currently, Nikkei is down -1.06%. Hong Kong HSI is up 0.05%. China Shanghai SSE is up 0.23%. Singapore Strait Times is flat. Japan 10-year JGB yield is up 0.0029 at 0.019.

Japan exports slumped in March as coronavirus hit

In non-seasonally adjusted terms, Japan’s exports dropped a massive -11.7% yoy in March while imports dropped -5.0% yoy. Trade surplus came in at just JPY 4.95B. The contraction in export was the worst since July 2016 as shipments to major destinations like China, US and EU were choked by the coronavirus pandemic. The impact will likely continue in April and onwards until global lockdown exits. In seasonally adjusted terms, exports dropped -4.1% mom while imports rose 7.2% mom. Trade balanced turned into JPY -0.19T deficit.

Separately, Reuters reported that the government is going to boost its economic rescue package by 8% to JPY 117. A major change is inclusion of JPY 100k cash payout for to every citizen, on top of JPY 300k payout to households affected by the pandemic. The government is also planning to issue extra bonds worth JPY 25.7T to fund the revised budget.

New Zealand CPI accelerated, but RBNZ core CPI slowed

New Zealand CPI rose accelerated to 0.8% qoq in Q1, up from Q4’s 0.5% qoq, well above expectation of 0.3% qoq. Annual inflation rate rose to 2.5% yoy, highest since 2011. Impact of coronavirus pandemic was not much reflected in the data yet as lockdown measures started on March 25. Separately released, RBNZ’s own core CPI measures slowed to 1.7% yoy in Q1, down from 1.8% yoy.

Separately, New Zealand Prime Minister Jacinda Ardern announced today that the country will “move out of Alert Level 4 lockdown at 11.59 p.m. on Monday April 27, one week from today”. Afterwards, “we will then hold in Alert Level 3 for two weeks, before reviewing how we are tracking again, and making further decisions at Cabinet on the 11th of May.”

RBA Lowe: We shouldn’t be worried about government borrowing

RBA Governor Philip Lowe told ABC News that the coronavirus pandemic was “going to be perhaps a once-in-a-lifetime event” and it “required a truly extraordinary response”. “I didn’t think in my term of governor, I’d be buying AUD 40 billion of government bonds, which we’ve done in the past few weeks and lending over AUD 100 billion to the banking system.”

Lowe also noted that there shouldn’t be concern on escalating government debt. “If ever there’s a time to borrow, now is it,” he said. “We shouldn’t be worried” about the debt. “We have the capacity to borrow, our interest rates are as low as they’ve ever been, the Australian government has a long record of responsible fiscal policy, so the budget accounts are in reasonable shape,” he added.

Zew, Ifo and PMIs to highlight the week

Confidence and sentiments indicators are the major focuses this week. Germany ZEW investor confidence and Ifo business climates will be featured. Eurozone, UK, US, Australia and Japan will release PMIs. Other data, while important, might take a back seat for the moment. Those include inflation data from UK, Canada and Japan, or pre-coronavirus pandemic data like UK employment and Canada retail sales.

Here are some highlights for the week:

- Monday: New Zealand CPI; Japan trade balance; Germany PPI; Eurozone current account, trade balance; Canada wholesale sales.

- Tuesday: RBA minutes; Swiss trade balance; UK employment; German ZEW; Canada retail sales; US existing home sales.

- Wednesday: UK CPI, PPI; Canada CPI, new housing price index; Eurozone consumer confidence; US house price index.

- Thursday: Australia PMIs; Japan PMI manufacturing; Germany Gfk consumer sentiment; Eurozone PMIs; UK PMIs, public sector net borrowing, CBI industrial orders; US jobless claims, PMIs, new home sales.

- Friday: Japan CPI, all industry index; UK retail sales; Germany Ifo business climate; US durable goods orders.

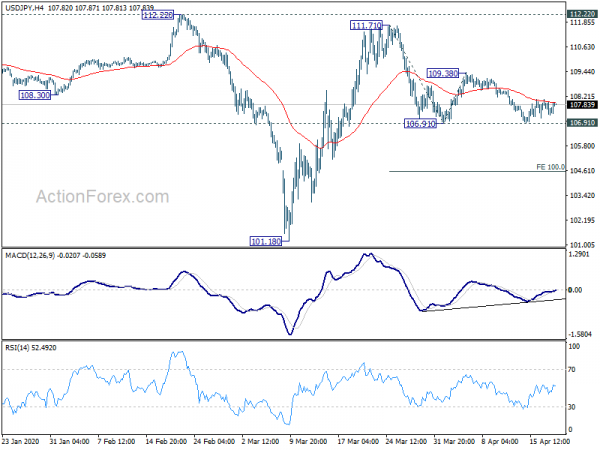

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.21; (P) 107.64; (R1) 107.99; More…

USD/JPY recovers mildly today but upside is capped by 4 hour 55 EMA so far. Intraday bias remains neutral for the moment. On the downside, break of 106.91 will extend the decline from 111.71 to 100% projection of 111.71 to 106.91 from 109.38 at 104.58. On the upside, break of 109.38 will suggest that fall from 111.71 has completed. Intraday bias will be turned back to the upside for 111.71/112.22 resistance zone.

In the bigger picture, at this point, whole decline from 118.65 (Dec 2016) continues to display a corrective look, with well channeling. There is no clear sign of completion yet. Break of 101.18 will target 98.97 (2016 low). Meanwhile, sustained break of 112.22 should confirm completion of the decline and turn outlook bullish for 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q1 | 0.80% | 0.30% | 0.50% | |

| 23:01 | GBP | Rightmove House Price Index M/M Apr | -0.20% | 1.00% | ||

| 23:50 | JPY | Trade Balance (JPY) Mar | -0.19T | -0.11T | 0.50T | 0.48T |

| 6:00 | EUR | Germany PPI M/M Mar | -0.10% | -0.40% | ||

| 6:00 | EUR | Germany PPI Y/Y Mar | 0.20% | -0.10% | ||

| 8:00 | EUR | Eurozone Current Account (EUR) Feb | 36.3B | 34.7B | ||

| 9:00 | EUR | Eurozone Trade Balance (EUR) Feb | 19.2B | 17.3B | ||

| 12:30 | CAD | Wholesale Sales M/M Feb | -0.20% | 1.80% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals