U.S. Highlights

- Following a four-week losing streak, U.S. financial markets regained some gusto, buoyed by optimism on the prospect of a new stimulus package.

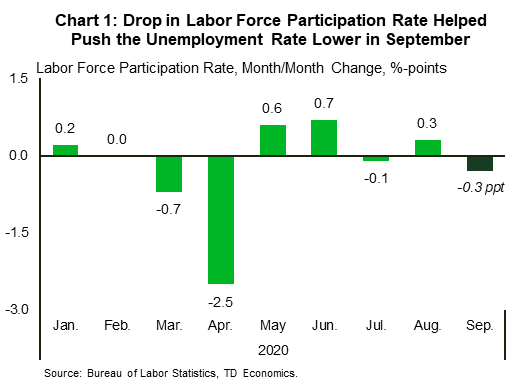

- The labor market continues to mend, albeit at a decelerating pace. The American economy added 661,000 payroll jobs in September, down from 1.5 million in August. Meanwhile, the unemployment rate fell to 7.9%, in part because of a pullback in the labor force participation rate.

- The House passed a $2.2 trillion coronavirus relief bill this week, but it will not pass the Senate. Talks between Speaker Pelosi and Treasury Secretary Mnuchin continue, but a deal has yet to be reached.

Canadian Highlights

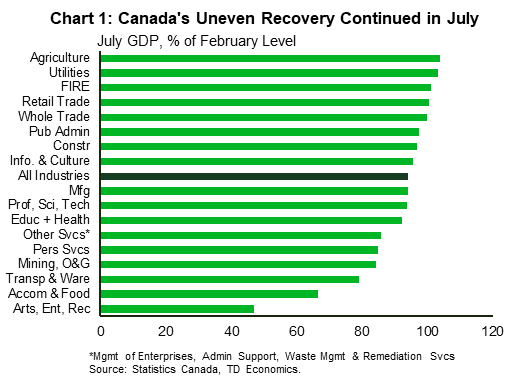

- GDP expanded by 3.0% m/m in July, bringing further confirmation that the economy continues to recover from its pandemic-induced plunge. However, progress is slowing (StatCan estimated a 1.0% m/m gain took place in August), and the recovery is uneven across industries.

- The continued rise in COVID-19 cases made headlines this week, prompting industry closures in Quebec and putting pressure on Ontario to do the same.

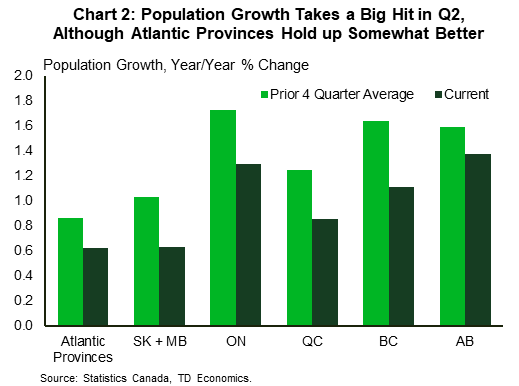

- Canada’s population expanded by only 25k in the second quarter, compared to 176k during the same period last year. A decline in the number of non-permanent residents in Canada was the main drag.

U.S. – Healing, but Slowing Labor Market

Following a four-week losing streak, financial markets regained some gusto, buoyed by optimism on the prospect of a new stimulus package. Sentiment soured late in the week however, as news broke that President Trump and the first lady tested positive for COVID-19. Still, the S&P 500 is on track to end the week about 2% above last week’s close (as of writing).

The release of employment data for the month of September was this week’s main economic highlight. The report showed ongoing, albeit decelerating progress in the labor market recovery. Indeed, 661,000 payroll jobs were added last month, down from 1.5 million in August. Overall, 51.5% of non-farm payrolls lost since the pandemic began have been recovered. The unemployment rate fell from 8.4% to 7.9% in September, a welcome improvement, but a markedly slower pace than in previous months. More concerning, the drop was due in large part to a pullback in the labor force participation rate (Chart 1) rather than strength in job growth.

The theme of a stalling labor market recovery was also borne out in the jobless claims data. Indeed, new filings for unemployment benefits have held stubbornly close to the 900,000 per week mark since the end of August, signaling that businesses continue to lay off workers at an elevated rate. While continuing claims have trended lower over the past few weeks, they remain well above pre-crisis levels.

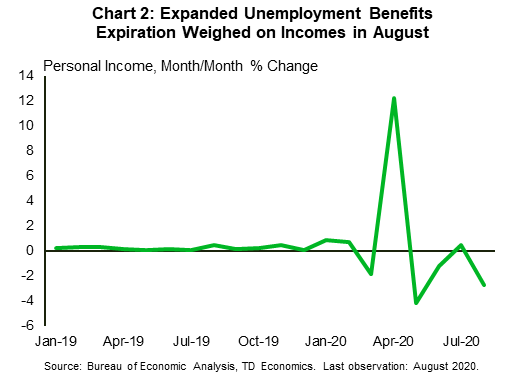

Unfortunately, as the $600/week federal unemployment top-up expired at the end of July, many people saw their income take a big hit in August. In fact, a 52% decline in unemployment benefits resulted in personal income falling by 2.7% month/month in August (Chart 2). While personal spending continued to make up lost ground, advancing by 1.0% on the month, the decline in incomes poses a downside risk to the recovery. What is more, spending on durable goods, which powered the early rebound in consumption, is showing signs of fatigue, while the recovery in services spending is also slowing. The latter is now in jeopardy due to a resurgence in new coronavirus cases.

Similar concerns were echoed in the September ISM Manufacturing report. The Index registered a worse-than-expected 0.6 point retreat to 55.4, pointing to a slower pace of expansion in the manufacturing sector. The details of the report showed a recovery that remains uneven, with a slew of industries continuing to contend with sluggish demand.

On a more positive note, new vehicles sales soared by 7.6% month/month in September to 16.3 million units. Alongside home sales, auto sales are one of the few economic indicators to have exhibited a “V-shaped” recovery and are now within 2.5% of their pre-crisis level from February.

All things considered, the balance of risks to the economic outlook remains tilted to the downside. The absence of a new stimulus package is beginning to take a toll on the recovery. Talks between House Speaker Pelosi and Treasury Secretary Mnuchin continued this week, but a deal has, so far, remained out of reach. Here’s hoping that Democrats and Republicans can close the gap and come to an agreement sooner rather than later.

Canada – Grinding It Out

This week brought confirmation that the Canadian economy continued to recover from its pandemic-induced depths during the summer months. However, the recovery appears to be unfolding in an uneven manner across industries, and momentum is slowing as output moves past the initial burst brought on by re-opening and the release of pent-up demand. The next leg of the recovery is likely to be much more of a grind.

In financial markets, news of President Trump’s positive COVID-19 diagnosis sent stocks lower, including the TSX, on Friday. This same factor, alongside broader demand concerns, weighed on WTI prices, which were down around 6% as of writing.

The marquee data event for the week was the July GDP report. Real GDP expanded by 3.0% (m/m) in July, matching Statistics Canada’s advance estimate and bringing output to within 6% of its February level (i.e before widespread industry shutdowns). As encouraging as these developments were, July’s expansion was the slowest of the recovery yet. In addition, StatCan’s advance estimate of a 1.0% m/m gain suggests that growth downshifted even further in August. Moreover, while a handful of industries managed to surpass February output levels in July, and others came closer, there remains several sectors that are struggling to gain any sustained traction (Chart 1). The pandemic has decimated the “high-touch” sectors of transportation/warehousing, accommodation and food services, arts, entertainment and recreation and personal services. Meanwhile, low prices have bogged down oil production.

The continued, concerning rise in new COVID-19 cases also made Canadian headlines this week. A sharp pick-up in caseloads prompted tightening measures in Quebec and brought pressure to do the same in Ontario. Bars, restaurants, cinemas, casinos, restaurant dining rooms and casinos were all ordered closed in Quebec until October 28th. Of cold comfort, these industries combined account for less than 5% of GDP, and the temporary nature of the closures imply that Quebec’s recovery should not be blown too far off course. Still, the shutdowns are another blow to industries that are already struggling.

Analysts were also given insight into the impact of COVID-19 on second quarter population growth this week. In all, only 25k people came to the country over the April-June period, marking the weakest such intake since at least 1946. The main drag was non-permanent residents (mostly foreign students and those on temporary work visas), which fell 140% y/y in the second quarter. Regionally, the slowdown was broad-based, with Saskatchewan, Manitoba, B.C., Ontario and Quebec taking the deepest hits relative to recent trends (Chart 2).

As bad as these data were, they matched our dour expectations. Interestingly, population growth held up relatively well across most of the Atlantic Provinces (except Newfoundland and Labrador), consistent with our forecast calling for these regions to outperform the country overall in 2020 – a forecast few would have had at the start of the year.

U.S: Upcoming Key Economic Releases

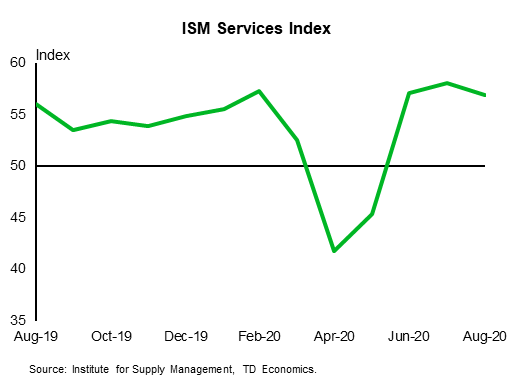

U.S. ISM Services Index – September

Release Date: October 5, 2020

Previous: 56.9

TD Forecast: 56.9

Consensus: 56.1

Business surveys have generally been signaling no let-up in the recovery, even as the hard data have been showing some deceleration. However, the hard data looked stronger than the survey data initially when the economy “reopened.” We expect another fairly healthy reading for ISM services index (TD: 56.9). The manufacturing ISM index fell in September, but with the level still solidly over 50 at 55.4 (down from 56.0).

Canada: Upcoming Key Economic Releases

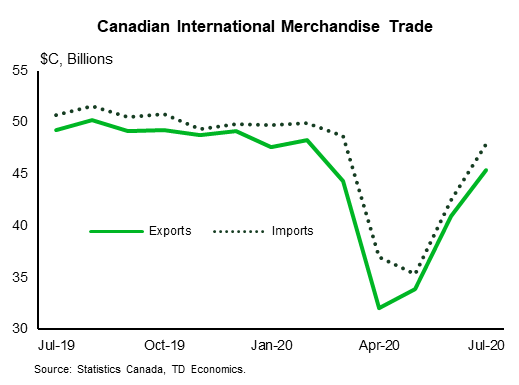

Canadian International Merchandise Trade – August

Release Date: October 6, 2020

Previous: -$2.45bn

TD Forecast: -$3.20bn

Consensus: NA

TD looks for the merchandise trade deficit to widen to $3.2bn in August, reflecting a modest increase in imports and little change to export activity. The latter will be weighed down by some giveback in motor vehicles, which account for 20% of total exports and had already returned to pre-covid levels by July, although employment/hours worked and manufacturing PMI data point to a stronger performance for other export categories. Exports are also supported by higher factory prices, suggesting a modest contraction for real exports in line with flash estimates for a pullback in manufacturing.

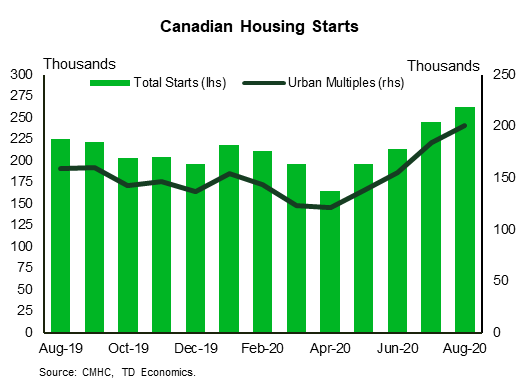

Canadian Housing Starts – September

Release Date: October 8, 2020

Previous: 262k

TD Forecast: 250k

Consensus: NA

We look for blistering pace of residential construction to continue into September with housing starts forecast remain strong at 250k annualized, down from 262k in August. This follows a solid increase in residential building permits for August and the highest reading for business sentiment in the construction industry since early 2018, along with recent strength in existing home sales. If realized, our forecast would leave the Q3 average sitting just above 250k which is the most for any quarter since 1990.

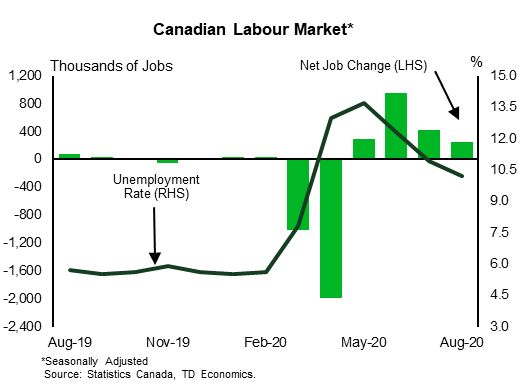

Canadian Employment – September

Release Date: October 9, 2020

Previous: 246k, unemployment rate: 10.2%

TD Forecast: 150k, unemployment rate: 9.6%

Consensus: NA

The labour market recovery is expected to continue into September with 150k jobs created during the month. This is a slowdown from previous months but would still have registered as one of the strongest prints of the pre-COVID era. High frequency mobility data has continued to show slowing momentum into the fall, with little change in the number of Canadians at workplaces and a plateau in transit/vehicle usage. However, other data points to further labour market gains, with hiring intentions and job postings showing improvement since the August LFS. Job growth of 150k should see the unemployment rate drift back to 9.6%, allowing for some modest improvement in labour force participation. Regional rollback of COVID restricts will have little to no impact on this report since most occurred after the reference week but could weigh on targeted sectors (bars and restaurants) in October.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals