Sterling softened again after the Brussels meeting ended with nothing more than comments that UK and EU are still far apart. Yet, traders are still holding their bets for now. Yen and Dollar also shrug off the deep pull back in US stocks overnight. Some fresh selling is seen in Asian session today. Commodity currencies are currently the stronger ones. Meanwhile, Euro is mixed as ECB policy recalibration is awaited.

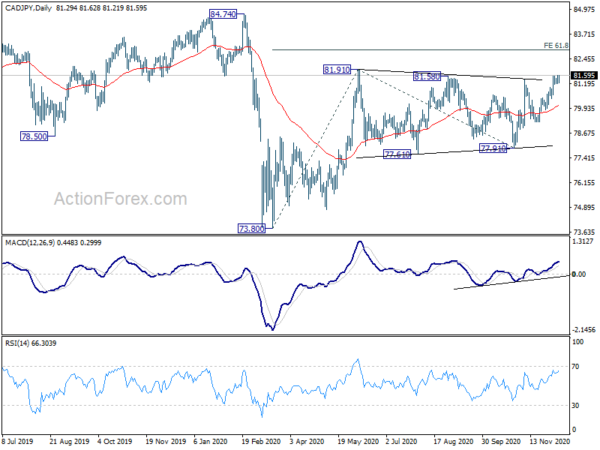

Technically, Canadian Dollar strengthened overnight after the relatively uneventful BoC rate decision. CAD/JPY is resuming the rise from 77.91 and it;s now pressing key resistance zone at 81.58/81.91. Decisive break there will resume whole rise from 73.80 to 61.8% projection of 73.80 to 81.91 from 77.91 at 82.92. Such development might come with USD/CAD’s break of 1.2768 temporary low too. In addition to Euro pairs, these two are worth a watch today.

In Asia, currently, Nikkei is up 0.01%. Hong Kong HSI is down -0.48%. China Shanghai SSE is up 0.24%. Singapore Strait Times is down -0.46%. Japan 10-year JGB yield is down -0.0010 at 0.020. Overnight, DOW dropped -0.35%. S&P 500 dropped -0.79%. NASDAQ dropped -1.94%. 10-year yield rose 0.028 to 0.941.

New deadline set for Brexit trade talks after Brussels meeting

The so called “Last Supper” meeting between UK Prime Minister Boris Johnson and European Commission President Ursula von der Leyen ended with no concrete progress. Both sides’ position remained “far apart” and a new deadline of this week is set for further talks.

After dinner, von der Leyen said, “we had a lively and interesting discussion on the state of play across the list of outstanding issues. We gained a clear understanding of each other’s positions. They remain far apart.” “We agreed that the teams should immediately reconvene to try to resolve these essential issues,” she added. “We will come to a decision by the end of the weekend.”

Separately, EU Financial Services Services Commissioner Mairead McGuinness said, “today we are preparing contingency plans, very specific and very narrowly focused to make sure that in the event of a ‘no deal’ that those sectors that are vulnerable, transport, aviation etc, that specific plans are put in place to maintain connectivity.”

NASDAQ lost 2% from new record, DOW lost momentum ahead of key near term projection

NASDAQ suffered a steep pull back and ended down -1.94% at 12338.95 overnight, after hitting new record high at 12607.14. Stalled stimulus talks in the US was a factor putting investors on guard. The Congress has less than tw0 weeks to try and reach a comprise before budget deadline. Additionally, the US had the worst days of coronavirus pandemic so far, with daily deaths hitting 3000 for the first time.

Technically, there is no immediate threat to the up trend of NASDAQ so far. As long as 12027.16 support holds, the record run is still in favor to continue. Next target is 38.2% projection of 6631.42 to 12074.06 from 10822.57 at 12901.65.

Meanwhile, DOW is already just inch away from equivalent target, 61.8% projection of 18213.65 to 29199.35 from 26143.77 at 30340.30. Upside momentum in DOW has been clearly diminishing as seen in daily MACD. We’d continue to view this projection level as a major near term test for DOW and a more noticeable pull back could be around the corner. Nevertheless, near term trend won’t be under much threat as long as 29231.20 support holds.

Gold in pull back after hitting 55 D EMA, another rise still in favor

Gold was in deep pull back overnight after failing to sustain above 55 day EMA. At this point, with 1821.96 minor support intact, further rise is still expected. Break of 1875.27 temporary top should reaffirm the case that corrective fall from 2075.18 has completed at 1764.31. Further rally should then be seen back to 1965.50 resistance next.

However, firm break of 1821.96 will indicate rejection by 55 day EMA (now at 1868.84). Such development will revive near term bearishness. Another decline attempt should then be seen for a test on 1764.31 low at least. In this case, we’d likely see the Dollar Index rebound further away from 90 handle.

EUR/CHF and EUR/JPY in contrasting outlook ahead of ECB recalibration

ECB monetary policy decision is a major focus for today and “recalibration” of the instruments are widely expected. Of the various tools, the pandemic emergency purchase program (PEPP) and the targeted longer-term refinancing operations (TLTROs) are the keys. For the former, we expect to see an increase of EUR 500B to the current envelope, making the total size to EUR 1850B . The program will extend to last at least until end-2021. Meanwhile, the discount window of TLTRO-III could be extended to the entire 3-year duration. Further easing in the collateral requirement is also likely.

Some suggested readings:

Technically, Euro is relatively mixed for the moment. EUR/CHF’s decline from 1.0871 was deeper then originally expected. It suggests that EUR/CHF is in another falling leg inside the corrective pattern from 1.0915. Deeper fall is in favor as long as 1.0799 minor resistance holds, for 1.0661 support.

On the other hand, EUR/JPY’s price actions from 126.68 are clearly corrective. It’s also holding well above 125.13 resistance turned support. Thus, another rise is in favor through 126.68 to 127.07 key resistance. Decisive break there will resume whole rally form 114.42. We’d see which way the Euro goes soon.

On the data front

Japan BSI large manufacturing index rose to 21.6 in Q4. PPI dropped -2.2% in November. Australia consumer inflation expectations was unchanged at 3.5% for December. UK RICS house price balance dropped slightly to 66 in November.

Looking ahead, UK GDP, productions and trade balance will be featured in European session. France will release industrial output. But major focus is on ECB. Later in the day, US will release jobless claims and CPI.

AUD/USD Daily Report

Daily Pivots: (S1) 0.7402; (P) 0.7444; (R1) 0.7482; More…

Intraday bias in AUD/USD stays on the upside at this point. Current rally 0.5506 should target 0.7635 key long term fibonacci level. On the downside, however, break of 0.7351 will indicate short term topping and turn bias back to the downside for pull back.

In the bigger picture, the sustained trading above 55 week EMA (now at 0.6978) is a sign of medium term bullishness. Nevertheless, AUD/USD will still need to overcome 38.2% retracement of 1.1079 (2011 high) to 0.5506 (2020 low) at 0.7635 decisively to indicate completion of long term down trend from 1.1079. Otherwise, current rebound from 0.5506 could still turn out to be a correction in the long term down trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Index Q/Q Q4 | 21.6 | 0.1 | ||

| 23:50 | JPY | PPI Y/Y Nov | -2.20% | -2.10% | -2.10% | |

| 0:00 | AUD | Consumer Inflation Expectations Dec | 3.50% | 3.50% | ||

| 0:01 | GBP | RICS Housing Price Balance Nov | 66% | 55% | 68% | 67% |

| 0:30 | AUD | RBA Bulletin | ||||

| 7:00 | GBP | GDP M/M Oct | 0.50% | 1.10% | ||

| 7:00 | GBP | Manufacturing Production M/M Oct | 1.00% | 0.20% | ||

| 7:00 | GBP | Manufacturing Production Y/Y Oct | -7.40% | -7.90% | ||

| 7:00 | GBP | Industrial Production M/M Oct | 0.30% | 0.50% | ||

| 7:00 | GBP | Index of Services 3M/3M Oct | 14.20% | |||

| 7:00 | GBP | Goods Trade Balance (GBP) Oct | -9.6B | -9.3B | ||

| 7:45 | EUR | France Industrial Output M/M Oct | 0.40% | 1.40% | ||

| 12:45 | EUR | ECB Interest Rate Decision | 0.00% | |||

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Initial Jobless Claims (Dec 4) | 723K | 712K | ||

| 13:30 | USD | CPI M/M Nov | 0.20% | 0.00% | ||

| 13:30 | USD | CPI Y/Y Nov | 1.30% | 1.20% | ||

| 13:30 | USD | CPI Core Y/Y Nov | 1.80% | 1.60% | ||

| 13:30 | USD | CPI Core M/M Nov | 0.10% | 0.00% | ||

| 15:00 | GBP | NIESR GDP Estimate Nov | 10.20% | |||

| 15:30 | USD | Natural Gas Storage | -1B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals