Dollar’s decline continues as another week starts as focus turns to Fed and BoJ, as well as a batch of important economic data. . European majors are also soft even though they managed to gain against the greenback. On the other hand, Australian and New Zealand Dollar are firmer together with Yen. Overall sentiments are mixed for the moment. But eyes will also be on India as coronavirus crisis intensified.

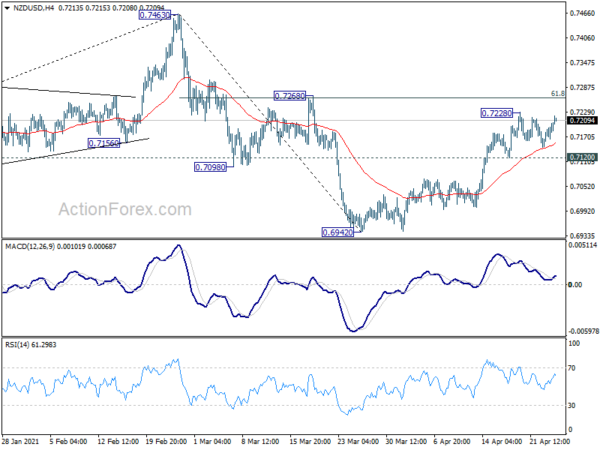

Technically, USD/CHF’s breach of 0.9127 temporary low suggests resumption of fall from 0.9471 towards 0.9029 fibonacci level. Focus will now turn to 0.7815 temporary top in AUD/USD and 0.7228 temporary top in NZD/USD. Break of these levels will further confirm broad based weakness in Dollar. As for NZD/USD, break of 0.7268 resistance should also confirm completion of the correction from 0.7463, and pave the way to retest this high.

In Asia, Nikkei is up 0.44%. Hong Kong HSI is down -0.25%. China Shanghai SSE is down -0.41%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is up 0.0068 at 0.076.

Gold rebound capped by 1800, but more upside still in favor

Gold’s rebound lost momentum after hitting 1797.71 last week, failing to break through 1800 handle. Some consolidations could be seen first. Mild near term bullishness is maintained with gold holding above 55 day EMA as well as 1763.36 minor support. We’d still expect another rise through 1797.71 to 38.2% retracement of 2075.18 to 1676.65 at 1828.88.

Also, firm break of 1828.88 will affirm the case that correction from 2075.18 has completed with three waves down to 1676.65. However, rejection by 1828.88, or break of 1763.36 support, would likely extend the decline from 2075.18 with another leg through 1676.65 low.

BoE Broadbent expects very rapid growth over next quarters

BoE Deputy Ben Broadbent said in a Telegraph interview published over the weekend that UK would see “very rapid growth at least over the next couple of quarters”. Though, it’s a too son to call it a “roaring twenties” scenario. He added, “the burden of proof it seems to me should be as to why that wouldn’t happen, rather than why it would, so I have tended to be on that more optimistic side.”

He also saw “less of a disinflationary effect”. “The price rises for those hitting capacity limits are going to be bigger than the falls in prices for those seeing falls in demand”, he explained. “When you get the shift in demand, you’re going to run into bottlenecks in some areas, particularly in those areas where supply, too, has been hit for a particular reason”.

BoJ and Fed to be non-events, GDP and inflation data watched

Two central banks will meet this week. BoJ will keep monetary policy unchanged and release new economic projections. No change in policy is expected. While BoJ might revised up growth forecasts, it will lower inflation forecasts at the same time. Fed is also widely expected to keep monetary policy unchanged. Chair Jerome Powell should reiterate that it’s premature to talk about stimulus. Fed officials will need to actual data, rather than outlook, before putting their hands on interest rates.

Suggested readings on Fed and BoJ:

While the BoJ and FOMC meeting would likely be non-events, economic data could be rather market moving. In particular, there will be GDP data from US, Eurozone and Canada; and inflation data from Australia, Eurozone and US. Here are some highlights for the week:

- Monday: Japan corporate services price index; German Ifo business climate: US durable goods orders.

- Tuesday: BoJ rate decision; UK CBI realized sales; US house price index, consumer confidence.

- Wednesday: Japan retail sales; Australia CPI; Germany Gfk consumer sentiment; Swiss Credit Suisse economic expectations; Canada retail sales; US goods trade balance, FOMC rate decision.

- Thursday: New Zealand trade balance; New Zealand ANZ business confidence; Australia import prices; Germany import prices, CPI flash, unemployment; Eurozone M3 money supply; US advance GDP, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, consumer confidence, housing starts; China PMIs; Australia PPI, private sector credit; France GDP flash; Swiss retail sales, KOF economic barometer; Germany GDP flash; Eurozone CPI flash, GDP flash; Canada GDP, IPPI and RMPI; US personal income and spending, Chicago PMI.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9117; (P) 0.9148; (R1) 0.9167; More….

USD/CHF’s fall from 0.9471 resumes by breaking 0.9127 temporary low. Intraday bias is back on the downside for 61.8% retracement of 0.8756 to 0.9471 at 0.9029 next. Sustained break there would bring retest of 0.8756 low. On the upside, though, break of 0.9194 resistance will indicate short term bottoming. Intraday bias will be turned back to the upside for rebound.

In the bigger picture, rejection by 61.8% retracement of 0.9901 to 0.8756 at 0.9464 argues that rebound from 0.8756 was probably just a corrective move. That is, larger down trend from 1.0237 might be still in progress. We’ll monitor the downside momentum of the decline from 0.9471, to assess the chance of breakthrough 0.8756 low at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Mar | 0.70% | -0.10% | 0.00% | |

| 8:00 | EUR | Germany IFO Business Climate Apr | 97.7 | 96.6 | ||

| 8:00 | EUR | Germany IFO Current Assessment Apr | 94.5 | 93 | ||

| 8:00 | EUR | Germany IFO Expectations Apr | 101.4 | 100.4 | ||

| 12:30 | USD | Durable Goods Orders Mar | 2.50% | -1.20% | ||

| 12:30 | USD | Durable Goods Orders ex-Transport Mar | 1.60% | -0.90% |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals