Major pairs and crosses are still bounded inside last week’s range as markets failed to take a decisive direction. While oil price continues to strengthen its rally, there is little reaction from Canadian Dollar so far. Stocks are also range bound while 10-year yield hover around 1.6 handle. Nevertheless, volatility might start to come back with US ADP employment and tomorrow’s non-farm payrolls.

Technically, we’d maintain that more downside is in favor in both Dollar and Yen for now, unless some levels are broken decisively. The levels include 1.4090 support in GBP/USD, 0.7673 support in AUD/USD, 0.9046 resistance in USD/CHF and 1.2201 resistance in USD/CAD. As for Yen pairs, the levels are 132.51 support in EUR/JPY, 153.81 support in GBP/JPY and 89.55 support in CAD/JPY.

In Asia, at the time of writing, Nikkei is up 0.49%. Hong Kong HSI is down -0.43%. China Shanghai SSE is up 0.39%. Singapore Strait Times is up 0.15%. Japan 10-year JGB yield is up 0.0039 at 0.083. Overnight, DOW rose 0.07%. S&P 500 rose 0.14%. NASDAQ rose 0.14%. 10-year yield dropped -0.024 to 1.591.

Fed Harker: It may be time to a least think about thinking about tapering

Philadelphia Fed President Patrick Harker said “we’re planning to keep the federal funds rate low for long.” He added, “but it may be time to at least think about thinking about tapering our $120 billion in monthly Treasury bond and mortgage-backed securities purchases.”

“We have to be careful in removing accommodation so that we don’t create any kind of ‘taper tantrum,’” he emphasized. “And that’s why we need to communicate very early, very often what we’re going to do.”

Fed: Economy expanded at somewhat faster pace, price pressures increased further

Fed’s Beige Book report noted that the national economy expanded at a “moderate pace”, “somewhat faster” than the prior reporting period. Several Districts cited the “positive effects” of increased vaccination and relaxed social distancing measures. Overall, “expectations changed little, with contacts optimistic that economic growth will remain solid.”

Two-third of Districts reported “modest employment growth” while wage growth was “moderate”. Businesses expected “labor demand will remain strong, but supply constrained, in the months ahead”. Overall price pressures “increased further”. Businesses anticipated facing “cost increase and charging higher prices in coming months.”

China Caixin PMI services dropped to 55.1, composite dropped to 53.8

China Caixin PMI Services dropped to 55.1 in May, down from 56.3, below expectation of 56.2. PMI Composite dropped to 53.8, down from 54.7.

Wang Zhe, Senior Economist at Caixin Insight Group said: “To sum up, the expansion in manufacturing and services maintained its momentum as both supply and demand expanded. Overseas demand was generally good, but service exports were affected by the pandemic. The job market continued to improve. In May, services recovered faster than manufacturing. Entrepreneurs were confident about the economic outlook. Inflation remained a crucial concern as the price gauges in manufacturing and services both rose last month.

Australia trade surplus rose to AUD 8B

Australia goods and services exports rose 3% mom to AUD 39.8B in April. Imports dropped -3% to AUD 31.7B. Trade surplus rose from AUD 2.2B to AUD 8.0B, matched expectations. Retail sales rose 1.1% mom, unchanged from preliminary results.

AiG Performance of Construction Index dropped -0.8 pts to 58.3, “largely maintaining the strong pace of post-2020 recovery following on from a record high in March“.

Looking ahead

Eurozone PMI services final and UK PMI services final are featured in European session. Later in the day, US will release ADP employment, jobless claims, non-farm productivity and ISM services.

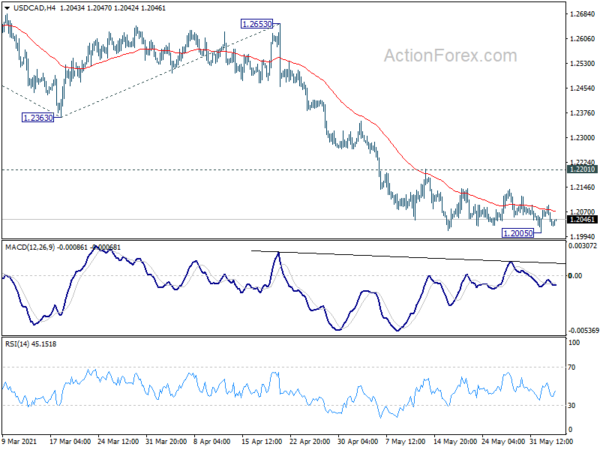

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2013; (P) 1.2052; (R1) 1.2075; More…

Intraday bias in USD/CAD remains neutral as sideway trading continues. Again, we’d stay cautious on strong support from 1.2048/61 to bring reversal. On the upside, break of 1.2201 resistance will indicate short term bottoming and turn bias to the upside for stronger rebound. On the downside, break of 1.2005, and sustained break of 1.2048/61 will carry larger bearish implications. Next near term target will be 161.8% projection of 1.2880 to 1.2363 from 1.2653 at 1.1816.

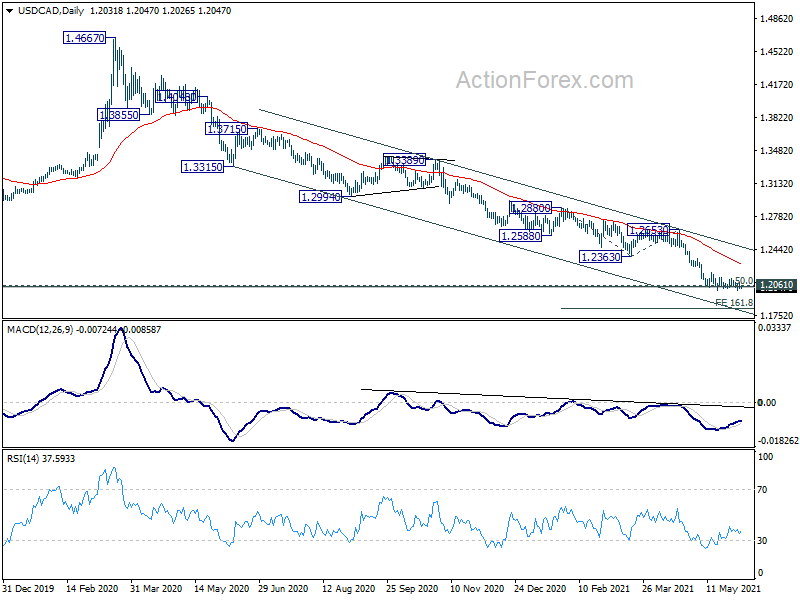

In the bigger picture, fall from 1.4667 is seen as the third leg of the corrective pattern from 1.4689 (2016 high). We’d look for strong support from 1.2061 (2017 low) and 50% retracement of 0.9406 to 1.4689 at 1.2048 to bring rebound. Nevertheless, sustained break of 1.2363 support turned resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will remain bearish in case of strong rebound. Also, sustained break of 1.2061 will pave the way to 61.8% retracement of 0.9406 to 1.4689 at 1.1424.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Construction May | 58.3 | 59.1 | ||

| 1:30 | AUD | Retail Sales M/M Apr | 1.10% | 1.10% | 1.10% | |

| 1:30 | AUD | Trade Balance (AUD) Apr | 8.03B | 8.00B | 5.57B | |

| 1:45 | CNY | Caixin Services PMI May | 55.1 | 56.2 | 56.3 | |

| 7:45 | EUR | Italy Services PMI May | 52 | 47.3 | ||

| 7:50 | EUR | France Services PMI May F | 56.6 | 56.6 | ||

| 7:55 | EUR | Germany Services PMI May F | 52.8 | 52.8 | ||

| 8:00 | EUR | Eurozone Services PMI May F | 55.1 | 55.1 | ||

| 8:30 | GBP | Services PMI May F | 61.8 | 61.8 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y May | -96.60% | |||

| 12:15 | USD | ADP Employment Change May | 695K | 742K | ||

| 12:30 | USD | Initial Jobless Claims (May 28) | 410K | 406K | ||

| 12:30 | USD | Nonfarm Productivity Q1 | 5.50% | 5.40% | ||

| 12:30 | USD | Unit Labor Costs Q1 | -0.40% | -0.30% | ||

| 13:45 | USD | Services PMI May F | 70.1 | 70.1 | ||

| 14:00 | USD | ISM Services PMI May | 62.9 | 62.7 | ||

| 14:00 | USD | ISM Services Employment May | 58.8 | |||

| 14:30 | USD | Natural Gas Storage | 115B | |||

| 15:00 | USD | Crude Oil Inventories | -1.7M |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals