Overall markets are in risk-off mode today, started with steep selloff in Hong Kong and China stocks. Nevertheless, losses in Europe are limited, while DOW future is just slightly lower. In the currency markets, commodity currencies are the worst performing ones, as led by New Zealand Dollar. Yen is the strongest one, followed by Swiss Franc. Dollar, Euro and Sterling are mixed.

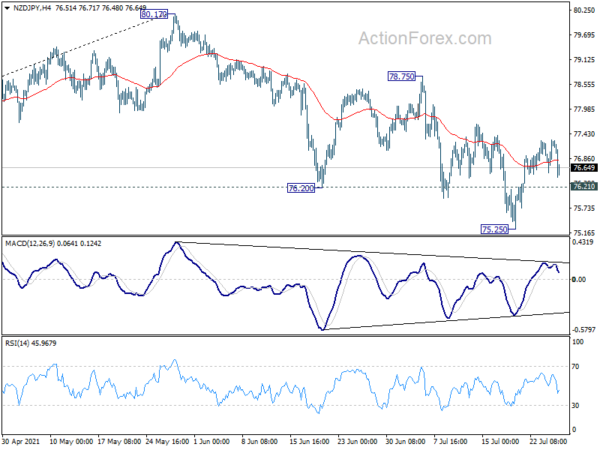

Technically, USD/JPY’s break of 110.00 minor support argues that recovery from 109.05 has completed at 110.58. Focus will firstly turn to 151.37 minor support in GBP/JPY, break will also suggest completion of recovery from 148.43. Also, break of 76.21 minor support in NZD/JPY will indicate completion of the recovery from 75.25.

In Europe, at the time of writing, FTSE is down -0.53%. DAX is down -0.59%. CAC is down -0.52%. Germany 10-year yield is down -0.0169 at -0.431. Earlier in Asia, Nikkei rose 0.49%. Hong Kong HSI dropped -4.22%. China Shanghai SSE dropped -2.49%. Singapore Strait Times dropped -0.01%. Japan 10-year JGB yield rose 0.0027 to 0.020.

US durable good orders rose 0.8% in June, ex-transport orders rose 0.3%

US durable goods orders rose 0.8% to USD 257.6B in June, below expectation of 2.1%. That’s the thirteen growth in last fourteen months. Ex-transport orders rose 0.3%, below expectation of 0.8%. Ex-defense orders rose 1.0%. Transportation equipment rose 2.1% to USD 77.5B.

ECB Holzmann: New forward guidance a step too far

ECB’s Governing Council member Robert Holzmann told CNBC that the central bank’s forward guidance went “a step too far”. The statement released last week noted that interest rates will remain at their present or until it sees inflation in line with the target of 2% “well ahead” of the end of its forecast horizon.

“We would have wished a different guidance, which doesn’t bind us too long in the future, in order to stay agile, and ready in case inflation requires an earlier liftoff,” he said.

“Our mandate breaks any forward guidance, but I think it would have been more honest to the markets to tell ‘Yes, we want to stay accommodative as it is for the time being, but we stand ready to change the rate if it’s necessary’,” Holzmann added.

UK CBI retail sales dropped 23, but orders grew fastest since 2010

CBI said UK retail sales dropped from 25 to 23 in the year July, but continued to grow at a rate “well above the long-run average”. Orders grew at the fastest pace since December 2010 (up fro 30 to 49). Sales are expected to grow at a faster pace (+29%) and orders at a slower pace (+39%) next month.

Ben Jones, Principal Economist at the CBI, said: “Helping people and businesses live safely with the virus is key to maintaining the confidence needed for economic recovery. Businesses will continue to face significant disruption without a more effective system for allowing double-jabbed people who are not infectious to continue to work—both in the coming weeks but, crucially, as we head into the autumn and winter months.”

BoJ Kuroda to adopt a learning-by-doing approach on climate change

BoJ Governor Haruhiko Kuroda said in a speech, “waiting until specific guidelines and ideas are fixed will only delay our response to the urgent global issue of climate change”.

Instead, “it will be important to adopt a learning-by-doing approach: implement the crucial measures first, then make adjustments when necessary.”

“The Bank will follow appropriately the evolving nature of climate-related issues, exchange dialogue with domestic and foreign stakeholders, including through active participation in international discussions,” he said, “and will constantly review its measures and make adjustments where needed.

Hong Kong HSI down -4.2% as tech rout continues

The selloff in Hong Kong intensified today with HSI losing a massive -1105 pts or -4.22%. The crush on tech continued with Chinese stocks like Meituan and Alibaba down -12.7% and -5.5% respectively. The Shanghai SSE also dropped -2.49%.

The HSI is now standing at an important support level around 25000 handle a 61.8% retracement of 21139.26 to 31183.35 at 24976.10. Some support might be seen here on oversold condition. But prospect of a strong rebound is limited. The development this week suggests that whole rise from 21139.26 has completed with three waves up to 31183.35 as a corrective move. Fall from there is at best a leg inside a medium term side way pattern, and at worst a the third of the long term pattern from 33484.07. In the latter case, HSI could target 21139.26 and below. We’ll see how it goes.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.23; (P) 110.41; (R1) 110.73; More…

Break of 110.00 minor support suggests that USD/JPY’s recovery from 109.05 has completed at 110.58. Intraday bias is back on the downside for 109.05 support first. Break there will resume the fall from 111.65 to 38.2% retracement of 102.58 to 111.65 at 108.18. On the upside, above 110.58 will turn bias back to the upside for retesting 111.65 resistance.

In the bigger picture, medium term outlook is staying neutral with 111.71 resistance intact. The pattern from 101.18 could still extend with another falling leg. Sustained trading below 55 day EMA will bring deeper fall to 107.47 support and below. For now, outlook won’t turn bullish as long as 111.71 resistance holds, even in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Jun | 1.40% | 1.30% | 1.50% | |

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Jun | 8.30% | 8.20% | 8.40% | 8.50% |

| 12:30 | USD | Durable Goods Orders Jun | 0.80% | 2.10% | 2.30% | 3.20% |

| 12:30 | USD | Durable Goods Orders ex Transportation Jun | 0.30% | 0.80% | 0.30% | 0.50% |

| 13:00 | USD | S&P/Case-Shiller Home Price Indices Y/Y May | 17.00% | 15.40% | 14.90% | 15.00% |

| 13:00 | USD | Housing Price Index M/M May | 1.70% | 1.80% | 1.80% | |

| 14:00 | USD | Consumer Confidence Jul | 125.3 | 127.3 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals