Markets are generally in consolidative mode today. Dollar turns weaker against Swiss Franc and Yen despite better than expected jobless claims data. But the greenback is just range bound against other major currencies. Commodity currencies are digesting near term gains but losses are so far very limited. Euro is trading sideway against Sterling but weakens notably against Swiss Franc.

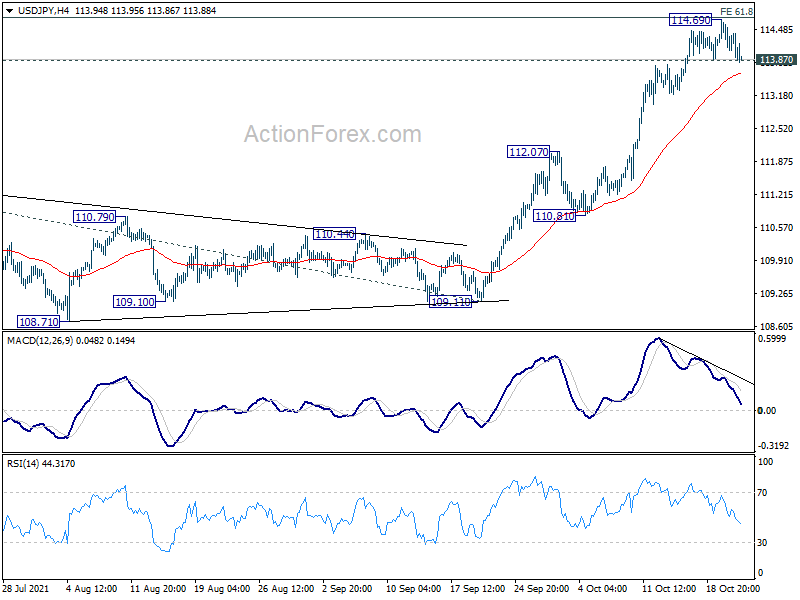

Technically, firstly, we’d continue to monitor if USD/JPY would break through 113.87 minor support firmly to start a near term pull back. That could be followed by break of 132.13 minor support in EUR/JPY and 156.58 minor support in GBP/JPY to confirm Yen’s general rebound. Secondly, we’d also see if EUR/CHF is breaking through 1.0678 temporary low to resume recent fall, and, whether EUR/GBP would follow through 0.8420 temporary low too.

In Europe, at the time of writing, FTSE is down -0.39%. DAX is up 0.06%. CAC is down -0.27%. Germany 10-year yield is up 0.017 at 0.107. Earlier in Asia, Nikkei dropped -1.87%. Hong Kong HSI dropped -0.45%. China Shanghai SSE rose 0.22%. Singapore Strait Times dropped -0.30%. Japan 10-year JGB yield dropped -0.0053 to 0.090.

US initial jobless claims dropped to 290k, continued to trend down

US initial jobless claims dropped -6k to 290k in the week ending October 16, better than expectation of 298k. It’s also the lowest level since March 14, 2020. Four-week moving average of initial claims dropped -15k to 320k, lowest since March 14, 2020 too.

Continuing claims dropped -122k to 2481k in the week ending October 9, lowest since march 14, 2020. Four-week moving average of continuing claims dropped -85k to 2656k, lowest since March 21, 2020.

US Philly Fed manufacturing dropped to 23.8, price indicators remained elevated

In the October Philadelphia Fed Manufacturing Business Outlook Survey, the diffusion index for current general activity dropped to 23.8, down from 30.7, below expectation of 26.0.

Looking at some details, current shipments index was essentially unchanged at 30.0. New orders rose 15 pts to 30.8. Employment index rose from 26.3 to 30.7. The index for prices paid rose 3 pts to 70.3. Current prices received index dropped -2 to 51.1. Price indicators remained elevated.

Australia NAB business confidence dropped to -1 in Q3

Australia NAB business confidence dropped from Q2’s 18 to -1 in Q3. Current business conditions dropped from 30 to 13. Conditions for the next 3 months dropped from 35 to 8. Conditions for the next 12 months also dropped from 33 to 19. Capex plans for the next 12 months dropped from 37 to 26. Trading conditions dropped from 36 to 16. Profitability dropped from 30 to 11. Employment dropped from 23 to 11.

Alan Oster, NAB Group Chief Economist, “With lockdowns in place for most of Q3, it’s unsurprising to see both business conditions and confidence take a fairly large hit for the quarter… While conditions deteriorated sharply, they didn’t fall to the depths seen during the first lockdowns in 2020.”

“While these survey results confirm the large hit to activity that took place in Q3, we are optimistic for a strong rebound in activity in Q4 and into 2022 and reopening progresses.”

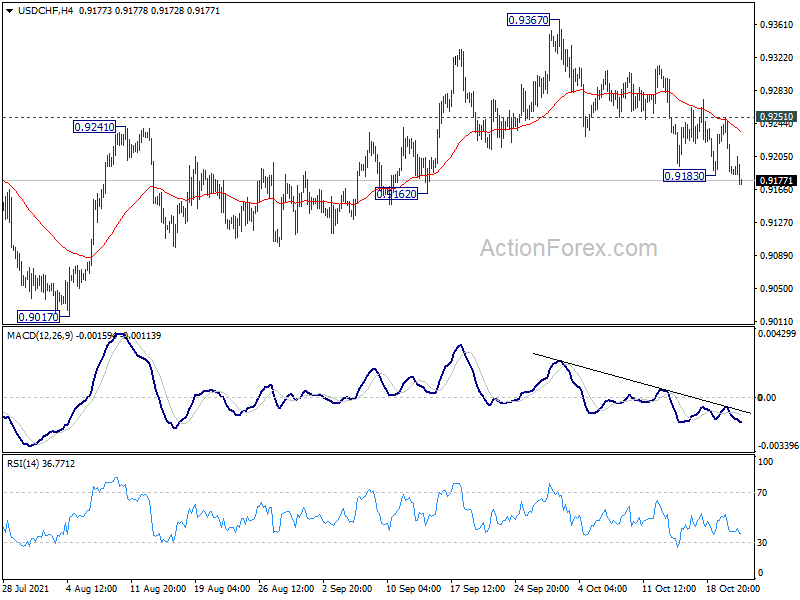

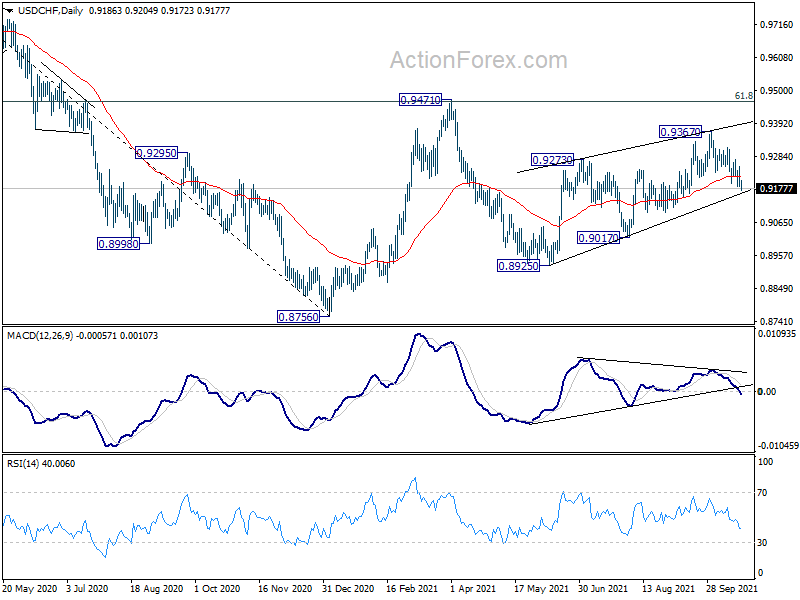

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9167; (P) 0.9209; (R1) 0.9232; More….

USD/CHF’s fall from 0.9367 resumes by breaking 0.9183 temporary low. Intraday bias is back on the downside for 0.9162 support. Considering bearish divergence condition in daily MACD, firm break of 0.9162 support will argue that whole rise from 0.8925 has completed Deeper decline would be seen to 0.9017 support next. On the upside, break of 0.9251 minor resistance will turn bias back to the upside for retesting 0.9367 instead.

In the bigger picture, the corrective structure of the rebound from 0.8925 argues that fall from 0.9471 is not completed yet. It could either be the second leg of pattern from 0.8756 (2021 low), or resuming larger down trend from 1.0237 (2018 high). We’d pay attention to the downside momentum of assess the odds later. But for now, medium term outlook will be neutral at best as long as 0.9471 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | NAB Business Confidence Q3 | -1 | 17 | 18 | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Sep | 21.0B | 23.5B | 19.8B | 16.1B |

| 12:30 | CAD | New Housing Price Index M/M Sep | 0.40% | 0.60% | 0.70% | |

| 12:30 | USD | Initial Jobless Claims (Oct 15) | 290K | 298K | 293K | 296K |

| 12:30 | USD | Philadelphia Fed Manufacturing Oct | 23.8 | 26 | 30.7 | |

| 14:00 | USD | Existing Home Sales Sep | 6.00M | 5.88M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Oct P | -5 | -4 | ||

| 14:30 | USD | Natural Gas Storage | -61.0B | 81B |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals