Australian Dollar leads other commodity currencies higher today, as supported by solid risk appetite. US futures indicate a much higher open and extended rally could push major indices to new record highs later this week. Dollar and Euro are currently the weakest ones for the day, followed by Yen. Sterling and Swiss Franc are mixed. In other markets, gold is trying to extend near term rally but upside momentum is weak. WTI crude oil is still defending 80 handle.

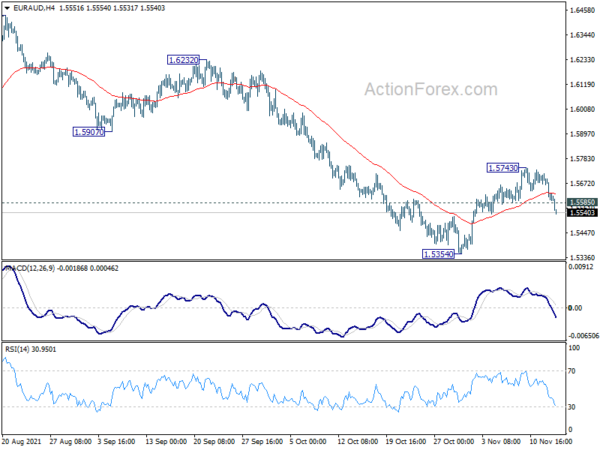

Technically, EUR/AUD’s break of 1.5585 minor support suggests that rebound from 1.5354 is complete at 1.5743. Deeper fall would be seen back to 1.5354 low. When that happens, we’ll see if it’s accompanied by break of 0.7431 minor resistance in AUD/USD, or deeper down trend extension in EUR/USD. The latter case is favored.

In Europe, at the time of writing, FTSE is down -0.04%. DAX is up 0.31%. CAC is up 0.31%. Germany 10-year yield is up 0.0070 at -0.250. Earlier in Asia, Nikkei rose 0.56%. Hong Kong HSI rose 0.25%. China Shanghai SSE dropped -0.16%. Singapore Strait Times rose 0.38%. Japan 10-year JGB yield dropped -0.0078 to 0.068.

US Empire State manufacturing rose to 30.9, employees and price paid surged

US Empire State Manufacturing Survey general business conditions jumped to 30.9 in November, up from 19.8, above expectation of 20.2. 43% of respondents reported improved conditions while 12% reported worsened conditions.

New orders rose 5 pts to 28.8. Shipment jumped 19 pts to 28.2. Delivery times dropped -5.8 to 38.0. Number of employees jumped 9 pts to 26.0, a record high. Average workweek also jumped 8 pts to 23.1. Price paid rose 4 pts to 83.0. Price paid rose 7 pts to 50.8, a record high.

From Canada, manufacturing sales dropped -3.0% mom in September, matched expectations. Wholesale sales rose 1.0% mom, below expectation of 1.1% mom.

ECB Lagarde: Conditions for rate hike very unlikely to be satisfied next year

In a European Parliament committee hearing, ECB President Christine Lagarde said, “growth momentum is moderating to some extent owing to supply bottlenecks and the rise in energy prices.” Consumer spending is “solid”, but shortages of materials, equipment and labour are “weighing on manufacturing production, weakening the near-term outlook.” “Although the duration of supply constraints is uncertain, they are likely to persist for several months and gradually ease only during 2022,” she added.

Lagarde also reiterated that the upswing in inflation is driven by three primary forces, energy prices, demand outpacing constrained supply, and reversal effect of German VAT cut. “The latter factor will fall out of the inflation calculation from January 2022 but the other two may last longer.” “As a result, we still see inflation moderating in the next year, but it will take longer to decline than originally expected,” she said.

On monetary policy, she said the conditions for rate hike are “very unlikely to be satisfied next year”. Intentions on further calibration of bond purchases will be announced in December. But “even after the expected end of the pandemic emergency, it will still be important that monetary policy – including the appropriate calibration of asset purchases – supports the recovery throughout the euro area and the sustainable return of inflation to our target of two per cent.”

Eurozone exports rose 10.0% yoy in Sep, imports rose 21.6% yoy

Eurozone exports of goods to the rest of the world rose 10.0% yoy to EUR 209.3B in September. Imports rose 21.6% yoy to EUR 202.0B. As a result, Eurozone recorded a EUR 7.3B surplus. Intra-Eurozone trade rose 16.4% yoy to EUR 191.5B.

In seasonally adjusted term, Eurozone exports dropped -0.4% mom to EUR 201.4B. Imports rose 1.5% mom to EUR 195.3%. Trade surplus narrowed to EUR 6.1B. Intra-Eurozone trade rose EUR 0.8B to EUR 182.9B.

Japan GDP contracted -0.8% qoq, -3.0% annualized in Q3

Japan GDP contracted -0.8% qoq in Q3, much worse than expectation of -0.2% qoq. In annualized term, GDP dropped -3.0% qoq, much worse than expectation of -0.8%.

Capital expenditure dropped -0.8% qoq, versus expectation of -0.6% qoq. External demand rose 0.1% qoq, versus expectation of 0.0% qoq. Private consumption dropped -1.1% qoq, versus expectation of -0.5% qoq. GDP price index dropped -1.1%, slightly better than expectation of -1.2%.

Economy minister Daishiro Yamagiwa said pace of pickup in the economy is weakening and policy support is needed. He also warned of downside risks from the global supply constraints. Prime Minister Fumio Kishida is expected to reveal a stimulus package “worth several tens of trillion yen” later this week on November 19.

BoJ Kuroda: Recovery mechanism maintained, inflation to hit 1% mid 2022

In a speech with business leaders, BoJ Governor Haruhiko Kuroda said that CPI is likely to “increase moderately in positive territory for the time being”, reflecting rise in energy prices. Thereafter, “it is projected to increase gradually to about 1 percent as the output gap turns positive around the middle of next year.”

He noted that economic recovery in Japan has been “somewhat slower than initially expected”. Nevertheless “the mechanism for economic recovery has been maintained.”

Real GDP is expected to recovery to pre-pandemic level in the first half of 2022. Thereafter, “as the resumption of economic activity progresses while public health is being protected, Japan’s economy is expected to follow a growth path that outpaces its potential growth rate, supported by relatively high growth in overseas economies and accommodative financial conditions.”

China industrial production rose 3.5% yoy in Oct, retail sales up 4.9% yoy

China industrial production rose 3.5% yoy in October, above expectation of 3.0% yoy. Retail sales rose 4.9% yoy, versus expectation of 3.8% yoy. Fixed asset investment rose 6.1% ytd yoy, versus expectation of 6.2%.

“The national economy was generally stable and maintained the trend of recovery,” the NBS said in a statement. “However, we must be aware that the international environment is still complicated and severe with many unstable and uncertain factors.”

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3370; (P) 1.3398; (R1) 1.3442; More…

GBP/USD is staying in consolidation from 1.3351 temporary low and intraday bias remains neutral first. We’d continue to expect upside of recovery to be limited below 1.3606 resistance, to bring down trend resumption. On the downside, break of 1.3351 will extend the decline from 1.4248 to 1.3164 fibonacci level next.

In the bigger picture, the structure of the fall from 1.4248 suggests that it’s a correction to the up trend from 1.1409 (2020 low) only. While deeper fall cannot be ruled out yet, downside should be contained by 38.2% retracement of 1.1409 to 1.4248 at 1.3164, at least on first attempt, to bring rebound. On the upside, firm break of 1.4376 key resistance (2018 high) will add to the case of long term bullish reversal. However, sustained trading below 1.3164 will revive some medium term bearishness and target 61.8% retracement at 1.2493.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q3 P | -0.80% | -0.20% | 0.50% | |

| 23:50 | JPY | GDP Price Index Q3 P | -1.10% | -1.20% | -1.10% | |

| 00:01 | GBP | Rightmove House Price Index M/M Nov | -0.60% | 1.80% | ||

| 02:00 | CNY | Retail Sales Y/Y Oct | 4.90% | 3.80% | 4.40% | |

| 02:00 | CNY | Industrial Production Y/Y Oct | 3.50% | 3.00% | 3.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Oct | 6.10% | 6.20% | 7.30% | |

| 04:30 | JPY | Industrial Production M/M Sep F | -5.40% | -5.40% | -5.40% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Sep | 6.1B | 12.5B | 11.1B | |

| 13:30 | CAD | Manufacturing Sales M/M Sep | -3.00% | -3.00% | 0.50% | |

| 13:30 | CAD | Wholesale Sales M/M Sep | 1.00% | 1.10% | 0.30% | |

| 13:30 | USD | Empire State Manufacturing Index Nov | 30.9 | 20.2 | 19.8 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals