Kiwi GDP contracted by 3.7% over the September quarter (due to lockdown), less than the -4.5% expected, despite Auckland spending the entire month of October in lockdown.

The smaller contraction shows that businesses and households have learned to adapt to Covid restrictions and that Covid related disruptions have less impact on economic activity.

The positive growth surprise alongside hot inflation and a tight labour market reasons the RBNZ will waste little time lifting interest rates early in 2022, adding the two consecutive highs in the back end of 2021.

Turning now to the Australian Labour force data for November. Employment rose by 366k in November following the easing of restrictions in mid-October, far stronger than the 200k gain expected.

The unemployment rate fell to 4.6% from 5.2%, despite a recovery in the participation rate to 66.1% from 64.7% last month. The labour market underutilization rate fell 2.6% to 12.1%, below its pre-pandemic level.

Following the more robust AU Q3 GDP data at the start of this month, today’s jobs report vindicates the RBA’s less dovish stance at its December Board meeting and supports market pricing for a start to interest rate hikes in 2022.

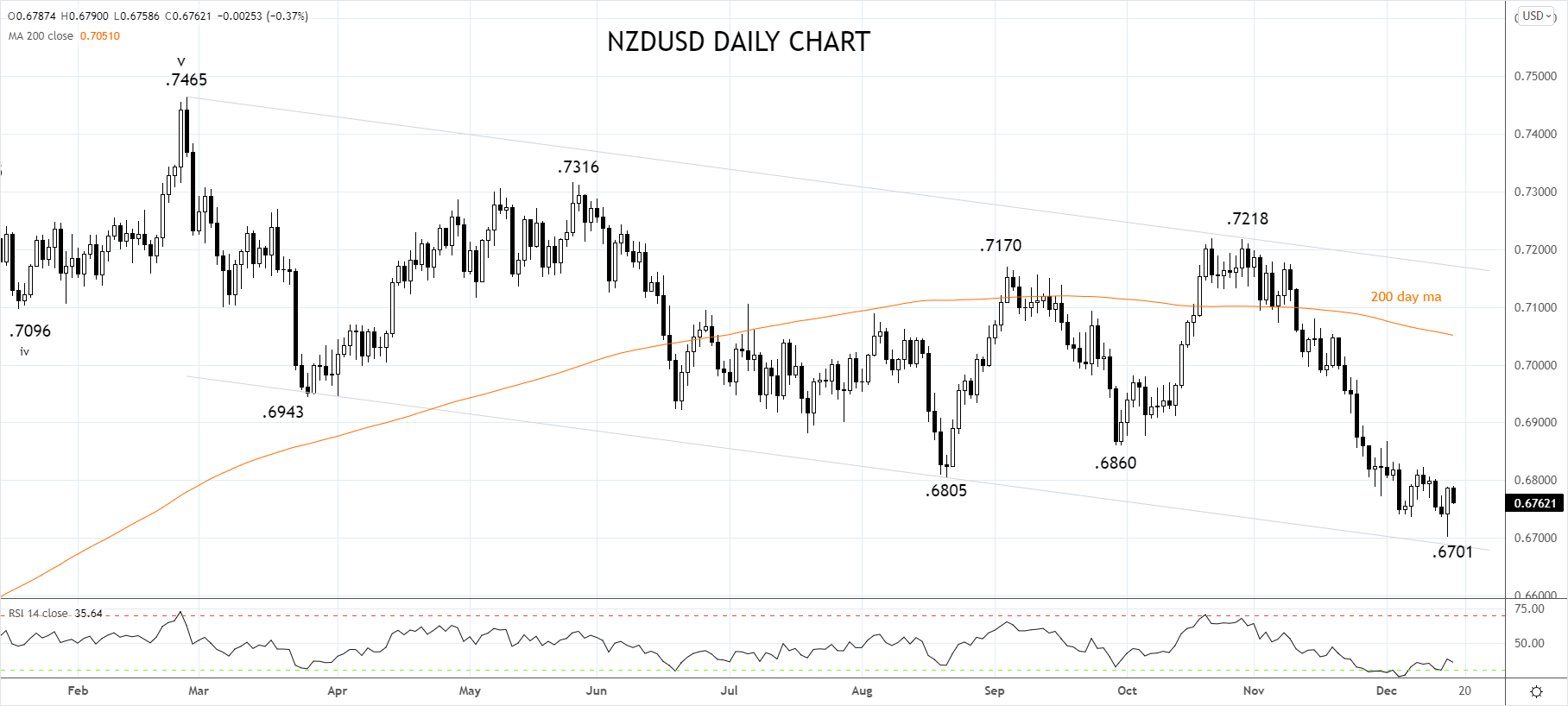

Tech-wise, the NZDUSD has rebounded nicely over the past 24 hours from the bottom of the nine-month trend channel, noted here yesterday. Providing trend channel support holds, look for the NZDUSD to extend its recovery towards short-term resistance at .6810/20 with scope to .6880/00.

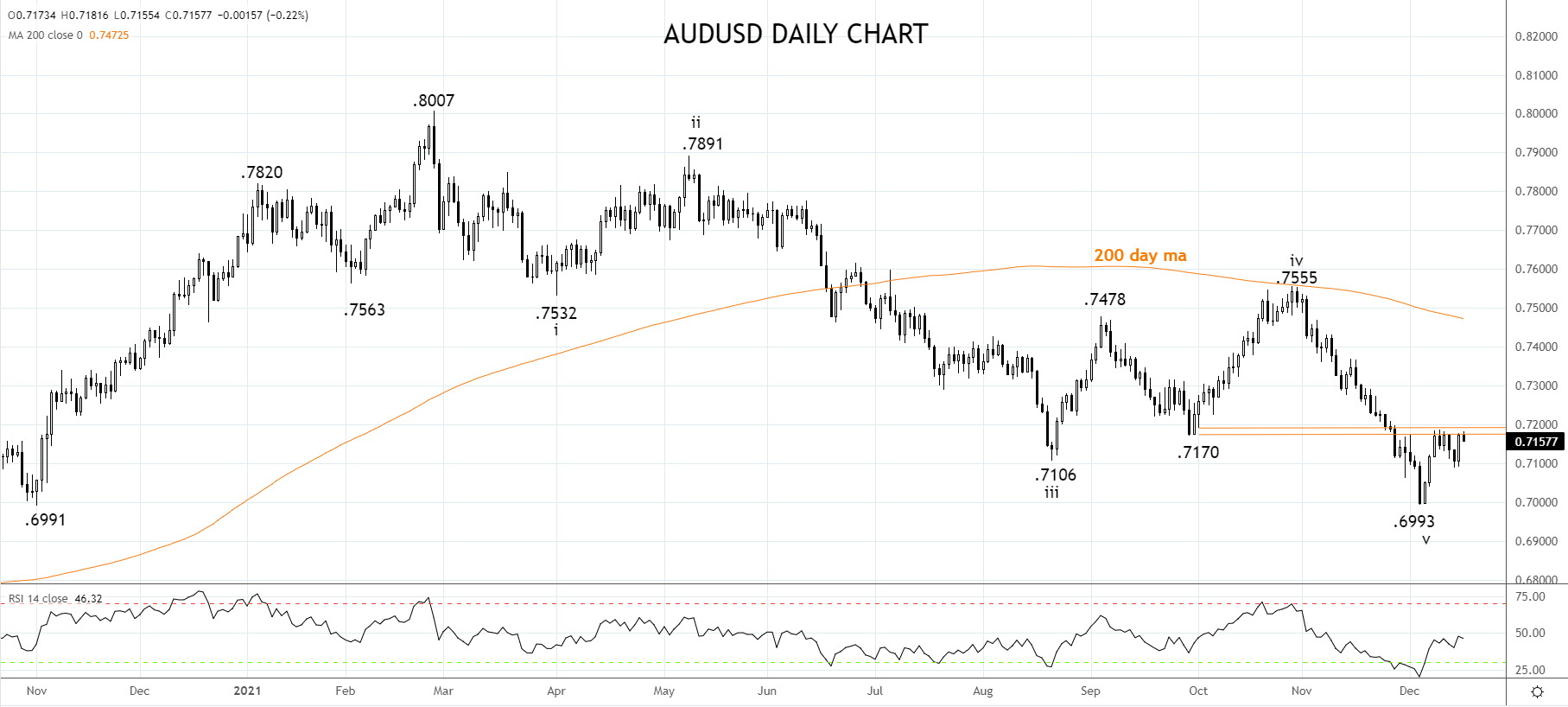

For the AUDUSD, further upside is dependent on a break above the short-term resistance .7185/95. A move that appears less certain following a worrying surge in new covid cases in NSW and Victoria over the past 48 hours, which casts some doubt over the re-opening. For this reason, the preference is to own the NZDUSD ahead of the AUDUSD.

For the AUDUSD, further upside is dependent on a break above the short-term resistance .7185/95. A move that appears less certain following a worrying surge in new covid cases in NSW and Victoria over the past 48 hours, which casts some doubt over the re-opening. For this reason, the preference is to own the NZDUSD ahead of the AUDUSD.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals