The financial markets are generally quiet today. Major European indexes are mixed while US futures are treading water. Gold is still trying to defend 1800 handle, despite dipping earlier. Silver is also recovering ahead of 20 handle. Bitcoin and Ethereum are also staying in sideway trading. Euro is firmer in general with Dollar and Yen. Swiss Franc is trading lower, followed by Aussie and Canadian.

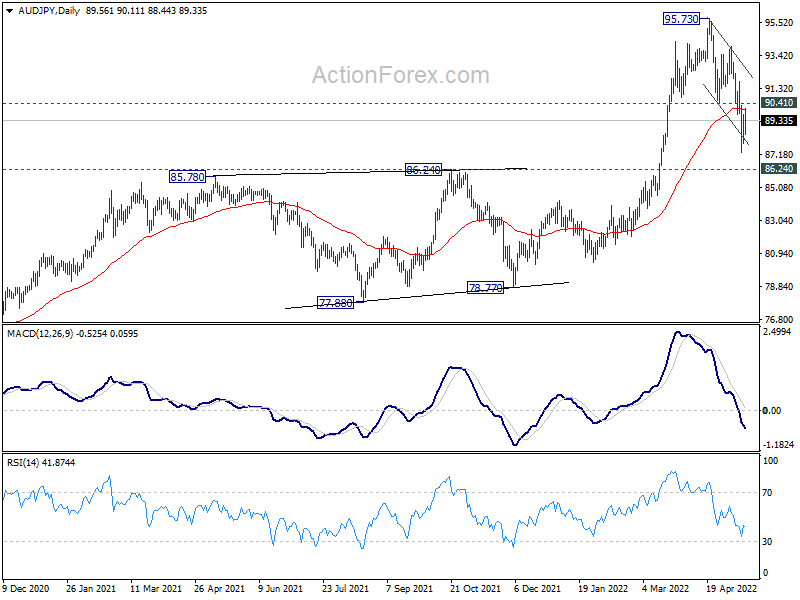

Technically, one focus in the week is whether overall risk sentiment would stabilize and rebound further. AUD/JPY could provide a guide to the development While it recovered ahead of 86.24 key medium term support, upside is capped by 55 day EMA (now at 89.99), around 90 handle. Sustained break of 90 handle will be a sign that overall risk sentiment is turning positive again.

In Europe, at the time of writing, FTSE is up 0.27%. DAX is down -0.65%. CAC is down -0.26%. Germany 10-year yield is up 0.0048 at 0.999. Earlier in Asia, Nikkei rose 0.45%. Hong Kong HSI rose 0.26%. China Shanghai SSE dropped -0.34%. Singapore Strait Times is up 0.82%. Japan 10-year JGB yield dropped -0.0014 at 0.244.

EU downgrades EZ 2022 GDP forecast to 2.7%, inflation upgraded to 6.1%

In the Spring 2022 Economic Forecast, EU revised 2022 GDP growth forecast for Eurozone sharply lower, and inflation forecast sharply higher. Here are the new forecasts for Eurozone:

- 2022 GDP growth at 2.7% (down from Autumn forecast of 4.3%.)

- 2023 GDP growth at 2.3% (down from 2.4).

- 2022 HICP inflation at 6.1% (up from 2.2%).

- 2023 HICP inflation at 2.7% (up from 1.4%).

- 2022 HICP core inflation at 3.5% (up from 2.0%).

- 2023 HICP core inflation at 2.4% (up from 1.7%).

Valdis Dombrovskis, Executive Vice-President said: “There is no doubt that the EU economy is going through a challenging period due to Russia’s war against Ukraine… The overwhelming negative factor is the surge in energy prices, driving inflation to record highs… While growth will continue this year and next, it will be much more subdued than previously expected. Uncertainty and risks to the outlook will remain high as long as Russia’s aggression continues.”

Eurozone exports rose 14.0% yoy in Mar, imports rose 35.4% yoy

Eurozone exports of goods rose 14.0% yoy to EUR 250.1B in March. Imports rose 35.4% yoy to EUR 266.5B. Trade deficit came in at EUR 16.4B. Intra-Eurozone trade rose 21.2% yoy to EUR 236.8B.

In seasonally adjusted terms, Eurozone exports rose 0.9% mom to EUR 225.3B. Imports rose 3.5% mom to EUR 242.8B. Trade deficit widened from EUR -11.3B to EUR -17.6B, versus expectation of EUR 2.3B surplus. Intra-Eurozone trade rose from February’s EUR 207.2B to EUR 210.3B.

ECB Villeroy: A too weak Euro goes against price stability objective

ECB Governing Council member Francois Villeroy de Galhau said in a Bank of France conference, “let me stress this: we will carefully monitor developments in the effective exchange rate, as a significant driver of imported inflation”. He added, “a euro that is too weak would go against our price stability objective.”

Villeroy said a “decisive” governing council meeting would be expected in June, followed by an “active summer” on policy. “The pace of the further steps will take into account actual activity and inflation data with some optionality and gradualism,” he said. Policymakers should “at least move towards the neutral rate”, he added.

BoJ Kuroda: Excess exchange rate volatility recently is undesirable

BoJ Governor Haruhiko Kuroda told the parliament today that “excess (exchange rate) volatility in a short term as seen recently is undesirable.” He pledged to keep a close watch of the impact of the currency moves on the economy and prices. He also added that exchange rate moves should be stable and reflecting economic fundamentals.

On monetary policy, “it’s important to back the economic activity with powerful monetary easing,” Kuroda reiterated. “It will take time for sustainable, stable inflation to take hold in Japan.”

China retail sales down -11.1% yoy in Apr, industrial production down -2.9% yoy

China retail sales dropped -11.1% yoy in April, worse than expectation of -6.0% yoy. Industrial production dropped -2.9% yoy, versus expectation of 0.7% yoy. Fixed asset investment rose 6.8% ytd yoy, also below expectation of 7.0%.

The “increasingly grim and complex international environment and greater shock of [the] Covid-19 pandemic at home obviously exceeded expectation, new downward pressure on the economy continued to grow.” The NBS said in a statement. But it added, “with progress in Covid controls and policies to stabilize the economy taking effect, the economy is likely to recover gradually.”

New Zealand BNZ services dropped to 51.4, disappointing in context of easing restrictions

New Zealand BNZ Performance of Services Index ticked down from 51.5 to 51.4 in April. Looking at some details, activity/sales dropped from 53.5 to 52.7. Employment rose from 49.2 to 51.2. New orders/business dropped from 59.0 to 53.6. Stocks/inventories rose from 52.8 to 54.8. Supplier deliveries dropped from 40.5 to 40.1.

BNZ Senior Economist Doug Steel said that “for large parts of the service sector that have been through the ringer over recent times, we suspect any result above breakeven would be welcomed. But, on the other hand, April’s result also looks somewhat disappointing in the context of easing COVID restrictions (from Red to Orange) halfway through the month.”

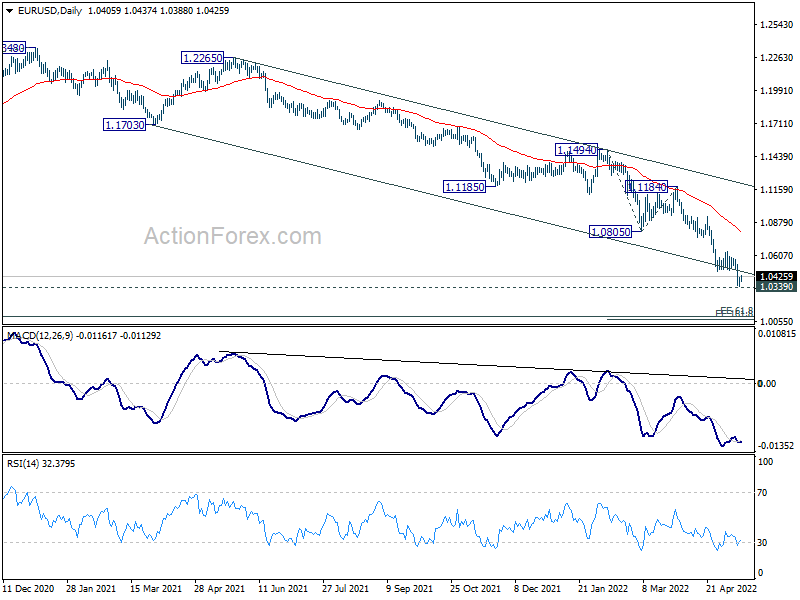

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0365; (P) 1.0393 (R1) 1.0435; More…

EUR/USD is staying in consolidation above 1.0339 long term support. Intraday bias remains neutral for the moment. Outlook also stays bearish as long as 1.0641 resistance holds. Decisive break of 1.0339 will carry larger bearish implication and target 161.8% projection of 1.1494 to 1.0805 from 1.1184 at 1.0069. Nevertheless, break of 1.0641 will indicate short term bottoming and turn bias back to the upside for rebound.

In the bigger picture, break of medium term channel support suggests downside acceleration. Current decline from 1.2348 (2021 high) is probably resuming long term down trend from 1.6039 (2008 high). Decisive break of 1.0339 will confirm this bearish case. Next target is 61.8% projection of 1.3993 to 1.0339 from 1.2348 at 1.0090. This will now remain the favored case as long as 1.0805 support turned resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Apr | 51.4 | 51.6 | 51.5 | |

| 23:50 | JPY | PPI Y/Y Apr | 10.00% | 9.40% | 9.50% | 9.70% |

| 02:00 | CNY | Retail Sales Y/Y Apr | -11.10% | -6.00% | -3.50% | |

| 02:00 | CNY | Industrial Production Y/Y Apr | -2.90% | 0.70% | 5.00% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Apr | 6.80% | 7.00% | 9.30% | |

| 06:00 | JPY | Machine Tool Orders Y/Y Apr P | 25.00% | 30.20% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Mar | -17.6B | 2.3B | -9.4B | -11.3B |

| 12:15 | CAD | Housing Starts Y/Y Apr | 267K | 250K | 246K | 248K |

| 12:30 | CAD | Manufacturing Sales M/M Mar | 2.50% | 2.10% | 4.20% | 5.10% |

| 12:30 | CAD | Wholesale Sales M/M Mar | 0.30% | 0.00% | -0.40% | -0.30% |

| 12:30 | USD | Empire State Manufacturing Index May | -11.6 | 15.5 | 24.6 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals