Dollar rises in early US session after data shows that headline consumer inflation accelerated once again in June, to the highest level since 1981. Yen is currently the worst performing one on rise in US and European benchmark yields. But there is prospect for recovery in Yen, except versus Dollar, if risk off sentiment intensifies. Kiwi is also on the softer side despite RBNZ rate hike earlier today. Euro is under performing Sterling and Swiss Franc. Canadian Dollar is resilient for now and the next move will depend on BoC rate decision.

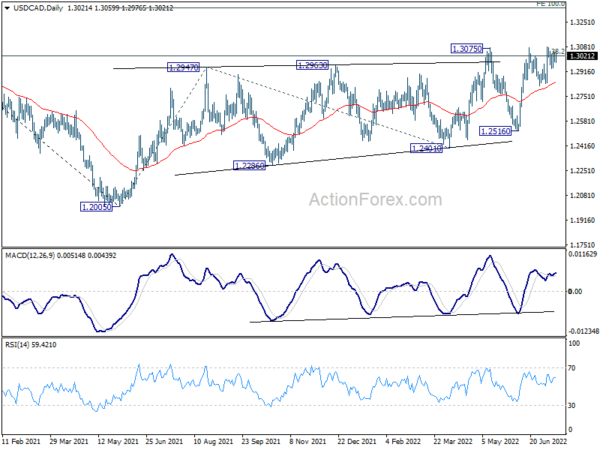

Technically, USD/CAD will be a focus for the rest of the session. Sustained break of 1.3075 resistance will extend larger up trend to 100% projection of 1.2005 to 1.2947 from 1.2401 at 1.3343. If that happens, it would be the final piece to confirm Dollar’s underlying momentum. But, break of 1.2818 near term support will raise the chance of another rejection by 1.3075.

In Europe, at the time of writing, FTSE is down -1.30%. DAX is down -1.87%. CAC is down -1.70%. Germany 10-year yield is up 0.0796 at 1.209. Earlier in Asia, Nikkei rose 0.54%. Hong Kong HSI dropped -0.22%. China Shanghai SSE rose 0.09%. Singapore Strait Times dropped -0.54%. Japan 10-year JGB yield dropped -0.0061 to 0.238.

US CPI accelerated again to 9.1% yoy in Jun, energy up 41.6% yoy, food up 10.4% yoy

US CPI rose 1.3% mom in June, above expectation of 1.0% mom. CPI core rose 0.7% mom, also above expectation of 0.5% mom. Energy index rose 7.5% mom, contributed nearly half of the all items increase. Gasoline index rose 11.2% mom. Food index rose 1.0% mom.

For the 12-month period, CPI accelerated from 8.6% yoy to 9.1% yoy, above expectation of 8.7% yoy. That’s the highest level since November 1981. CPI core (all items less food and energy) slowed slightly from 6.0% yoy to 5.9% yoy, above expectation of 5.7% yoy. Energy index rose 41.6% yoy, highest since April 1980. Food index rose 10.4% yoy, highest since February 1981.

Eurozone industrial production rose 0.8%, mom in May, EU up 0.6% mom

Eurozone industrial production rose 0.8% mom in May, well above expectation of 0.2% mom. Production of non-durable consumer goods rose by 2.7%, capital goods by 2.5% and durable consumer goods by 1.4%, while production of intermediate goods remained unchanged and production of energy fell by -3.3%.

EU industrial production rose 0.6% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+13.9%), Greece (+2.6%) and Czechia (+2.4%). The largest decreases were observed in Lithuania (-7.6%), the Netherlands (-3.3%) and Luxembourg (-2.9%).

UK GDP grew 0.5% mom in May, much better than expectations

UK GDP grew 0.5% mom in May, much better than expectation of 0.0%. Services rose 0.4% mom. Production rose 0.9% mom. Construction also rose 1.5% mom. Monthly GDP is estimated to be 1.7% above its pre-pandemic levels in February 2020. In the three months to May, GDP grew 0.4%. Annual growth in monthly GDP was 3.5% yoy.

Also published, industrial production was up 0.9% mom, 1.4% yoy, versus expectation of 0.0% mom, 1.7% yoy. Manufacturing production was up 1.4% mom, 2.3% yoy, versus expectation of 0.1% mom, 0.3% yoy. Goods trade deficit was little changed at GBP -21.4B, versus expectation of GBP -18.3B.

NIESR forecasts 0.2% growth in UK GDP in Q2

After data showing 0.5% mom GDP growth in UK, NIESR now forecasts 0.2% mom growth in June. For whole of Q2, growth would then be 0.2%. It still forecast a contraction of -0.1% in GDP Q3, with growth likely to slow further as inflation drags on consumer demand.

Rory Macqueen, Principal Economist, NIESR: “If April activity was more encouraging than the headline figure suggested – with strong consumer-facing services dragged down by the reduction in vaccinations – the opposite may be true of May. Headline growth of 0.5 per cent owed much to rising GP visits, while sectors like hospitality, retail and the arts all contracted, suggesting that rising prices may have eaten into discretionary household consumption.

” More encouragingly, manufacturing had its joint strongest month since November 2020, and construction recorded a seventh consecutive month of expansion. With plenty of room for revisions, it looks like touch and go as to whether the UK economy entered recession in the second quarter.”

RBNZ lifts OCR by 50bps to 2.5%, maintains approach of brisk rate hikes

RBNZ raised Official Cash Rate by 50bps to 2.50% as widely expected. The central bank also indicated that it will follow the projected path to raise interest to nearing 3.5% by the end of 2022, and then around 4% in mid-2023.

“The Committee is comfortable that the projected path of the OCR outlined in the recent May Monetary Policy Statement remains broadly consistent with achieving its primary inflation and employment objectives – without causing unnecessary instability in output, interest rates and the exchange rate,” RBNZ said in the statement.

Also, as noted in the summary records of meeting, “The Committee agreed to maintain its approach of briskly lifting the OCR until it is confident that monetary conditions are sufficient to constrain inflation expectations and bring consumer price inflation to within the target range.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 136.39; (P) 136.96; (R1) 137.44; More…

USD/JPY rises in early US session but stays below 137.73 temporary top. Intraday bias remains neutral first. In case of another retreat, downside should be contained by 134.73 support to bring rebound. Firm break of 137.74 will resume larger up trend to 100% projection of 114.40 to 131.34 from 126.35 at 143.29.

In the bigger picture, current rally is seen as part of the long term up trend from 75.56 (2011 low). Next target is 100% projection of 75.56 (2011 low) to 125.85 (2015 high) from 98.97 at 149.26, which is close to 147.68 (1998 high). This will remain the favored case as long as 126.35 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 02:00 | NZD | RBNZ Interest Rate Decision | 2.50% | 2.50% | 2.00% | |

| 06:00 | GBP | GDP M/M May | 0.50% | 0.00% | -0.30% | |

| 06:00 | GBP | Index of Services 3M/3M May | 0.10% | 0.20% | 0.00% | 0.20% |

| 06:00 | GBP | Industrial Production M/M May | 0.90% | 0.00% | -0.60% | -0.10% |

| 06:00 | GBP | Industrial Production Y/Y May | 1.40% | 1.70% | 0.70% | 1.60% |

| 06:00 | GBP | Manufacturing Production M/M May | 1.40% | 0.10% | -1.00% | -0.60% |

| 06:00 | GBP | Manufacturing Production Y/Y May | 2.30% | 0.30% | 0.50% | 1.30% |

| 06:00 | GBP | Goods Trade Balance (GBP) May | -21.4B | -18.3B | -20.9B | -21.5B |

| 06:00 | EUR | Germany CPI M/M Jun F | 0.10% | 0.10% | 0.10% | |

| 06:00 | EUR | Germany CPI Y/Y Jun F | 7.60% | 7.60% | 7.60% | |

| 09:00 | EUR | Eurozone Industrial Production M/M May | 0.80% | 0.20% | 0.40% | |

| 11:00 | GBP | NIESR GDP Estimate (3M) Jun | 0.20% | -0.10% | 0.40% | |

| 12:30 | USD | CPI M/M Jun | 1.30% | 1.00% | 1.00% | |

| 12:30 | USD | CPI Y/Y Jun | 9.10% | 8.70% | 8.60% | |

| 12:30 | USD | CPI Core M/M Jun | 0.70% | 0.50% | 0.60% | |

| 12:30 | USD | CPI Core Y/Y Jun | 5.90% | 5.70% | 6.00% | |

| 14:00 | CAD | BoC Interest Rate Decision | 2.25% | 1.50% | ||

| 14:30 | USD | Crude Oil Inventories | -1.5M | 8.2M | ||

| 18:00 | USD | Fed’s Beige Book |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals