The dollar index is trading just under new highest since Sep 2002, hit on Thursday’s acceleration above 109.00 mark.

The greenback remains well supported by strong risk aversion on global economic and political uncertainty, while the latest talks that the Fed may opt for a super-sized 1% rate hike in its July 26-27 policy meeting, following the latest US inflation report which showed that consumer prices continue to rise.

In addition, data showed that Chinese economy sharply slowed in the second quarter, while political crisis in Italy is deepening and US banking earning season started on a weak tone that adds to negative outlook and further boosts safe-haven flows that supports the US currency.

On the other side, calmer tones come from some Fed policymakers, who favor another 0.75% hike this month that could cool down euphoric sentiment on expectations for more aggressive steps from the US central bank.

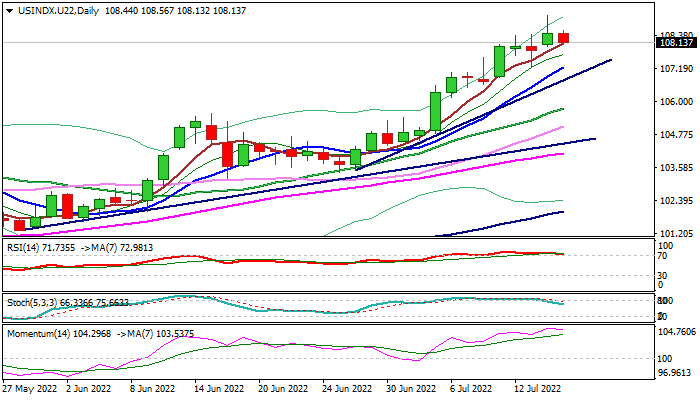

The dollar index is on track for the third consecutive week of gains that is positive signal, but daily studies started to point lower and warn of correction.

Daily stochastic emerged from overbought territory and stretched 14-d momentum is starting to turn south.

The price adjustment is likely to be limited and offer better levels to re-enter strong uptrend, but traders may become more aggressive sellers if the Fed disappoints high expectations.

Dips should stay above rising 10DMA (107.21) and a trendline support (106.98) to keep larger bulls intact.

Res: 108.56; 109.12; 109.67; 110.00

Sup: 108.08; 107.21; 106.98; 106.51

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals