Traders work on the floor of the New York Stock Exchange.

Lucas Jackson | Reuters

The third quarter wraps up in the week ahead with stocks just slightly higher for the period, after a summer of zigzag moves.

The market faces some of the same challenges in the final quarter of the year, including Brexit, the trade war with China, sluggishness in the global economy and the impeachment inquiry into President Donald Trump. By mid-quarter, the U.S. presidential election will be just a year away, and it could become a factor that could start to trigger market volatility.

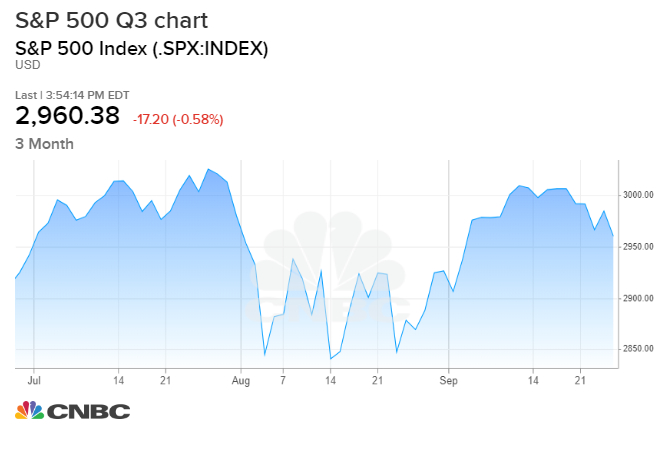

Stocks were lower in the past week, with the S&P 500 down 1%, finishing at 2,961.

For the year to date, the S&P 500 is up 18.1%, but in the third quarter, so far, it added just 0.7%. The S&P started the quarter at 2,752, went as high as 3,028 before falling back. It has chopped in a range down to about 2,860, and has repeatedly struggled to get back to its high.

“We think you stay within the range — 2,820 to 3,030,” said Julian Emanuel, BTIG head equities and derivatives strategist. Emanuel’s year-end target has been 3,000.

“We see new highs, whether they happen in the fourth quarter or in 2020, as a function of geopolitical developments. From our point of view, the developments of the last several weeks, particularly [Sen. Elizabeth] Warren rising in the polls, increases in our mind the probability you get some sort of deal with China,” he said.

Analysts said there could be more volatility because of the efforts by House Democrats to impeach Trump. The investigation into the president has to do with his withholding of aid to Ukraine and whether it was tied to a request to get dirt on front running Democratic presidential candidate former Vice President Joe Biden and his son Hunter.

Warren, D-Mass., whose tax and other policies are viewed as unfriendly to markets, is catching up with Biden in the polls, and some strategists see her benefiting from any negative news on Hunter Biden’s dealings with a Ukraine gas company. Emanuel said if Warren continues to gain, that may encourage China to move forward with a trade deal with Trump, for fear making a deal with Warren would be more difficult.

Besides political headlines, there is some key data coming out in the week ahead, including Friday’s September employment report, and ISM and PMI manufacturing data on Tuesday. The economy is expected to have added 145,000 jobs, above the 130,000 last month, while the unemployment rate is expected to stay steady at 3.7%, according to Refinitiv.

“We expect another month of census-related hiring to push public sector payrolls higher and, as a result, we forecast only 120k increase in private sector payrolls,” notes Michael Gapen, chief U.S. economist at Barclays. “Our forecast for private sector employment gains in September would represent some improvement relative to August, but our forecast overall remains consistent with our outlook for slower employment growth on the heels of deceleration in economic activity.”

There are also a number of Fed speakers scheduled for next week, including New York Fed President John Williams; Cleveland Fed President Loretta Mester, and Boston Fed President Eric Rosengren.

Trade will remain a major topic for markets, as U.S. and Chinese negotiators get closer to Oct. 10 talks. Headlines Friday that the White House is considering blocking or limiting U.S. investments into China sent stocks lower, after optimism about the talks lifted them early in the day.

Emanuel said the fourth quarter may have a different tone from that of the third quarter, after the wild move lower in rates during August and early September. He expects bond yields have bottomed, and he favors some of the cyclical names, like financials and energy.

“The likelihood is long-term yields move higher, and you could see some form of switching out of bond exposure and into stock exposure. That type of embracing of the stock market is typical of final innings,” for markets, he said.

Strategists said the impeachment efforts against Trump may ultimately not have a negative impact on stocks. Even if he is impeached by the House, the Senate would be expected to acquit him. Analysts liken the possible reaction to be more like when President Bill Clinton was impeached and acquitted by the Senate than when President Richard Nixon was facing impeachment proceedings. Nixon resigned before he was impeached.

Stocks gained 28% in the year after impeachment efforts began against Clinton, but lost 39% in the year after they were begun against Nixon.

Emanuel said the 2020 presidential election could also come into play this quarter, and Trump may take actions to boost the economy, such as finding a solution to the trade war with China. A resolution could give a boost to stocks.

“People are very nervous and in general reasonably well-hedged because they remember the fourth quarter of last year so well, and from our point of view, we don’t necessarily see this trading range resolve itself any time soon,” said Emanuel.

Markets will also be watching the Fed’s repo operation Monday. The Fed has been conducting open market operations to assure there is enough cash in the short-term funding market, which was under stress at the start of last week. The Fed has calmed the market, but market pros are watching to see how much activity there is and whether rates rise. The final day of the month typically sees a surge in cash requirements, and on Monday, investors may require cash for the settlement of $113 billion in Treasury securities.

Week Ahead Calendar

Monday

9:45 a.m. Chicago PMI

Tuesday

Monthly vehicle sales

9:15 a.m. St. Louis Fed President James Bullard

9:45 a.m. Manufacturing PMI

10:00 a.m. ISM manufacturing

10:00 a.m. Construction spending

4:15 p.m. Chicago Fed President Charles Evans

Wednesday

8:15 a.m. ADP Employment

10:50 a.m. New York Fed President John Williams

9:15 p.m. Philly Fed President Patrick Harker

Thursday

8:30 a.m. Initial claims

9:45 a.m. Services PMI

10:00 a.m. ISM nonmanufacturing

10:00 a.m. Factory orders

12:10 p.m. Cleveland Fed President Loretta Mester

3:45 p.m. Chicago Fed President Charles Evans

Friday

8:30 a.m. Employment report

8:30 a.m. International trade

10:15 a.m. Boston Federal Reserve President Eric Rosengren

10:25 a.m. Atlanta Fed President Raphael Bostic

1:00 p.m. Minneapolis Fed President Neel Kashkari

Trading at forex

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals