Stock market snapshot as of [1/11/2019 1:40 PM]

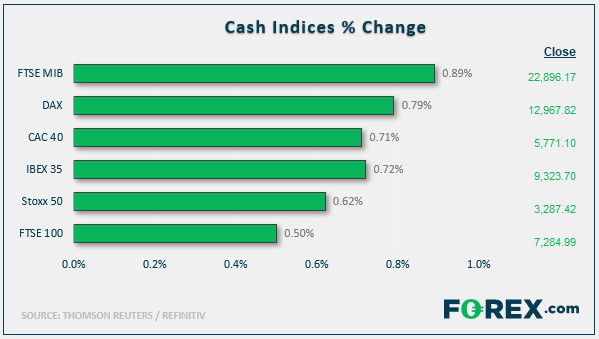

U.S. equities extend gains made by futures markets in the wake of higher than forecast U.S. payrolls, as do European shares. Ahead of the readings, participants had partially discounted the importance of the data, given expectations that they would be strongly impacted by a United Auto Workers strike at some GM plants

In the event, payrolls came in far higher than the 89,000 indicated by consensus forecasts, with a print at 128,000. It’s worth noting that Wall Street’s so-called ‘whisper number’ was reportedly more like 100,000, suggesting that any element of surprise was moderated

The unemployment rate was steady at the multi-decade low of 3.6%. Average hourly earnings were also fairly undramatic, though the monthly growth rate in October of 0.2% was below the 0.3% investors were expecting

Given that payrolls come in the same week of a finely tuned Fed rate cut, in many ways these data were set to be largely neutral for markets. In the end, a slightly stronger than forecast headline did little harm to sentiment, whilst upward revisions of recent months totalling 95,000, maintain a ‘goldilocks’ read of near-term economic and policy prospects

ISM’s manufacturing PMI was more of an also-ran in terms of both market attention and focus, though the headline missed slightly, whilst the key employment component beat forecasts

Initial positive sentiment was propped by a key manufacturing sentiment survey out of China, in the shape of Caixin’s PMI, which beat expectations. The data help nullify a still ambiguous take regarding trade talks, though at least Washington is keeping up positive rhetoric about a phase-1 deal. That contrasts with unnamed officials from Beijing, whose more pessimistic comments upended risk appetite a day ago

Brent crude crossed above the $60/bbl. threshold, with help from the payrolls fillip. LME Copper barely seems to have looked at the data, staying down about 1.9%. Gold slips below $1,510/oz, but the loss on the day is contained to 0.3% ahead of Wall Street’s open

Treasuries and European sovereign bonds mostly ticked into a positive move on the day following an earlier steady tone after the previous session’s advance. This essentially shrugs off payrolls cheer

Stocks/sectors on the move

A return to risk seeking seems reflected in tech shares taking over the lead from miners in European stock markets after the U.S. data. Energy also strengthens as crude oil prices rise, though also with an eye relief from Exxon’s quarterly report

Miners and industrial goods makers remain underpinned in a typical reaction to promising data out of Chin

Heavyweight U.S.-listed stocks are in focus given Europe’s slate light at the end of the week: Exxon (XOM), Chevron (CVX) and Alibaba (BABA). The oil majors saw diverging fortunes in Q3, at least on the surface. CVX blamed its earnings miss on a tax charge as well as weak oil prices. The stock falls 1.3% By contrast, XOM’s EPS topped forecasts, though as with other ‘supermajors’ that have reported this week, there are questions about earnings quality. Exxon estimates collapsed ahead of Friday’s release and a positive tax effect flattered profits. XOM shares rise 1.3%. BABA crushed top and bottom-line views, though the reaction was volatile in pre-market trading as the conference call revealed an “aggressive” push into “lower-tier” cities, whilst cloud revenue growth slackened, even though it advanced 64%. The stock traded 2.3%

FX snapshot as of [1/11/2019 11:50 AM]

FX markets

Early yen gains in follow on from Thursday’s more risk-off feel have been trimmed after the fairly solid U.S. jobs outcome. The Dollar Index has also duly erased the morning’s losses after hitting the lowest since July, last rising a few ticks

The Kiwi is in the spotlight against the greenback and the Aussie. These moves appear largely based on a report by the region’s Westpac bank, suggesting that the RBNZ will probably stand pat at this month’s policy meeting

Norway’s krone keeps a strong lead against G-10 peers after unemployment there fell

The rand edges lower ahead of a sovereign bond rating scheduled from Moody’s late in the European session, with a downgrade widely expected

Upcoming economic highlights

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals