Stock markets rebound strongly in European session, on speculations that ECB could follow Fed to announce new monetary stimulus soon. There are also talks that markets are boosted by former US Vice President Joe Biden’s Tuesday night victories in the Democratic primary for for US presidential candidate. But we’re skeptical on the depth of the correlation. Overall, we’re seeing US stocks, in near term consolidations above last week’s low. Hence, a day up then a day down is nothing something that really surprises us.

Global coronavirus cases continue to surge and reaches 94301 so far, with 3220 deaths. South Korea reaches 5621, with 34 deaths. Iran reaches 2922, with 92 deaths. Italy reaches 2502, with 79 deaths. Japan surges pass 300 to 319. Germany (244), France 212, Spain 193 and USA (128) are all worsening. Switzerland is catching up at 93. Singapore and Hong Kong remain steady at 110 and 103 respectively.

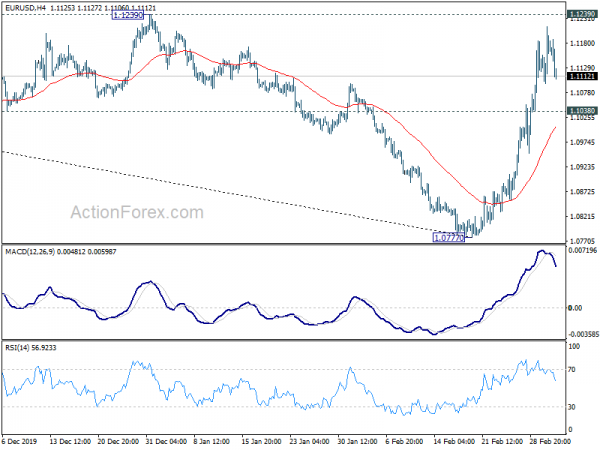

In the currency markets, Euro is currently the weakest, followed by Yen and Swiss Franc. Commodity currencies are the strongest ones for today, led by Aussie. Focus will turn to whether BoC would cut interest rate, and by how much. Technically, EUR/USD is clearly losing a lot of upside momentum ahead of 1.1239 key resistance. Break of 1.1038 minor support will suggest rejection by this key resistance and retain near term bearishness for retesting 1.0777 low first. EUR/GBP also dips ahead of 0.8786 resistance. Break of 0.8594 support will reaffirm the case that price actions from 0.8276 are merely a consolidation pattern. And fall from 0.9324 isn’t over yet.

In Europe, currently, FTSE is up 1.53%. DAX is up 1.31%. CAC is up 1.37%. German 10-year yield is up 0.0059 at -0.619. Earlier in Asia, Nikkei rose 0.08%. Hong Kong HSI dropped -0.24%. China Shanghai SSE rose 0.63%. Singapore Strait Times rose 0.18%. Japan 10-year JGB yield dropped -0.0288 to -0.140.

US ADP jobs rose 183k, job market firewall should weather most coronavirus scenarios

US ADP private employment grew 183k in February, slightly below expectation of 190k. By company size, small businesses added 24k jobs, medium businesses added 26k, large businesses added 133k. By sector, goods-production employment grew only 11k. But service-providing employment surged 172k.

“The labor market remains firm, as private-sector payrolls continued to expand in February,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Job creation remained heavily concentrated in large companies, which continue to be the strongest performer.”

Mark Zandi, chief economist of Moody’s Analytics, said, “COVID-19 will need to break through the job market firewall if it is to do significant damage to the economy. The firewall has some cracks, but judging by the February employment gain it should be strong enough to weather most scenarios.”

UK PMI Services finalized at 53.2, suggests quarterly GDP growth of just over 0.2%

UK PMI Services was finalized at 53.2 in February, down from January’s 53.9. PMI Composite dropped to 53.0, down from 53.3.

Chris Williamson, Chief Business Economist at IHS Markit: “The post-election rebound in service sector growth lost some of its bounce in February, in part due to coronavirus related disruptions to sectors such as travel and tourism, but continued to expand at an encouragingly robust pace.

Alongside an improvement in manufacturing and a return to growth in the construction sector, the survey data are consistent with quarterly GDP growth of just over 0.2%, up from stagnation in the fourth quarter of last year.”

Eurozone PMI composite finalized at 52.6, problems lie ahead

Eurozone PMI Services was finalized at 52.6 in February, slightly up from January’s 52.5. PMI Composite was finalized at 51.6, up from 51.3. Looking at some member stats, they’re generally stuck at rather low expansionary reading. Italy PMI Composite was at 4-month high of 50.7. Germany’s Composite was finalized at 50.7, France at 52.0. Ireland, however, surged to 17-month high at 56.7.

Chris Williamson, Chief Business Economist at IHS Markit said: “The eurozone economy showed resilience to disruptions arising from the coronavirus outbreak in February, but dig deeper into the data and there are signs that problems lie ahead… Exports of both goods and services are now falling at an increased rate due to virus-related downturns in demand, and increasingly widespread delivery delays threaten future production.

“In the service sector, growing numbers of companies are reporting lost business due to the virus spread, notably in sectors such as hotels, travel, transport and tourism but also even in areas such as financial services. While the PMI data so far for the first quarter are signalling a 0.1-0.2% increase in GDP, there are clear downside risks and a likely weakening of the economy in March.”

Also released, Eurozone retail sales rose 0.6% mom in January, matched expectations. Germany retail sales rose 0.9% mom in January, matched expectations. Swiss CPI came in at -0.1% mom, 0.1% yoy in February, versus expectation of 0.3% mom, 0.0% yoy.

Debelle: RBA has capacity to cut one more time, then QE should be considered

RBA Deputy Governor Guy Debelle said the decision to lower interest rate by -0.25% earlier this week was to “support the economy as it responds to the global coronavirus outbreak”. He added that “the coronavirus outbreak overseas is having a significant effect on the Australian economy at present, particularly in the education and travel sectors.”

On monetary policy, Debelle said the central bank has capacity to lower its policy rate one more time. “Beyond that, we will have to consider quantitative easing (QE),” he added. And, “I don’t think negative interest rates are something that would be contemplating.”

Australia GDP grew 0.5% in Q4, remains below long run average

Australia GDP grew 0.5% qoq in Q4, above expectation of 0.4% qoq, but slowed from Q3’s 0.6% qoq. Through the year, the economy grew 2.2%. Household consumption and inventories are the main contributor to growth, followed by imports and government consumptions. Public capital formation and exports provided no contributed while private capital formation was a drag. Chief Economist for the ABS, Bruce Hockman, said: “The economy has continued to grow and picked up through the year, however the rate of growth remains below the long run average.”

China Caixin PMI services dropped to 26.5, necessary to pay attention to divergence of business sentiment

China Caixin PMI Services dropped to 26.5 in February, down from 51.8, well below expectation of 48.0. Markit said the sharply decline in activity was due to travel restrictions and company closures. There were record falls in total new work and export sales. Outstanding work rose substantially. PMI Composite dropped from 51.9 to 27.5.

Zhengsheng Zhong, Chairman and Chief Economist at CEBM Group said: “The coronavirus epidemic has obviously impacted China’s economy. It is necessary to pay attention to the divergence of business sentiment between the manufacturing and the service sectors. While recent supportive policies for manufacturing, small businesses and industries heavily affected by the epidemic have had a more obvious effect on the manufacturing sector, it is more difficult for service companies to make up their cash flow losses.”

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1106; (P) 1.1160; (R1) 1.1223; More…

Intraday bias in EUR/USD is turned neutral as it retreats notably ahead of 1.1239 key resistance. On the upside, decisive break of 1.1239 will confirm medium term bottoming at 1.0777 and turn outlook bullish.. On the downside, break of 1.1038 minor support will turn bias back to the downside for retesting 1.0777 low. That would also retain near term bearishness.

In the bigger picture, as long as 1.1239 resistance holds, larger down trend from 1.2555 (2018 high) is still in favor to extend through 1.0777 low. However, sustained break of 1.1239 will also have 55 week EMA (1.1154) decisive taken out. That should confirm medium term bottoming, with bullish convergence condition in weekly MACD. Further rise could then be seen back to 38.2% retracement of 1.2555 to 1.0777 at 1.1456 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Feb | 42.7 | 41.3 | ||

| 21:45 | NZD | Building Permits M/M Jan | -2.00% | 9.90% | 9.80% | |

| 00:00 | NZD | ANZ Commodity Price Feb | -2.10% | -0.90% | ||

| 00:30 | AUD | GDP Q/Q Q4 | 0.50% | 0.40% | 0.40% | 0.60% |

| 01:45 | CNY | Caixin Services PMI Feb | 26.5 | 48 | 51.8 | |

| 07:00 | EUR | Germany Retail Sales M/M Jan | 0.90% | 0.90% | -3.30% | |

| 07:30 | CHF | CPI M/M Feb | -0.10% | 0.30% | -0.20% | |

| 07:30 | CHF | CPI Y/Y Feb | 0.10% | 0.00% | 0.20% | |

| 08:45 | EUR | Italy Services PMI Feb | 52.1 | 51.5 | 51.4 | |

| 08:50 | EUR | France Services PMI Feb F | 52.5 | 52.6 | 52.6 | |

| 08:55 | EUR | Germany Services PMI Feb F | 52.5 | 53.3 | 53.3 | |

| 09:00 | EUR | Eurozone Services PMI Feb F | 52.6 | 52.8 | 52.8 | |

| 09:30 | GBP | Services PMI Feb F | 53.2 | 53.3 | 53.3 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Jan | 0.60% | 0.60% | -1.60% | -1.10% |

| 13:15 | USD | ADP Employment Change Feb | 183K | 191K | 291K | 209K |

| 13:30 | CAD | Labor Productivity Q/Q Q4 | -0.10% | 0.20% | 0.20% | |

| 14:45 | USD | Services PMI Feb F | 49.4 | 49.4 | ||

| 15:00 | USD | ISM Non-Manufacturing PMI Feb | 55.5 | 55.5 | ||

| 15:00 | CAD | BoC Interest Rate Decision | 1.25% | 1.75% | ||

| 15:30 | USD | Crude Oil Inventories | 2.8M | 0.5M | ||

| 16:15 | CAD | BoC Press Conference | ||||

| 19:00 | USD | Fed’s Beige Book |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals