- Hopes for a production-cut deal by OPEC today catapult oil higher

- Deal will likely get done, yet any positive reaction in oil may be short lived

- Stocks climb with crude, but watch out for US jobless claims today

- Euro will stay tuned to the Eurogroup meeting – are Eurobonds on the menu?

Oil jumps on signs a deal is near, but caution warranted

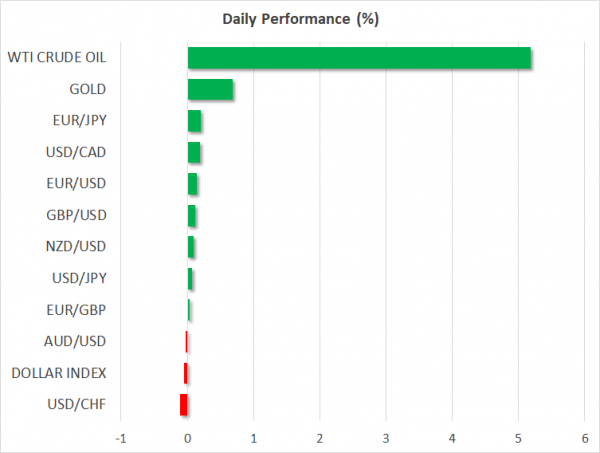

The energy market has come back into the spotlight ahead of the meeting between OPEC and Russia today at 14:00 GMT, where expectations are riding high for a deal to cut oil production and shore up prices. Algeria’s energy minister was the latest to play up the prospect of an agreement yesterday, saying that output could be cut by as much as 10 million barrels per day (mbp/d).

While that was hardly surprising given recent news, oil prices still jumped as investors became more confident that the talks won’t fall apart. Reports that Russia is willing to cut 1.6 mbp/d and comments from a Texas oil regulator that US producers will cut ‘4 mbp/d in the next 3 months organically’ added credibility to this prospect.

All told, it seems rather likely that a deal will be hashed out. The real question is how much will be cut, and from what baseline. Will a 10 million cut be calculated from today’s output levels, which are roughly 3 million barrels higher than a month ago, before Saudi Arabia and Russia went on a production spree? If that’s the case, then the real cut will only be around 7 million barrels.

Even if the real cut is 10 million though, that’s still unlikely to stabilize the market. Most estimates suggest oil demand will take a hit of around 20-30 million barrels, so the market will still be left oversupplied on a scale never seen before.

Therefore, while prices could jump on the headlines of a deal, there’s a high risk any gains will remain short-lived or that the size of the cuts will disappoint investors, leading to a ‘sell the fact’ reaction in oil. In the FX market, this could spell more pain for oil-sensitive currencies like the Canadian dollar, Norwegian krone, Russian ruble, and Mexican peso.

Stocks follow oil higher – will US data today matter?

Wall Street continues to defy the mounting evidence that the real economy is unraveling, instead taking heart from signs the US is approaching ‘peak virus’. The S&P 500 gained 3.4% yesterday and is primed for a higher open today, with markets taking off after Democratic Senator Bernie Sanders dropped out of the presidential race. The recovery in oil prices added fuel to the rally.

This rebound will be put to the test today though, when US initial jobless claims hit the wires. Forecasts suggest that another 5 million Americans filed for unemployment benefits last week. If met, that would push the total number of job losses up to ~15 million just in the last three weeks. For perspective, the entire American workforce is 163 million.

A disappointing set of jobless data could throw a monkey wrench into the stock rally, though contrary to conventional wisdom that might boost the dollar, which has been acting like a safe haven amidst all the chaos. Admittedly, when the ‘going gets tough’, all investors and corporates want to hold is the dollar – it’s stable, liquid, and accepted everywhere.

Fed Chairman Powell will speak at 14:00 GMT.

Euro braces for more Eurogroup disappointment

The Eurozone’s finance ministers will resume talks on coordinated fiscal measures today at 15:00 GMT. For the euro, what really matters is whether this will open the door for the creation of Eurobonds, which still seems unlikely given persistent opposition from Germany and the Netherlands.

That said, the risks appear asymmetric. With nobody really expecting a breakthrough, a Eurobond agreement could push the euro much higher, whereas another disappointment may only elicit minor losses.

Finally, the minutes of the latest ECB meeting today will likely be seen as outdated. The same holds for the Canadian jobs report, as those data were collected before the nation went into lockdown.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals