Dollar’s weakness continues today as largest GDP contraction in more than a decade gives no help. A wave of selling is seen in Sterling in European session. Yet there was no sustainable momentum so far. Yen is follow as the third weakest on mild yet solid risk appetite. Commodity currencies are currently strongest. Focus will turn to FOMC rate decision next.

Fed is generally expected to keep monetary policies unchanged today. There will be no formal economic projections until June, which is agreeable as everything ties to how the coronavirus pandemic is contained. Nevertheless, Fed chair Jerome Powell could still offer a glimpse of what he expected in the second half, and he view on the shape of the recovery. Guidance on interest rates would be something to watch too. Powell has ruled out negative rates for now and we’ll see if he sticks to the same position.

Suggested readings:

In other markets, DOW is current up nearly 400 pts at initial trading. Gold is gyrating in tight range around 1700 handle. WTI crude oils is having a solid rebound, back above 15. In Europe, FTSE is up 2.08%. DAX is up 1.84%. CAC is up 1.40%. German 10-year yield is down -0.0283 at -0.496. Earlier in Asia, Nikkei dropped -0.06%. Hong Kong HSI rose 0.28%. China Shanghai SSE rose 0.44%. Singapore Strait Times rose 0.46%. Japan 10-year JGB yield dropped -0.0075 to -0.045.

US GDP shrank -4.8% in Q1, worst since 2008

US GDP contracted -4.8% annualized in Q1 slightly worse than expectation of -4.0% annualized. That’s the largest decline since 2008 and marked the formal start of a recession.

Looking at some details, personal consumption expenditures dropped -7.6%. Gross private domestic investment dropped -5.6%. Exports of goods and services dropped -8.7% while imports dropped -15.3%> Government consumption expenditures and gross investment rose 0.7%.

Price index for gross domestic purchases rose 1.6%. PCE price index rose 1.3%, slowed from 1.4%. PCE core price index rose 1.8%, up from 1.3%.

Eurozone economic sentiment crashed to 67, but stays above 2009 low

Economic sentiment “crashed” in both Eurozone and EU in April. Eurozone Economic Sentiment Indicator dropped -27.2 pts to 67.0. EU ESI dropped -28.8 pts to 65.8. These were the strongest decline in the ESI on record since 1985. The indicators are now far below their long run averages of 100 and very close to the lowest levels registered during the Great Recession in 2009.

Industrial confidence dropped -19.2 to -30.4, steepest monthly fall on record, but remained above 2009 low. Services confidence dropped -32.7 pts to record low of -35.0. Consumer confidence dropped -11.1 to -22.7. Retail trade confidence dropped -19.7 to -28.3. Employment expectations dropped -30.1 to 63.7.

Amongst the largest euro-area economies, the ESI crashed in the Netherlands(-32.6), Spain (-26.0), Germany (-19.9), and France (-16.3),2 while no data could be collected in Italy due to the strict confinement measures.

UK Raab: No intention of changing Brexit transition period

UK Foreign Minister Dominic Raab said said today that the government’s “position is unchanged” regarding Brexit. That is, “the transition period ends on the 31st of December, that is enshrined in law.”

He further told the parliament, “there is no intention of changing that and actually what we should do now … is focus on removing any additional uncertainty, doing a deal by the end of the year and allowing both the UK and the European Union and all of its member states to bounce back as we come through the coronavirus.”

Australia CPI jumped to 2.2% in Q1, highest since 2014

Australia CPI rose 0.3% qoq in Q1, above expectation of 0.2% qoq. Annually, CPI accelerated to 2.2% yoy, up from 1.8% yoy, beat expectation of 2.0% yoy. The annual rate was also the highest level since Q3 of 2014. RBA trimmed mean CPI rose 0.5% qoq, slightly above expectation of 0.4% qoq. Annual rate also accelerated to 1.8% yoy, up from 1.6% yoy and beat expectation of 1.6% yoy.

ABS Chief Economist, Bruce Hockman said: “There were some price effects of COVID-19 apparent in the March quarter due to higher purchasing of certain products towards the end of the quarter, as restrictions came into effect… More evident effects of COVID-19 are expected in the June quarter CPI.”

New Zealand imports and exports surged in March, but trade with China shrank

New Zealand’s imports rose 7.7% yoy to NZD 5.1B in March while exports rose 3.8% yoy to NZD 5.8B. Trade surplus came in at NZD 672m, smaller than expectation of NZD 700m.

Trade with its largest partner, China, continued to drop. Imports from China dropped -10% yoy to NZD 714m. Exports to China dropped -5.8% yoy to NZD 1.4B. Meanwhile, exports to Australia also dropped -8.9% yoy to NZD 738m. But exports to US rose 9.4% to NZD 623m. Exports to EU rose 8.2% yoy to NZD 595m. Exports to Japan also rose 22% yoy to NZD 352m.

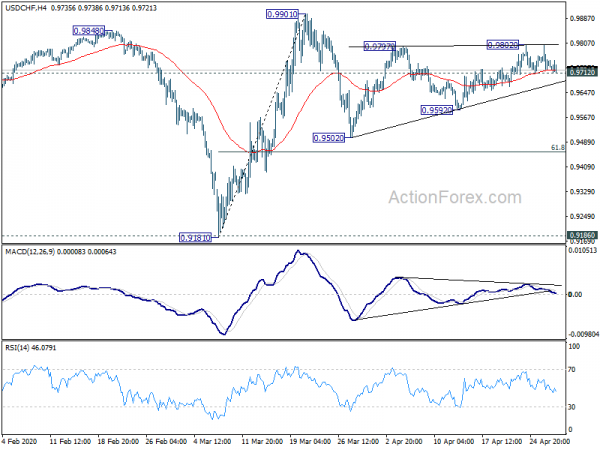

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9714; (P) 0.9757; (R1) 0.9793; More…

Intraday bias in USD/CHF remains neutral with focus on 0.9712 minor support. Break there will extend the consolidation pattern from 0.9901 with another falling leg. Intraday bias will be turned to the downside for 0.9592 support first. In this case, downside should be contained by 61.8% retracement of 0.9181 to 0.9901 at 0.9456 to rebound. On the upside, break of 0.9502 will target a test on 0.9901 high.

In the bigger picture, decline from 1.0237 is seen as the third leg of the pattern from 1.0342 (2016 low). It could have completed at 0.9181 after hitting 0.9186 key support (2018 low). Break of 0.9901 will extend the rebound form 0.9181 through 1.0023 resistance. After all, medium term range trading will likely continue between 0.9181/1.0237 for some more time.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Mar | 672M | 700M | 594M | 531M |

| 23:01 | GBP | BRC Shop Price Index Y/Y Mar | -0.70% | -0.80% | ||

| 01:30 | AUD | CPI Q/Q Q1 | 0.30% | 0.20% | 0.70% | |

| 01:30 | AUD | CPI Y/Y Q1 | 2.20% | 2.00% | 1.80% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q1 | 0.50% | 0.40% | 0.40% | 0.50% |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q1 | 1.80% | 1.60% | 1.60% | |

| 06:00 | EUR | Germany Import Price Index M/M Mar | -3.50% | -2.30% | -0.90% | |

| 08:00 | CHF | ZEW Survey – Expectations Apr | 12.7 | -45.8 | ||

| 09:00 | EUR | Eurozone Economic Sentiment Apr | 67 | 75 | 94.5 | 94.2 |

| 09:00 | EUR | Eurozone Services Sentiment Apr | -35 | -2.2 | -2.3 | |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -22.7 | -22.7 | -22.7 | |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | -30.4 | -25 | -10.8 | -11.2 |

| 09:00 | EUR | Eurozone Business Climate Apr | -1.81 | -0.28 | ||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Mar | 7.50% | 5.50% | 5.50% | |

| 12:00 | EUR | Germany CPI M/M Apr P | 0.30% | 0.00% | 0.10% | |

| 12:00 | EUR | Germany CPI Y/Y Apr P | 0.80% | 0.60% | 1.40% | |

| 12:30 | USD | GDP Annualized Q1 P | -4.80% | -4.00% | 2.10% | |

| 12:30 | USD | GDP Price Index Q1 P | 1.40% | 1.00% | 1.40% | 1.30% |

| 14:00 | USD | Pending Home Sales M/M Mar | -10.00% | 2.40% | ||

| 14:30 | USD | Crude Oil Inventories | 11.2M | 15.0M | ||

| 18:00 | USD | Fed Interest Rate Decision | 0.25% | 0.25% | ||

| 18:30 | USD | FOMC Press Conference |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals