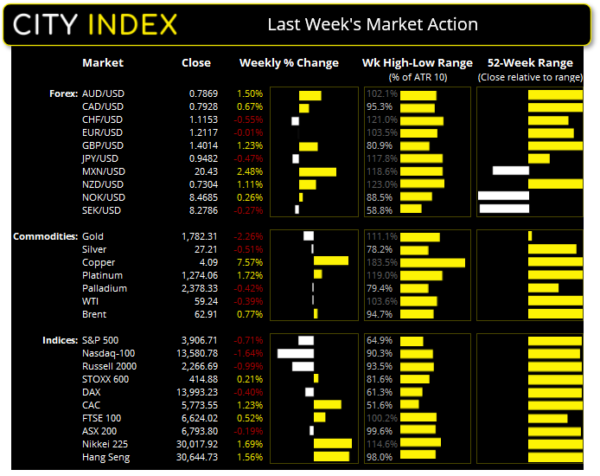

AUD and NZD pairs rallied into the weekly close on Friday as commodities and, in particular copper, pushed aggressively higher.

Commodities chalked up another broad rise last week, with the CRB index (commodities index) rising for a fourth consecutive week and closing at its highest level since November 2018. The index is a basket of 19 commodities ranging from energy, agriculture and metals and is a good barometer for inflationary pressures. And the index has risen by over 30% since the March lows then markets are clearly pricing in inflation.

But it was copper prices which stole the show after its bullish run increased its magnitude and closed above $4 for the first time since August 2011. Gaining an impressive 7.5% last week alone, upside pressures increased due to demand optimism for copper as Chinese investors returned to their desks.

Gold remains unloved after breaking beneath key support at 1764 and producing a bearish engulfing week. However, Friday’s bullish outside candle suggests the potential for a little mean reversion from recent lows, with 1800 being the next obvious target.

WTI closed the week back below $60 and has formed a bearish hammer on the weekly chart. Brent closed at 62.91 and formed a bearish pinbar on the weekly chart. With prices looking stretched to the upside and signs that the Texas freeze is thawing, we are on guard for a potential correction from current levels.

Commodity currencies rally

The Australian dollar was the strongest major last week, with most of its gains coming through on Friday as copper broke to new highs. Closing the week at its most bullish level since March 2018 and just shy of 0.8000 one must question at what point the RBA will try and jawbone their currency. Whilst AUD was the strongest, commodity FX in general enjoyed a weaker dollar environment, with CAD, NZD and MXN also pushing firmly higher against the greenback.

The British pound closed above 1.4000 and at its highest level since April 2018. Confidence of a faster vaccine rollout remains a key driver behind the pound’s strength, although any bumps in the road regarding vaccinations are likely to show up in price action too.

Further signs of a weaker dollar emerged on the yen. A bearish hammer has formed on the USD/JPY weekly chart after a failed break above its 50-week eMA, so we question whether the high may already be in place.

Weekly repositioning for FX majors was relatively light, with all futures seeing less than 10k contracts changed compared with the prior week. The largest weekly change was seen on Japanese yen futures where traders increased their net-bullish exposure by 9.4k contracts (2.6%)

Interestingly, traders reduced net-bullish exposure to the Swiss franc by -13.1%. Given the strength of CHF pairs over recent weeks and the temporary break above 118 on CHF/JPY, perhaps traders are increasingly concerned that the SNB (Swiss National Bank) will intervene to weaken their currency. This means net-long exposure to Swiss franc futures are their least bullish since July 2020.

Net-long exposure to copper futures remained just below record highs. Although bullish exposure may well now be at a record level given the explosively bullish price action in the second half of last week.

Despite gold’s weaker performance over the last few months traders remain overwhelmingly net-long, with bulls outnumbering bears by a ratio of 4.4:1. However, short interest increased by its largest amount in four months last week.

GBP/NZD rolls over at its 200-day eMA

A potential bearish swing trade may have formed on GBP/NZD. The weekly chart remains in a longer-term downtrend and produced a bearish pinbar, after Friday’s bearish engulfing candle eradicate all gains seen between Monday and Thursday. A break beneath last week’s low (1.9167) confirms the bearish reversal candle.

We can see on the daily chart that a bearish engulfing candle saw prices roll over at the 200-day eMA. This average was last tested in October where a bearish engulfing candle also formed ahead of -6.5% decline.

Switching to the four-hour chart shows prices broken below a bullish trendline which suggests a change in trend. Given the decline stopped just above the 1.9160 swing low, we see the potential for a minor rebound from current levels. Yet this may provide an opportunity to fade into the rebound and target lower support levels.

- Bears can seek to fade into minor rallies above 1.9160.

- The broken trendline or the 38.2% Fibonacci retracement level could aid with trade entry level.

- A break below 1.9160 brings 1.9000 into focus.

- It is a quiet start to the week for Asian economic data.

- Christine Lagarde speaks at the European Semester Conference at 00:45 Tuesday morning.

Watchlist update:

USD/JPY: Removed from watchlist. Prices broken beneath 105.75 to invalidate the original bullish bias.

CHF/JPY: Prices failed to hold above key resistance around 118.60 and produced a weekly bearish pinbar and a bearish engulfing on Friday. The near-term bias remains bearish below Friday’s high and potential targets include 117 and the low around 116.13 – 27.

GBP/CHF: The breakout from its basing pattern has performed well and is already over halfway to hitting its longer-term target around 1.9000. We continue to favour longs upon low volatility retracements or breakouts to new highs. The near-term bias remains bullish above the 1.2490 swing low (H4).

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals