Implied volatility, synonymous with expected volatility, is a variable that shows the degree of movement expected for a given market or security. Often labeled as IV for short, implied volatility quantifies the anticipated magnitude, or size, of a move in an underlying asset.

WHAT IS IMPLIED VOLATILITY?

Implied volatility is a number displayed in percentage terms reflecting the level of uncertainty, or risk, perceived by traders. IV readings, which are derived from the Black-Scholes options pricing model, can indicate the degree of variation expected for a particular equity index, stock, commodity, or major currency pair over a stated period of time.

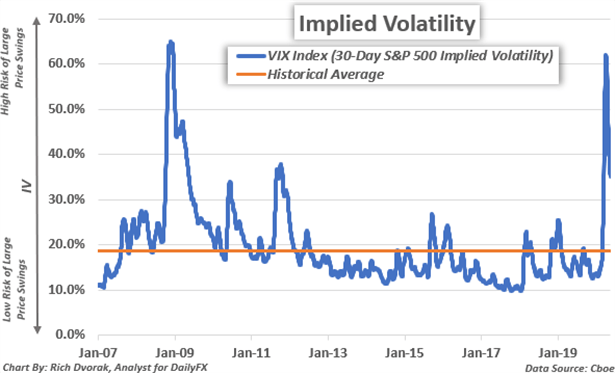

Implied volatility readings have a direct impact on the price of option contracts and are thus important metrics tracked by options traders. Several other market participants analyze and pay close attention to implied volatility as well seeing that useful insight that can be garnered and incorporated into a trading strategy. The well-known VIX Index, for instance, is simply the 30-day implied volatility reading derived from at-the-money S&P 500 option prices.

A high VIX level (i.e. percent), or implied volatility reading, indicates that stock market risk is relatively elevated and there is a greater chance of larger than normal price swings over the specified time frame. A greater range of potential outcomes, in turn, leads to higher implied volatility readings, and corresponds with a higher options contract price for the underlying asset.

This positive relationship between implied volatility and options contract price is true for both call options and put options. To be clear, this is assuming all other variables in the options contract pricing model are held constant. Aside from directly impacting option contract prices, there are multiple applications for analyzing implied volatility. Some examples include looking at differences between implied volatility and realized volatility, gauging market sentiment, identifying support and resistance levels, and finding relationships across asset classes.

Recommended by Rich Dvorak

Building Confidence in Trading

IMPLIED VOLATILITY VS HISTORICAL VOLATILITY – WHAT IS THE DIFFERENCE?

Implied volatility is the expected size of a future price change. Implied volatility broadly reflects how big or small of a move is anticipated to be over a particular time frame. On the other hand, historical volatility, or realized volatility, indicates the actual size of a previous price change. Historical volatility illustrates the overall level of market activity that has already been observed.

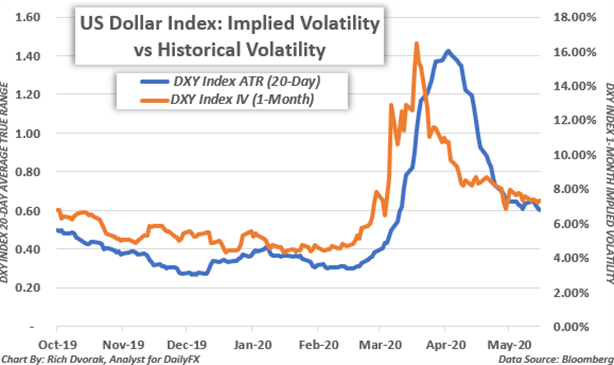

The average true range (ATR) of an asset or security is an example of an indicator that illustrates historical volatility. Though implied volatility and historical volatility differ slightly in the regard of future expectations versus past observations, the two metrics are closely related and tend to move in similar patterns.

Recommended by Rich Dvorak

Check out our latest list of top trading opportunities.

Implied volatility readings are typically higher when there is a large degree of uncertainty corresponding with potential for market impact – and often surrounds economic data releases or other scheduled risk events like central bank meetings. This can lead to larger price swings and thus can materialize into higher readings of realized volatility. Likewise, when historical volatility remains anchored during calm market conditions, or when perceived risk is relatively subdued, IV tends to be lower.

IMPLIED VOLATILITY CAN REFLECT MARKET RISK AND UNCERTAINTY

Implied volatility is a projection of how much market movement is anticipated – regardless of the direction. In other words, implied volatility reflects the expected range of potential outcomes and uncertainty around how high or low an underlying asset might rise or fall.

High implied volatility indicates there is a greater chance of large price swings expected by traders whereas low implied volatility signals that the market expects price movements to be relatively tame. Implied volatility measurements can also help traders gauge market sentiment considering IV broadly depicts the level of perceived uncertainty – or risk.

IMPLIED VOLATILITY TRADING RANGES CAN INDICATE TECHNICAL SUPPORT AND RESISTANCE LEVELS

Implied volatility measurements can be incorporated into various trading strategies as well. This is due to their usefulness for identifying potential areas of technical support and resistance. An implied volatility trading range is typically calculated under the assumption that prices will stay contained within a one-standard deviation move. Mathematically, this means that there is a 68% statistical probability that price action will fluctuate within the defined implied volatility trading range over a specified time frame.

That said, if prices trade at the upper barrier of its pre-defined implied volatility trading range, then there is an 84% statistical probability that prices will gravitate lower and a 16% probability that prices will continue rising. On the other hand, if prices trade at the lower barrier of its pre-defined implied volatility trading range, then there is an 84% statistical probability that prices will drift higher and a 16% probability that prices will continue falling.

ADVANTAGES OF IMPLIED VOLATILITY AS A FOREX SIGNAL

Largely owed to the inherent mean-reverting characteristic of major currency pairs, implied volatility trading ranges typically serve as robust forex signals. For example, this EUR/GBP analysis that defined a 24-hour implied volatility trading range for EUR/GBP provided an illustrated example of how these technical barriers can help traders identify possible inflection points and trading opportunities.

On 14 January 2020, spot EUR/GBP price action was trading at 0.8541 and its implied volatility measurement was clocked at 7.3% for the overnight (i.e. 1-day) options contract. Using these value inputs, and the options-derived trading range formula below, it was estimated that EUR/GBP would fluctuate between implied support of 0.8508 and implied resistance of 0.8574 over the next 24-hours with a 68% statistical probability.

In other words, the calculated 24-hour trading range reflected a 1-standard deviation implied move of

+/- 0.0033 from spot, which meant that Euro-Pound volatility was expected to be contained within a 66- pip band around its then-current price of 0.8541 for the 15 January 2020 trading session.

Recommended by Rich Dvorak

Forex for Beginners

As trading progressed and market activity unfolded, EUR/GBP jumped to an intraday high of 0.8578, but the currency pair closed the 15 January 2020 session at 0.8547 after spot prices pivoted sharply lower. This was driven by an influx of selling pressure that followed a rejection of its implied high technical barrier.

USING IMPLIED VOLATILITY TO TRADE COMMODITIES, STOCKS, & INDICIES

In addition to forex, implied volatility gauges can be incorporated into trading strategies for commodities, stocks, and indices. As mentioned above, measures of implied volatility can indicate the market’s overall level of uncertainty. Correspondingly, cross-asset implied volatility benchmarks tend to reflect useful relationships with their respective underlying markets and may provide insight as to where that market might head next.

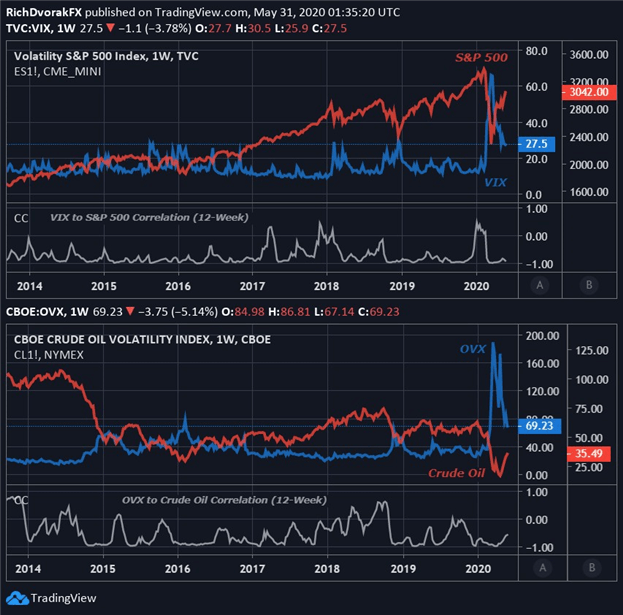

Chart created by Rich Dvorak with TradingView

Arguably the most popular implied volatility benchmark is the S&P 500 VIX Index. The VIX Index typically rises amid turbulent market conditions and increasing uncertainty, though the ‘fear-gauge’ tends to soar during aggressive selloffs in stocks. In turn, the VIX generally holds a strong inverse relationship with the S&P 500.

The OVX Index, which reflects 30-day expected crude oil price volatility, provides an example of another commonly cited IV benchmark. Seeing that the price of crude oil and stocks react similarly to deteriorating risk appetite, it is unsurprising that sentiment-linked crude oil frequently maintains a negative correlation with both the VIX and OVX.

Chart created by Rich Dvorak with TradingView

Although this inverse relationship typically observed between an asset’s price and its implied volatility reading serves as a general rule of thumb, that is not always the case and there are certain exceptions. The correlation of price with implied volatility is dynamic, meaning it is constantly changing, which corresponds with a relative strengthening or weakening from their historical relationship.

Recommended by Rich Dvorak

Get Your Free USD Forecast

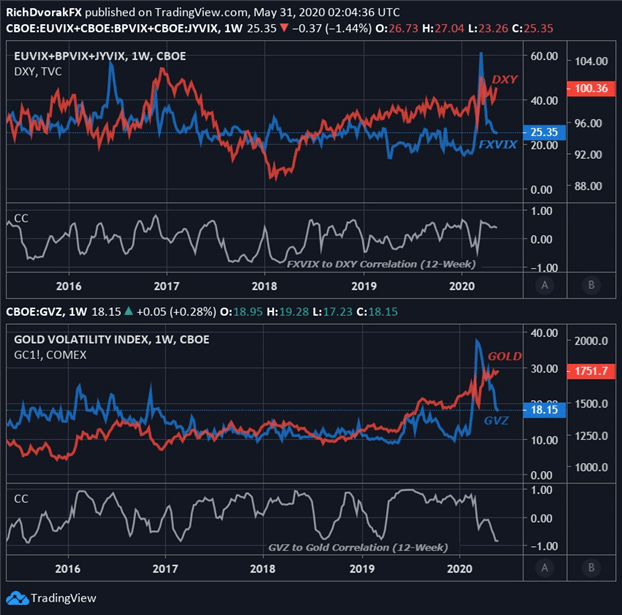

Similarly, when it comes to common safe-haven assets, a direct relationship between price and implied volatility may show. For instance, the US Dollar Index (DXY) broadly follows the ebb and flow of expected currency volatility (FXVIX). Also, a positive correlation is often reflected by the price of gold and gold volatility (GVZ). These examples help illustrate the valuable insight that implied volatility readings can provide when incorporated into macro approaches and other comprehensive trading strategies.

Open a demo FX trading account with IG and trade currencies that respond to systemic trends.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals