Lower treasury yields helped buoy Wall Street overnight, with the Nasdaq 100 leading the rally with a 1.5% gain.Lower treasury yields helped buoy Wall Street overnight, with the Nasdaq 100 leading the rally with a 1.5% gain.

Asian Futures:

- Australia’s ASX 200 futures are up 20 points (0.28%), the cash market is currently estimated to open at 7,065.90

- Japan’s Nikkei 225 futures are up 160 points (0.56%), the cash market is currently estimated to open at 28,524.61

- Hong Kong’s Hang Seng futures are up 98 points (0.35%), the cash market is currently estimated to open at 28,510.26

UK and Europe:

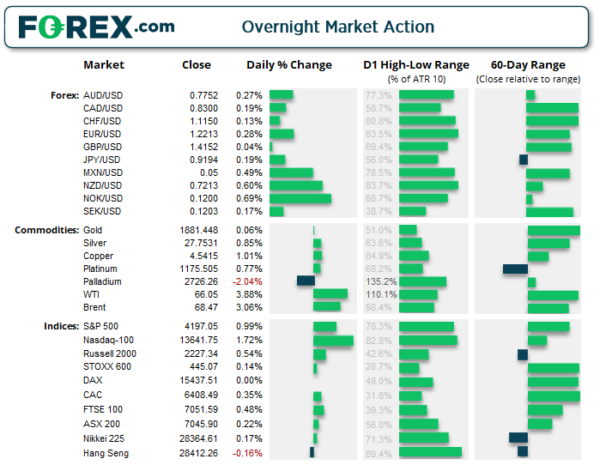

- UK’s FTSE 100 index rose 33.54 points (0.48%) to close at 7,051.59

- Europe’s Euro STOXX 50 index rose 9.8 points (0.24%) to close at 4,035.58

- Germany’s DAX index rose 67.25 points (0.44%) to close at 15,437.51

- France’s CAC 40 index rose 22.08 points (0.35%) to close at 6,408.49

Monday US Close:

- The Dow Jones Industrial rose 186.14 points (0.54%) to close at 34,393.98

- The S&P 500 index rose 41.19 points (1%) to close at 4,197.05

- The Nasdaq 100 index rose 230.016 points (1.72%) to close at 13,641.75

Wall Street points to a firmer open for Asian indices:

Sentiment was also lifted by a minor rebound on Bitcoin, which rose to a two-day high. The US 10-year yield (1.6%) fell -2bps and the 30-year (2.3%) was down -3bps. The S&P 500 rose 1% to a two-week high, led by communication services sector (1.84%) and technology (1.76%). MGM Resorts (MGM), Caesars Entertainment and Twitter were the top performing stocks, rising 5.1%, 4.9% and 4.8% respectively. But it was the Nasdaq 100 that was the top performer with a 1.7% rise which also closed to a two-week high. The Dow Jones was up 0.5% and the Russell 2000 rose 0.55% (growth stocks rose 0.65% and value stocks rose 0.45%).

Futures are pointing to a firmer open for Asia with SPI 200 futures up 0.28%, Hang Seng futures rising 0.35% and CSI300 futures currently 0.49% higher.

The ASX 200 is set to open just beneath Wednesday’s high (which was a large bearish candle). This also takes prices just above the 20-day eMA, so it’s a distinct possibility we could see prices break above 7066 and head for the 7085 swing high if Wall Street’s sentiment is carried over to Asian trade today. Whether it can muster up the strength to rest the 7100 handle remains to be seen but a daily close above 7085 would be constructive. It would take a break below 7000 to regain our bearish interest on the daily chart.

ASX 200 Market Internals:

ASX 200: 7045.9 (0.22%), 24 May 2021

- Healthcare (1.49%) was the strongest sector and Materials (-1.09%) was the weakest

- 8 out of the 11 sectors closed higher

- 3 out of the 11 sectors outperformed the ASX 200

- 118 (59.00%) stocks advanced, 73 (36.50%) stocks declined

- 3 hit a new 52-week high, 2 hit a new 52-week low

- 66.5% of stocks closed above their 200-day average

- 40.5% of stocks closed above their 20-day average

Outperformers:

- + 14.7% – Kogan.com Ltd (KGN.AX)

- + 5.82% – Gold Road Resources Ltd (GOR.AX)

- + 5.09% – Westgold Resources Ltd (WGX.AX)

Underperformers:

- -4.60% – OZ Minerals Ltd (OZL.AX)

- -4.17% – Fortescue Metals Group Ltd (FMG.AX)

- -3.56% – AMP Ltd (AMP.AX)

NZD was the strongest FX major:

The New Zealand dollar was the strongest major overnight, seeing NZD/USD produce a bullish engulfing candle and rise broadly against its peers. As NZD/JPY also rose to the top of its 3-day range it has failed to break beneath key support at 77.90 (and its 50-day eMA) so the anticipated bearish breakout is now on ice.

The British pound was effectively flat yet is holding steady around 3-month highs after BOW (Bank of England) Governor Andrew bailey said he des not see long-term implications from a pickup in inflation, in his annual report to the Treasury committee. GBP/CAD broke beneath Friday’s (bearish outside day) low to suggest is corrective swing high formed last week in line with our bearish bias in yesterday’s report.

AUD/NZD produced its fourth bearish hammer which closed beneath the 1.0800 handle to underscore the level’s significance, and now just below the midway point of its 1.0715 – 1.0800 range.

EUR/JPY trying to build a base above 132.50

EUR/JPY remains in a strong uptrend since its May 2020 low, and trading just off its highs and currently on track for its seventh consecutive bullish month. However, prices failed to hold above the September 2018 high which triggered a corrective phase, but a bullish engulfing candle around the 132.50 support zone suggests the correction may now be complete. Prices have since pulled back on the four-hour chart but remain above the 50-day eMA, so we’re now looking for bullish momentum to return and challenge the highs around 133.13/21.

Our bias remains bullish above 132.48 (but hopefully a higher low will form to allow for tighter risk management).

The initial target is the September 2018 high then the May high. But if the trend has truly resumed it should break to new highs.

Copper defies China’s commodity price crackdown

Copper prices shook off concerns of China’s latest crackdown on rising commodities prices and

printed a bullish hammer, with its lower wick perfectly respecting the 4.435 low and closing at the

day’s high. Whilst it remains unclear whether this is the corrective low, it appears bulls are at least trying to carve one out. Our bias remains bullish above the 4.3755 – 4.4350 support zone.

Gold remains just off its 4-month highs around 1880, unable to push higher yet reluctant to retrace. At this stage we’d see any spikes lower as merely a shakeout ahead of its next leg high, and our bias remains bullish above the 1808 low which leaves plenty of wriggle room for such spikes should they materialise.

Oil prices rallied for a second consecutive day to close at a four-day high as concerns over Iranian oil exports continued to subside. WTI settled back above 66.0 whilst brent now trades at 68.49.

Up Next (Times in AEST)

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals