Sterling suffered a lot of volatility today. It surged on stronger than expected consumer inflation data, but then reversed on news that UK Prime Minister Theresa May’s rejection of EU’s Irish border proposal. The Pound sort of stabilized then as markets await what May is going to say exactly in the EU summit in Salzburg. For now, Sterling is the second weakest one for today, following Swiss Franc. On the other hand, Australian Dollar is the strongest one as risk markets have already left escalation in US-China trade war behind.

Recent strength is global treasury yield is worth a note. US 10 year yield broke 3% handle this week and is so far staying firm. German 10 year yield trades slightly lower at 0.48 but it’s on track to take on 0.5 key resistance zone. This is seen as a major factor in driving down the Japanese Yen and, to a lesser extent the Swiss Franc. Meanwhile, 10 year Japan JGB yield has another strong rally today after BoJ rate announcement. It closed up 0.058 at 0.122, hitting the highest level since January 2016. This could be the factor that gives the Swiss Franc extra pressure.

Major European indices are generally higher today. At the time of writing, FTSE is up 0.17%, DAX up 0.14% and CAC up 0.21%. Earlier in Asia, Nikkei closed up 1.08%, Hong Kong HSI gained 1.19% and Singapore Strait Times rose 1.19%. China SSE rose 1.14% to 2730.85, taken 2700 handle out firmly. There was no impact on sentiments after this week’s escalation in US-China trade war. SSE is now suddenly looking back at 2800 resistance zone again.

Technically, it now looks like USD/CHF has formed a short term bottom at 0.9599. Focus is back on 0.9757 minor resistance for confirmation. EUR/CHF is also also looking at 1.1342 resistance to confirm bottoming back at 1.1178. It remains to be seen if this is just Swiss Franc’s weakness or it’s general among European majors. EUR/USD struggles below 1.1733 resistance and could be dragged down easily.

Released in US session, housing starts rose to 1.28m annualized rate in August, building permits dropped to 1.23m. Current account deficit narrowed to USD -101B in Q2. These data are ignored by traders.

Sterling knocked down as UK PM May said to reject EU Barnier’s proposal

Sterling is knocked down heavily after the Times reported that Prime Minister Theresa May will reject EU negotiator Michel Barnier’s “improved” proposal regarding Irish border. Focus will now be on what May would say at the two-day EU summit in Salzburg today.

Earlier, the Guardian reported that May hit back at Barnier’s criticism on her Cheques Plan. May wrote in Die Welt that “there have been arguments made against our proposals that have been at odds with the reality of trade negotiations elsewhere and indeed the current trading relationship between EU member states”.

And she emphasized “neither side can demand the unacceptable of the other, such as an external customs border between different parts of the United Kingdom – which no other country would accept if they were in the same situation – or the UK seeking the rights of EU membership without the obligations.”

UK CPI accelerated to 2.7%, beat BoE’s projections

Sterling surges broadly, but briefly, after stronger than expected consumer inflation reading. Headline CPI jumped to 2.7% yoy, up from 2.5% yoy and beat expectation of 2.4% yoy. Core CPI also accelerated to 2.1% yoy, up from 1.9% yoy and beat expectation of 1.8% yoy. The headline inflation reading is notably higher than BoE’s own projection of 2.5% as projected in the latest inflation report. That could prompt policy rethink among BoE MPC members. And inflation hawks likes Michael Saunders now have some reasons to strike back.

Also released, RPI jumped to 3.5% yoy, up from 3.2% yoy and beat expectation of 3.4% yoy. PPI input slowed to 8.7% yoy, down from 10.3% yoy. PPI output slowed to 2.9% yoy, down from 3.1% yoy. PPI output core slowed to 2.1% yoy, down from 2.3% yoy. Also from UK, house price index accelerated to 3.1% yoy in July, above expectation of 2.9% yoy.

Also released in European session, Eurozone current account surplus narrowed to EUR 21.3B in July.

BoJ kept short term rate at -0.10%, asset purchase as JPY 80T pa

BoJ left monetary policies unchanged as widely expected. Short term policy interest was held at -0.10%. BoJ will also continue with JGB purchase to keep 10 year yield at around 0%, but allow it to “move upward and downward to some extent”. Annual pace of monetary base expansion is kept at JPY 80T. The decision was made by 7-2 vote. Harada opposed again on allowing yield to move in a range as that’s “too ambiguous” as guideline. Kataoka continued his push to “strengthen monetary easing”.

The central bank expected the economy to “continue its moderate expansion”. Domestic demand is likely to “follow an uptrend”. Exports are expected to continue the “moderate increasing trend”. CPI is “likely to increase gradually toward 2 percent, mainly on the back of the output gap remaining positive and medium- to long-term inflation expectations rising”

Risks to outlook include US macroeconomic policies, consequences of protectionist moves, developments in emerging and commodity-exporting economies, Brexit and geopolitical risks.

Also from Japan, trade deficit widened to JPY -0.19T in August.

BoJ Kuroda watching US-China trade war with grave concern

BoJ Governor Haruhiko Kuroda warned in the post meeting press conference “protectionism could affect not only the countries that are engaged (in trade wars) but the global economy as a whole through supply chains.” He added that the BoJ is “watching developments with grave concern.” For the moment, Kuroda said “it’s hard to say what specific impact this could have”. But he noted “there could be wide-ranging effects, given the complex global supply chain in the world economy.”

On monetary policy, he said that “we must maintain our powerful monetary easing given it will take time to achieve our inflation target.” And, if 2% inflation is met, “we won’t be continuing our current unconventional policy”. Also, he commented on the bond market activity since BoJ explicitly allowed 10 year JGB yield to move between -0.1% and 0.1%. He said “bond market trading activity has heightened somewhat… but trading tends to thin in August of each year, so it’s too early to gauge the impact of our July decision.”

South Korean Moon del cared era of no war with North Korean Kim

South Korean President Moon Jae-in had a rather successful summit, the third one this year, with North Korean Leader Kim Jong-Un. Speaking at a joint news conference in Pyongyang after the meeting, hey pledged to turn Korean peninsula into “land of peace without nuclear weapons and nuclear threats” and take “prompt steps” toward the goal.

Kim added that “the world is going to see how this divided nation is going to bring about a new future on its own”. Meanwhile, Moon said “the era of no war has started,” and “today the North and South decided to remove all threats that can cause war from the entire Korean peninsula.”

According to Moon, Kim also “expressed its readiness” on permanent dismantlement of its main nuclear facilities in Yongbyon. However, correspondingly measures have to be taken by the US.

Trump, like a cheerleader on the sideline, tweeted “Kim Jong Un has agreed to allow Nuclear inspections, subject to final negotiations, and to permanently dismantle a test site and launch pad in the presence of international experts. In the meantime there will be no Rocket or Nuclear testing.” But again, there was no well deserved credit given to Moon.

Chinese Premier Li: One-way depreciation of the yuan brings more harm than benefits for China

Chinese Premier Li Keqiang said in a forum today that the talk of China deliberately weakening the Yuan exchange rate was “groundless”. He added that “one-way depreciation of the yuan brings more harm than benefits for China.” Also, a weaker currency “will only come at a cost of damaging China’s economic environment”.

And he pledged that “China will never go down the road of relying on yuan depreciation to stimulate exports.” Instead, China would “tick to market-oriented foreign exchange reform”. But he also said, the currency would be kept “basically stable at an adaptive level”.

On US-China trade war, Li said “no unilateralism will offer a viable solution”. Instead, “it is essential that we uphold the basic principles of multilateralism and free trade.” He noted intellectual property theft would be “dealt with seriously” with “doubled or even tripled unaffordable penalties” for breaches in order to ensure firms are “comfortable” bringing their business to China.

Li also said China is “deeply integrated into the world economy, the Chinese economy is inevitably affected by notable changes in the global economic and trade context.” And he admitted that “we’re facing greater difficulties in keeping stable performance of the Chinese economy.” But he also indicated Beijing has “prepared sufficient tools for us to deal with risks and challenges” and added that “these policy tools will boost China’s resilience to cope with various challenges and difficulties.”

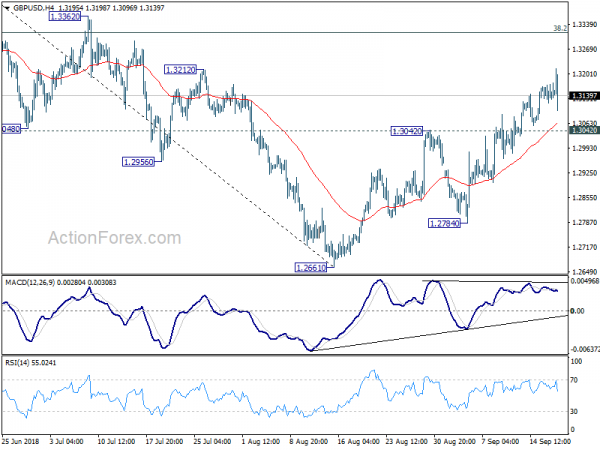

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3120; (P) 1.3146; (R1) 1.3173; More…

GBP/USD spiked higher to 1.3214 but quickly retreated. At this point, further rise is still expected in the pair. Rebound from 1.2661 might extend towards 1.3316 key fibonacci level. However, as such rebound is seen as a corrective move, upside should be limited by 1.3316 to bring near term reversal. On the downside, break of 1.3042 resistance turn support will argue that rebound from 1.2661 might be completed. In such case, intraday bias will be turned back to the downside for 1.2784 support to confirm.

In the bigger picture, whole medium term rebound from 1.1946 (2016 low) should have completed at 1.4376 already, after rejection from 55 month EMA (now at 1.4062). The structure and momentum of the fall from 1.4376 argues that it’s resuming long term down trend. And this will be the preferred case as long as 38.2% retracement of 1.4376 to 1.2661 at 1.3316 holds. However, firm break of 1.3316 would bring stronger rebound to 61.8% retracement at 1.3721. And, the eventual depth of the fall from 1.4376, and the chance of hitting 1.1946 low, will depend on the strength of the interim corrective rebound from 1.2661.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| JPY | BoJ Rate Decision | -0.10% | -0.10% | |||

| 22:45 | NZD | Current Account (NZD) Q2 | -1.62B | -1.32B | 0.18B | 0.09B |

| 23:50 | JPY | Trade Balance (JPY) Aug | -0.19T | -0.14T | -0.05T | -0.10T |

| 00:30 | AUD | Westpac Leading Index M/M Aug | 0.10% | 0.00% | ||

| 08:00 | EUR | Eurozone Current Account (EUR) Jul | 21.3B | 22.4B | 23.5B | |

| 08:30 | GBP | CPI M/M Aug | 0.70% | 0.50% | 0.00% | |

| 08:30 | GBP | CPI Y/Y Aug | 2.70% | 2.40% | 2.50% | |

| 08:30 | GBP | Core CPI Y/Y Aug | 2.10% | 1.80% | 1.90% | |

| 08:30 | GBP | RPI M/M Aug | 0.90% | 0.60% | 0.10% | |

| 08:30 | GBP | RPI Y/Y Aug | 3.50% | 3.40% | 3.20% | |

| 08:30 | GBP | PPI Input M/M Aug | 0.50% | 0.40% | 0.50% | 0.00% |

| 08:30 | GBP | PPI Input Y/Y Aug | 8.70% | 9.10% | 10.90% | 10.30% |

| 08:30 | GBP | PPI Output M/M Aug | 0.20% | 0.20% | 0.00% | |

| 08:30 | GBP | PPI Output Y/Y Aug | 2.90% | 2.90% | 3.10% | |

| 08:30 | GBP | PPI Output Core M/M Aug | 0.10% | 0.20% | 0.00% | 0.10% |

| 08:30 | GBP | PPI Output Core Y/Y Aug | 2.10% | 2.10% | 2.20% | 2.30% |

| 08:30 | GBP | House Price Index Y/Y Jul | 3.10% | 2.90% | 3.00% | |

| 12:30 | USD | Current Account (USD) Q2 | -101B | -103B | -124B | -122B |

| 12:30 | USD | Housing Starts Aug | 1.28M | 1.24M | 1.17M | |

| 12:30 | USD | Building Permits Aug | 1.23M | 1.31M | 1.31M | 1.30M |

| 14:30 | USD | Crude Oil Inventories | -2.7M | -5.3M |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals