The US dollar is higher against most major currencies on Friday. The Canadian dollar was the single currency that appreciated versus the greenback. The loonie moved higher at the end of the week with the release of a stronger than expected monthly GDP number. The softer trade comments also helped dissipate the risk aversion sentiment lifting the Canadian currency. Oil prices in North America are higher as lower supply due to disruptions put WTI crude above $74. US jobs data will be released on Friday, July 6 at 8:30 am EDT with Canadian employment data also due at that time.

- RBA expected to keep rates unchanged on Tuesday

- FOMC meeting minutes to be published on Thursday

- Canadian and US employment data due on Friday

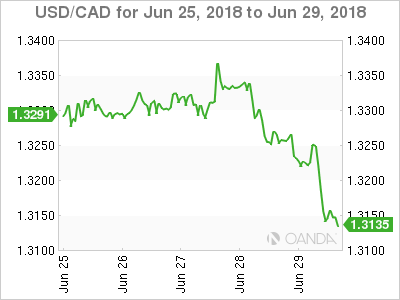

Loonie Gets GDP Boost as Canadian Economy Gains Traction

The USD/CAD lost 0.82 percent in the last five days. The currency is trading at 1.3152 after a stronger than expected monthly Canadian GDP datapoint. The gross domestic product gained 0.1 percent in April as 12 out of the 20 industrial sectors had positive results. Manufacturing was the biggest contributor with 0.8 percent growth. The loonie rose after the positive economic indicator could support a rate move by the Bank of Canada (BoC) on July 11. The BoC Governor has sent mixed messages, but a 70 percent chance of a lift in interest rates has been priced in by the market. The CAD touched 10 day highs after being under pressure due to trade war rhetoric and soft economic data.

Canadian businesses remain optimistic as evidenced by the Bank of Canada (BoC) Business Outlook Survey published on Friday. The main caveat is the survey was taken a month ago, before anti-trade comments reached a different pitch. The decision by the central bank will be guided by additional data with the upcoming Canadian jobs report on Friday a big factor. Businesses anticipate higher employment with a growing number reporting labor shortages. The Canadian economy is on track to print a 2 percent gain in the second quarter, putting an end to three quarters below that level. The developments in the trade front are sure to influence the final decision by the BoC.

EUR Steadier After EU Summit Agrees on Migrant Deal

The EUR/USD gained 0.09 percent during the week. The single currency is trading at 1.1666 in a volatile week that has seen the USD rise as trade war rhetoric escalated and the German Chancellor was under pressure to deliver a united response to the immigrant crisis in Europe. The EU summit appears to be headed for a positive outcome for Merkel and she might have done enough earn the support from the coalition partner CSU. Jobs weeks in the US will also feature the ISM manufacturing PMI data on Monday with a steady reading of 58.2 expected.

The economic calendar holds more clues for the direction of the USD than the EUR. The US stock market has bounced back and might be prove to be immune from trade war comments adding more support for the greenback. Friday’s U.S. non farm payrolls (NFP) is expected to add another 200,000 jobs to the economy and hourly earning to gain 0.3 percent validating the Fed’s tightening pace. The market is pricing in another rate hike in September with the CME FedWatch tool showing a 72.9 percent of higher rates at the end of the Federal Open Market Committee (FOMC) meeting on September 26.

Higher oil prices have pushed inflation above the European Central Bank (ECB) target, but with other indicators not showing the same upward trend the central bank will be slow to act with interest rates in Europe to continue at record low until the third quarter of 2019.

Yen Slips as Market Moves on from Risk Aversion

The USD/JPY rose 0.79 percent in the previous five sessions. The currency pair is trading at 110.85 after the return of risk appetite hit the safe haven yen. The more amicable comments from the Trump administration regarding trade, with China in particular, triggered more selling for holders of short USD/JPY positions. The USD is not out of the woods yet, the new tariffs for Chinese imports kicking in on July 6.

WTI Rises With US Drawdowns and Lower Supply

The West Texas Intermediate is trading at weekly highs of $74.32 after lower than expected crude inventories in the US and supply disruptions in Canada and Libya. The American crude benchmark is higher than the price of Brent given the decision by Saudi Arabia to increase supply to Europe. A bigger drawdown and the after effect of the Iranian agreement have put the WTI in higher demand.

Market events to watch this week:

Monday, July 2

- 4:30am GBP Manufacturing PMI

- 10:00am USD ISM Manufacturing PMI

Tuesday, July 3

- 12:30am AUD RBA Rate Statement

- 4:30am GBP Construction PMI

- 9:30pm AUD Retail Sales m/m

- 9:30pm AUD Trade Balance

Wednesday, July 4

- 4:30am GBP Services PMI

Thursday, July 5

- 6:00am GBP BOE Gov Carney Speaks

- 8:15am USD ADP Non-Farm Employment Change

- 10:00am USD ISM Non-Manufacturing PMI

- 11:00am USD Crude Oil Inventories

- 2:00pm USD FOMC Meeting Minutes

Friday, July 6

- 8:30am CAD Employment Change

- 8:30am CAD Trade Balance

- 8:30am CAD Unemployment Rate

- 8:30am USD Average Hourly Earnings m/m

- 8:30am USD Non-Farm Employment Change

- 8:30am USD Unemployment Rate

*All times EDT

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals