Yen surges broadly today as risk aversion dominates the markets. Italy is at the center of storm as yield spread with Germany stays above 300 alarming level, on concerns over budget deficit. Despite criticism from EU and risk of credit rating downgrade, the populist government doesn’t appear to be interested in backing down. While Euro is the second weakest one, Sterling is even worse as Brexit optimism is put into question again. Meanwhile, Australian Dollar follow Yen as the second strongest, then New Zealand Dollar. Then lack of reaction in Aussie and Kiwi suggests that today’s moves are not too much related to Asia.

At the time of writing, CAC is trading down -1.13%, DAX down -1.05% FTSE down -0.87%. German 10 year yield is down -0.042 at 0.535. Italian 10 year yield is up 0.188 at 3.594. Earlier today, China Shanghai SSE ended down -3.72% at 2716.51. Considering that Chinese markets were on holiday for the whole of last week, today’s fall, which large, isn’t something unexpected. If not for the PBoC’s RRR cut, the decline could be worse. Hong Kong HSI ended down -0.80%, Singapore Strait Times down -0.88%. Nikkei was on holiday today.

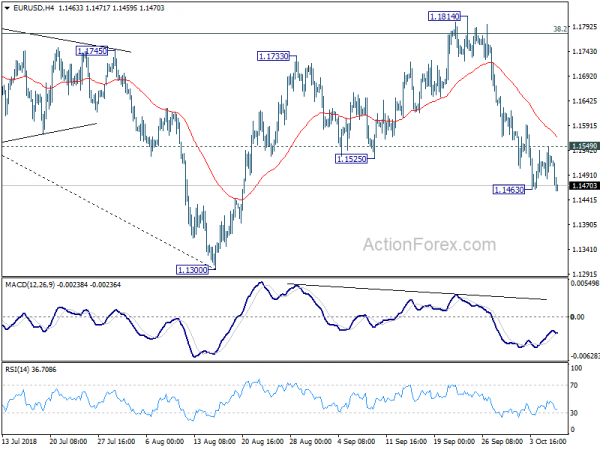

Technically, EUR/USD’s break of 1.1463 temporary low suggests decline resumption. For now, recovery is EUR/GBP is far rather weak. GBP/USD is held well above 1.3002 minor support, GBP/JPY well above 145.67 support. Thus, there is no clear sign of reversal in the Pound yet, despite today’s sharp “pull back”. The question is rather on how far the Japanese could go.

Fed Bullard: Growth surprise allowed Fed to normalize as planned

St. Louis Fed President James Bullard said in at a forum in Singapore that growth in US is on track to beat forecast for three consecutive years from 2017 to 2019. And he discussed a few consequences of the growth surprise. Firstly, it allowed Fed to normalize monetary policy along its projected path. Secondly, it helped profitability of U.S. firms, helping to drive U.S. equity markets higher. Thirdly, Dollar has naturally strengthened in 2018 (due in part to the larger growth surprise domestically).

Bullard added that “faster productivity growth” is needed to maintain the current real GDP growth rate. “A switch to the high state for labor productivity growth would raise the U.S. potential growth rate to a stunning 3.4 percent.” However, he noted “this switch is a possibility, but it has not materialized so far.”

Italy Salvini vows “we will not backtrack”

Italian Deputy Prime Minister, League leader Matteo Salvini insisted today that “we will not backtrack, we will not backtrack” referring to the 2019 budget deficit target. He blamed the volatility in the markets on speculators that are taking advantages. Salvini said “If one had evil thoughts, he would think there are people betting on the spread because they don’t want Italy to grow and create jobs”. And, “speculators acting like (George) Soros are betting on Italy’s collapse to buy at discount prices the healthy companies, and there are many of them, that have remained in this country.”

Salvini also warned that credit agencies have to be fair on Italy. He said “I hope no one has prejudice toward this government, or strange intentions.” Moody’s is going to review Italy’s Baa2 rating, with negative outlook, by the end of October. S&P will also review the BBB with stable outlook rating on October 26.

Eurozone Sentix Investor Confidence dropped to 11.4 on Italy and German auto industry

Eurozone Sentix Investor Confidence dropped to 11.4 in October, down from 12, matched expectations. Sentix noted in the release “uncertainties about the fiscal policy stance in Italy and the automobile industry in Germany are depressing the sentiment”. Meanwhile, the US economy remains strong with “assessment of the situation rises to an all-time high and raises investors’ expectations of rising inflation rates and a restrictive central bank policy”. Sentix added the situation value at 66.5 “signal overheating”.

On Eurozone, Sentix said the economy is “recording a further slight slowdown”. That was attributable to current situation values which dropped to 33.0, lowest since April 2017. But Sentix also said the data “do not represent a fundamentally new assessment by investors” as expectation value was “hardly changed”.

German industrial production dropped -0.3% mom vs expectation of 0.4% rise

German industrial production dropped -0.3% mom in August, much worse than expectation of 0.4% mom rise. Recent batch of soft data confirmed that growth momentum has slowed further in 2018. And some concerns were raised as the slowdown could be deeper than expected. In particular, German PMI composite has dropped to a 2-month low of 55.0 in September. Q3 growth is unlikely to match Q2’s 0.5%. The government’s economic projections to be updated this Thursday will shed some mor lights on the outlook.

Brexit optimism put into question again

Sterling tumbles today as Brexit optimism is put into question again. It’s reported that Brexit Minister Dominic Raab is not going to Brussels this week for the talk on Irish border. And, Prime Minister Theresa May’s office doesn’t expect a deal at the European Council next week.

May’s spokesman is also quoted saying that the withdrawal deal with EU will not be agreed without securing a “precise future framework” on relationship. The spokesman also emphasized that there’s a difference between optimistic talk and getting an agreement. He urged EU to move it position.

Separately, according to a document seen by Reuters, EU insisted that it’s own Irish border backstop proposal as “pragmatic” that “built on existing health checks on animals and agricultural goods between mainland Britain and Northern Ireland.

China Caixin PMI services rose to 53.1, PMI composite composite at 52.1

China Caixin PMI services rose to 53.1 in September, up from 51.5 and beat expectation of 51.5. Caixin PMI composite rose 0.1 to 52.1, showing that overall business activity expanded modestly at the end of Q3. Still, the rate of activity growth remains lackluster compares to earlier in 2018.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said in the release that the PMI composite indicated “stable” performance for the month. However, “demand remained subdued as the growth rate for new orders, although marginally higher than the previous month, lingered at a low level.” Also, “the deterioration in employment will test policymakers’ determination in pressing ahead with reforms.” The employment sub-index hit the lowest level since August 2016.

China Eases Monetary Policy Further, Intervening to Avoid Sharp Fall in Renminbi

Over the weekend, China announced to cut RRR by 100 bps, effective October 15 and applicable to all types of banks, including large commercial banks, joint-stock banks, city commercial banks, non-county rural commercial banks, and foreign banks whose current RRR stand at 15.5% (large banks) or 13.5% (small to medium banks). The move would release a total of RMB 1.2 trillion in liquidity, of which 450B is for offsetting maturing Medium-Term Lending Facility (MLF) loans and the rest (RMB 750B) injected into the banking system. PBOC reinforced that it would maintain the “prudent and neutral” monetary policy, and keep the renminbi (Chinese yuan) movement stable. More in China Eases Monetary Policy Further, Intervening to Avoid Sharp Fall in Renminbi.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1486; (P) 1.1518; (R1) 1.1551; More…..

EUR/USD’s breach of 1.1463 suggests resumption of fall from 1.1814. Intraday bias is turned back to the downside for retesting 1.1300 low next. On the upside, above 1.1549 minor resistance will now indicate short term bottoming and bring lengthier consolidation. But for now, we’d hold on to the view that correction from 1.1300 has completed at 1.1814. Thus, we’d expect upside to be limited well below 1.1814 to bring another decline to 1.1300 eventually.

In the bigger picture, corrective pattern from 1.1300 could have completed at 1.1814 after hitting 38.2% retracement of 1.2555 to 1.1300at 1.1779. Decisive break of 1.1300 will resume the down trend from 1.2555 to 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. On the upside, break of 1.1814 will delay the bearish case and extend the correction from 1.1300 with another rise before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:45 | CNY | Caixin China PMI Services Sep | 53.1 | 51.5 | 51.5 | |

| 5:45 | CHF | Unemployment Rate Sep | 2.50% | 2.50% | 2.60% | |

| 6:00 | EUR | German Industrial Production M/M Aug | -0.30% | 0.40% | -1.10% | -1.30% |

| 8:30 | EUR | Eurozone Sentix Investor Confidence Oct | 11.4 | 11.4 | 12 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals