Dollar softens mildly against European majors in early US session after weaker than expected job data. But risk aversion remains the overall theme of the market. Australian Dollar stays the weakest one, followed by Canadian and New Zealand Dollar. WTI crude oil is back at 51.2 as even though OPEC+ might agree to a production cut next yet, the number could be more symbolic than substantial. Meanwhile, Yen remains the strongest ones, followed by Europeans. Sterling is somehow hibernating, waiting for next week’s Brexit vote in UK Commons.

Some attributed stocks selloff to arrest of Chinese tech giant Huawei’s CFO in Canada, on request by the US. There are worries that such act could jeopardize US-China trade truce. And there are talks that investors simply don’t believe there’s anything concrete out of the Trump-Xi meeting. But we’d like to point out again that US Trade Representative Robert Lighthizer was assigned to take over the negotiation. Lighthizer is the only one in the cabinet who knows how to make a trade agreement, like the USMCA. And he’s now leaving EU Trade Commission Cecilia Malmtrom behind, with focus turned to China. That’s strong enough a signal that both sides are going to deliver something solid in the next 90 days or so. Or at least, Trump believes so.

Instead, we’d point to the sharp decline in bond yields and stocks as sign of worry in global slow down. Japan 10 year JGB yield closed at 0.05 today, lowest close since July. And it hit as high as 0.166 just back in early October. German 10 year bund yield is now down -0.027 at 0.250. It hit as low as 0.244, lowest since the one day spike low of 0.186 in June. If only daily close is considered, 10 year bund yield is at lowest since April 2017. US 10 year yield opens lower again and breaks 2.9 handle to 2.887. DOW futures is currently down -400 pts.

Technically, EUR/USD, USD/CHF, GBP/USD, USD/JPY, EUR/JPY are bounded in familiar range. USD/CAD is showing some convincing to holding itself above 1.3385 key resistance. 1.3685 fibonacci level would be next target should WTI crude oil breaks below 50 handle again. AUD/USD is now pressing 0.7199 support. EUR/AUD is also smelling 1.5781 resistance. Break of these two level will prompt deeper selloff in the Aussie.

US ADP jobs missed expectation, growth still strong but likely peaked

US ADP report showed only 179k growth in private sector jobs in November, down from 225k and missed expectation of 200k.

In the release, Ahu Yildirmaz, vice president and co-head of the ADP Research Institute, noted that “although the labor market performed well, job growth decelerated slightly”. Also, “Midsized businesses added nearly 70 percent of all jobs this month. This growth points to the midsized businesses’ ability to provide stronger wages and benefits. It also suggests they could be more insulated from the global challenges large enterprises face.”

Mark Zandi, chief economist of Moody’s Analytics, said, “Job growth is strong, but has likely peaked. This month’s report is free of significant weather effects and suggests slowing underlying job creation. With very tight labor markets, and record unfilled positions, businesses will have an increasingly tough time adding to payrolls.”

US initial jobless claims dropped -4k to 231k in the week ending December 1, above expectation of 226k. Four-week moving average of initial claims rose 4.25k to 228.0k. Continuing claims dropped -74k to 1.631M in the week ending November 24. Four-week moving average of continuing claims rose 250 to 1.667M.

Also released, US trade came in at USD -55.5B in October, slightly wider than expectation of USD -55.2B. Non-farm productivity was revised down to 2.3% in Q3 and unit labor cost revised down to 0.9%. From Canada trade deficit came in wider than expected at CAD -1.2B in October.

UK PM May on Brexit vote: My deal, no deal, or no Brexit

In a BBC radio interview, UK Prime Minister Theresa May tried to play down the chance of delaying the December 11, Tuesday, Brexit vote in the parliament. And she added what she’s doing is leading up to the vote, rather than talking about delaying it.

May said that there are three options for the MPs. The first one is leaving EU with a deal, that is her deal. Second is leading EU with no deal. And the final one is having no Brexit at fall. She also insisted that if the deal is voted down, it’s up for those who opposed to propose a plan B.

Separately, the European Court of Justice said it will deliver the judgement, on December 10 at 0800GMT, on whether UK can unilaterally reverse Brexit. That would be a day ahead of the scheduled UK parliamentary vote. Earlier this week, ECJ’s advocate general said that UK has the right to withdraw Brexit notice unilaterally, up to the point of formal conclusion of the deal. It’s generally expected, while not binding, ECJ will follow the advocate’s opinion.

MOFCOM: China and US working towards removing all “raised” tariffs

Chinese Commerce Ministry spokesman Gao Feng repeated in a regular press briefing that the meeting between Xi and Trump in Argentina was “very successful and has reached important consensus on economic and trade issues.” He added both countries have “high degree of interest in economic and trade issues and have natural and complementary structural need”. And team from both sides are working closely to reach an agreement within the next 90 days. He also added the “ultimate goal” is to cancel all “raised” tariffs. (He didn’t say all tariffs).

Gao also explained that the agreement will start with agricultural products, energy, automobiles, etc. And both sides would “immediately implement specific issues that the two sides have reached consensus.” During the 90 days period, there will be “conduct consultations on issues such as intellectual property protection, technical cooperation, market access, and trade balance”, in accordance with a clear timetable and roadmap.

Besides, “in the fields of protecting intellectual property rights, promoting fair competition, and relaxing market access” Gao said “China and the United States and enterprises of both countries share common demands, which is also in line with China’s consistent direction of deepening reform and opening up”.

BoJ Kuroda: Risks tilted toward the downside

BoJ Governor Haruhiko Kuroda warned today that “risks to Japan’s economy are tilted toward the downside” And BoJ policymakers “need to pay particular attention to protectionist moves such as Sino-U.S. trade friction.”

Kuroda also warned that “raising interest rates now to create policy space for future economic downturns may risk delaying achievement of our inflation target.”

Also, it’s premature to reveal the exit strategy for the ultra loose monetary policy. Kuroda said “we need to debate an exit strategy and explain it to markets but only when inflation approaches our target.”

RBA Debelle: There’s scope to cut rates and QE is an effective option

RBA Deputy Governor Guy Debelle reiterated in a speech that the central bank’s rhetorics that the “next move in monetary policy is more likely up than down, though it is some way off.” But he also emphasized that there is “still scope for further reductions in the policy rate”, referring monetary capacity.

Debelle also said RBA has learned from the experience of other central banks using other tools of monetary policy. And “QE is a policy option in Australia, should it be required.” He added that “there are less government bonds here, which may make QE more effective.” Besides, he added “floating exchange rate matters and remains an important shock absorber for the Australian economy.”

Released from Australia, trade surplus came in smaller than expected at AUD 2.32B in October. Retail sales rose 0.3% mom in October, matched expectations.

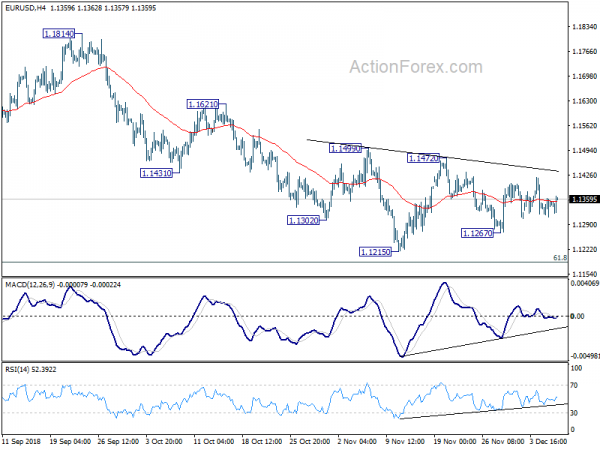

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1317; (P) 1.1339; (R1) 1.1368; More…..

EUR/USD recovers mildly in early US session but it’s bounded in range of 1.1267/1472. Intraday bias remains neutral at this point. As long as 1.1472 resistance holds, deeper decline is expected in the pair. On the downside, break of 1.1267 will target 1.1215 low first. Firm break there will resume larger down trend from 1.2555 for 1.1186 fibonacci level next. However, considering bullish convergence condition in daily MACD, firm break of 1.1472 will be suggest medium term bottoming and turn outlook bullish for 1.1814 resistance instead.

In the bigger picture, as long as 1.1814 resistance holds, down trend down trend from 1.2555 medium term top is still in progress and should target 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. However, break of 1.1814 will confirm completion of such down trend and turn medium term outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Oct | 2.32B | 3.00B | 3.02B | 2.94B |

| 00:30 | AUD | Retail Sales M/M Oct | 0.30% | 0.30% | 0.20% | 0.10% |

| 07:00 | EUR | German Factory Orders M/M Oct | 0.30% | -0.40% | 0.30% | 0.10% |

| 12:30 | USD | Challenger Job Cuts Y/Y Nov | 51.50% | 153.60% | ||

| 13:15 | USD | ADP Employment Change Nov | 179K | 200K | 227K | 225K |

| 13:30 | CAD | International Merchandise Trade (CAD) Oct | -1.2B | -0.7B | -0.4B | -0.9B |

| 13:30 | USD | Trade Balance Oct | -55.5B | -55.2B | -54.0B | -54.6B |

| 13:30 | USD | Initial Jobless Claims (DEC 1) | 231K | 226K | 234K | 235K |

| 13:30 | USD | Non-Farm Productivity | 2.30% | 2.40% | 2.20% | |

| 13:30 | USD | Unit Labor Costs | 0.90% | 1.00% | 1.20% | |

| 14:45 | USD | Services PMI Nov F | 54.4 | 54.4 | ||

| 15:00 | CAD | Ivey PMI Nov | 60.3 | 61.8 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Nov | 59.5 | 60.3 | ||

| 15:00 | USD | Factory Orders Oct | -2.00% | 0.70% | ||

| 16:00 | USD | Crude Oil Inventories | -1.3M | 3.6M |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals