Despite initial setback, US equities extended the post-Christmas historic rebound overnight. DOW ended up 1.14% to 23138.82. S&P 500 rose 0.86% and NASDAQ added 0.38%. But the improvement in sentiments isn’t carried over to Asian session. Nikkei is currently down -0.39%. Hong Hong HSI is just up 0.09% while China Shanghai SSE is up 0.15%. Singapore Strait Times is the better performing one and is up 0.73%. In the currency markets, Dollar is trading as the weakest one for today, followed by Canadian. On the other hand, Yen is so far the strongest one, followed by Swiss Franc. But major pairs and crosses generally held in yesterday’s range.

In the bond markets, despite rebound in stocks, US treasury yields weakened again overnight. 10-year yield closed down -0.054% at 2.743. 30-year yield dropped -0.018 to 3.030 after dipping to 3.003. It’s still stubbornly holding on to 3% handle. Yield curve remains inverted from 1-year (2.602) to 2-year (2.572) and 3-year (2.562). It should also be noted that Japan 10 year JGB yield is also extending recent decline, down -0.0139 at 0.01 for now.

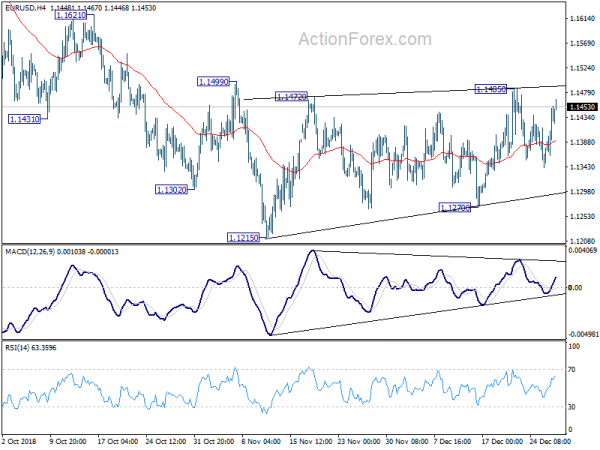

Technically, AUD/USD and USD/CAD extended recent move but are both losing momentum. Dollar might start to top against the two. Also, EUR/USD will possibly challenge 1.1485 resistance today. USD/CHF is pressing 0.9848 key support again. There is prospect of some Dollar weakness before year-end. Yen crosses, including USD/JPY, EUR/JPY and GBP/JPY are staying in consolidation, with EUR/JPY being the stronger one. But recent decline in these Yen crosses are still expected to resume sooner rather than later.

47% Americans blamed Trump for government shutdown

There is no end in sight to the partial US government shutdown as it enters in the the sixth day. Trump continued to blame the Democrats for “OBSTRUCTION of the desperately needed Wall”. White House spokeswoman Sarah Sanders also said yesterday that “the president has made clear that any bill to fund the government must adequately fund border security,” without specially mentioning the border wall.

According to a Reuters/Ipsos poll conducted between Dec 21-26, more Americans blamed Trump for the government shut down. 47% said Trump was responsible, 33% said Congressional Democrats and 8% said Congressional Republicans. Meanwhile, 49% said they opposed to funding for the border wall, and only 36% supported it.

BoJ: Global risks tiled to the downside, uncertainties heightened

As shown in the Summary of Opinions at the December 19/20 meeting, BoJ board members sounded more concerned with global developments. The summary noted that “regarding the outlook for the global economy, risks have been tilted to the downside on the whole amid heightening uncertainties and a prevailing view that such situation will be protracted.”

Specially, it said “looking at the latest data on trade activities in China, both exports and imports marked negative growth on a month-on-month basis, which possibly indicates a deceleration in the Chinese economy”. For Japan, ” it cannot be said that the actual condition of restoration-related demand and production stemming from natural disasters has been strong”. Also, “recovery in exports to China has been weak, and exports as a whole also have shown weak developments.”

BoJ also maintained that “it is necessary to persistently continue with the current powerful monetary easing as the momentum toward 2 percent inflation is maintained.” And it warned that “trying to normalize monetary policy prematurely before achieving the price stability target could adversely strengthen the side effects.” The summary also noted that long-term yield should be allowed to “temporarily turn negative” and “move upward and downward more or less symmetrically from around zero percent”.

On the data front

Japan Tokyo CPI core slowed to 0.9% yoy in December, matched expectations. Unemployment rate rose 0.1% to 2.5% in November. Industrial production dropped -1.1% mom in November versus expectation of -1.6% mom. Retail sales rose 1.4% versus expectation of 2.1%.

Looking ahead, Swiss KOF leading indicator, UK BBA mortgage approvals and Germany CPI flash will be released in European session.

Later in the day, due to partial government shutdown, only Chicago PMI and pending home sales will be release from the US.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1372; (P) 1.1413; (R1) 1.1475; More…..

EUR/USD rebounds to as high as 1.1467 so far today but upside is limited below 1.1485 resistance so far. Intraday bias remains neutral first. On the upside, break of 1.1485 resistance will revive the case of near term reversal, on bullish convergence condition in daily MACD. Bias will be turned back to the upside for 1.1621 resistance first. Break will target 1.1814 key resistance next. On the downside, break of 1.1270 will, instead, revive the bearish case that down trend from 1.2555 is still in progress. Bias will be turned back to the downside for 1.1186 key fibonacci level.

In the bigger picture, as long as 1.1814 resistance holds, down trend down trend from 1.2555 medium term top is still in progress and should target 61.8% retracement of 1.0339 (2017 low) to 1.2555 at 1.1186 next. Sustained break there will pave the way to retest 1.0339. However, break of 1.1814 will confirm completion of such down trend and turn medium term outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Jobless Rate Nov | 2.50% | 2.40% | 2.40% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Dec | 0.90% | 0.90% | 1.00% | |

| 23:50 | JPY | BOJ Summary of Opinions | ||||

| 23:50 | JPY | Industrial Production M/M Nov P | -1.10% | -1.60% | 2.90% | |

| 23:50 | JPY | Retail Trade Y/Y Nov | 1.40% | 2.10% | 3.50% | 3.60% |

| 08:00 | CHF | KOF Leading Indicator Dec | 98.8 | 99.1 | ||

| 09:30 | GBP | BBA Mortgage Approvals Nov | 38.9K | 39.7K | ||

| 13:00 | EUR | German CPI M/M Dec P | 0.30% | 0.10% | ||

| 13:00 | EUR | German CPI Y/Y Dec P | 2.00% | 2.30% | ||

| 14:45 | USD | Chicago PMI Dec | 61.2 | 66.4 | ||

| 15:00 | USD | Pending Home Sales M/M Nov | 1.10% | -2.60% | ||

| 15:30 | USD | Natural Gas Storage | -141B | |||

| 16:00 | USD | Crude Oil Inventories | -0.5M |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals