Yen remains the strongest one for today as the risk aversion dominates the global markets. Major European indices do pare back much of earlier losses. But it’s unsure whether the recovery could sustain. Persistent decline in German 10 year bund yield, which hit the lowest since April 2017, is something for investor to worry about. Also, DOW futures is now down -300 pts, pointing to sharply lower open. More importantly, focus will also be on how much US yield curve would flatten at the long end, and invert from 1-year to 5-year.

Staying in the currency markets, Canadian Dollar is the second strongest, thanks to steadiness in WTI crude oil which stays above 45. Dollar is the third strongest one. Meanwhile, Sterling is reversing Monday’s surprised gain and is trading as the weakest, followed by Australian Dollar and then Euro.

Technically, GBP/JPY’s strong break of 139.29 key support now confirms medium-to-long term bearish reversal. EUR/JPY will be looking at equivalent key support at 124.08. EUR/USD breached 1.1485 resistance briefly earlier today and quickly reversed. Focus will now be on 1.1342 minor support and break will be the first sign of larger decline resumption. With today’s selloff, GBP/USD is eyeing 1.2615 minor support and EUR/GBP is eying 0.9086 resistance.

In Europe, at the time of writing, FTSE s down -0.60%, DAX is down -0.25%, CAC is down -1.34%. German 10 year yield is down -0.0882 at 0.161, lowest since April 2017. Earlier in Asia, Hong Kong HSI dropped -2.77%. China Shanghai SSE dropped -1.15%. Singapore Strait Times dropped -0.97%. Japan was on holiday.

UK PMI manufacturing rose to 54.2, stocks at near record but positive impact likely short-lived

UK PMI manufacturing rose to 54.2 in December, up from 53.1 and beat expectation of 52.6. It’s also the highest level in six months. Markit also noted that “new order and new export order inflows strengthen”, and “stocks of purchases and finished goods rise sharply”.

Rob Dobson, Director at IHS Markit, said in the release that the rise followed “short-term boosts to inventory holdings and inflows of new business as companies stepped up their preparations for a potentially disruptive Brexit.” He added that stocks of purchases and finished goods both rose at near survey-record rates, but “any positive impact on the PMI is likely to be short-lived”. Also, manufacturing will be entering 2019 “on a less than ideal footing with Brexit uncertainty having intensified considerably.”

Eurozone PMI manufacturing finalized at 51.4, manufacturing boom faded away to near stagnation

Eurozone PMI manufacturing was finalized at 51.4 in December, unrevised. It’s down from November’s 51.8 and hit the lowest since February 2016. Markit also noted that “fall in new work signalled for third month running” and “confidence about the future hits fresh six-year low”. Among the countries, Germany hit 33-month low at 51.5. Spain hit 28-month low at 51.5. France hit 27-month low at 49.7, in contraction. Italy, despite recovering to 2-month high at 49.2, remained in contraction.

Chris Williamson, Chief Business Economist at IHS Markit noted in the release that “a disappointing December rounds off a year in which a manufacturing boom faded away to near stagnation.” And, “the last three months of 2018 saw manufacturers report the worst quarterly performance in terms of production since the second quarter of 2013.” Also, “the undercurrent of weak demand and growing risk aversion evident across the surveys suggests that any rebound could prove modest at best, with Brexit representing a particularly worrying unknown for the outlook.”

China Caixin PMI manufacturing in first contraction since 2017, greater downward pressure ahead

The Caixin China PMI manufacturing dropped to 49.7 in December, down from 50.2 and missed expectation of 50.3. That’s also the first contractionary reading since May 2017. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group, noted in the release that “external demand remained subdued due to the trade frictions between China and the U.S., while domestic demand weakened more notably”. And, “it is looking increasingly likely that the Chinese economy may come under greater downward pressure.”

In our view, the latest PMI data added further evidence that China’s economy is in bad shape. Trade war with the US has not only weakened trade, but also domestic demand. The job market has also deteriorated, suggesting further stimulus is needed to be in place as soon as possible. We expect the central bank to accelerate monetary easing. While further reduction in required reserve ratio is widely expected, we believe PBOC could also reduce the policy rate to support the economy. The government’s fiscal policy would be increasingly accommodative, in the form of increasing spending on infrastructure and cutting taxes. More in China’s PMIs Confirmed Manufacturing Sector in Contraction.

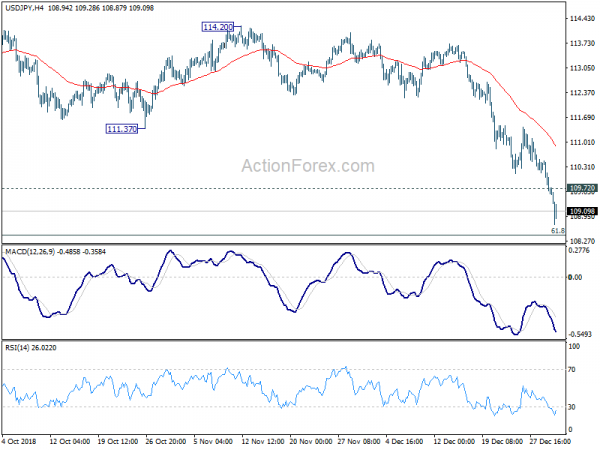

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.53; (P) 109.73; (R1) 109.93; More..

USD/JPY drops to as low as 108.70 so far today and intraday bias remains on the downside. Current fall from 114.54 should target 61.8% retracement of 104.62 to 114.54 at 118.40 first. Sustained break there will pave the way to retest 114.54 low next. On the upside, above 109.20 minor resistance will turn intraday bias neutral to bring consolidation. But upside of recovery should be limited by 111.37 support turned resistance to bring fall resumption.

In the bigger picture, price actions from 125.85 (2015 high) are seen as a long term corrective pattern, no change in this view. Apparently, such corrective pattern is not completed yet. Fall from 114.54 is seen as another medium term down leg, 98.97/104.62 support zone. For now, we’d expect strong support from there to contain downside to bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 1:45 | CNY | Caixin PMI Manufacturing Dec | 49.7 | 50.3 | 50.2 | |

| 8:45 | EUR | Italy Manufacturing PMI Dec | 49.2 | 48.4 | 48.6 | |

| 8:50 | EUR | France Manufacturing PMI Dec F | 49.7 | 49.7 | 49.7 | |

| 8:55 | EUR | Germany Manufacturing PMI Dec F | 51.5 | 51.5 | 51.5 | |

| 9:00 | EUR | Eurozone Manufacturing PMI Dec F | 51.4 | 51.4 | 51.4 | |

| 9:30 | GBP | PMI Manufacturing Dec | 54.2 | 52.6 | 53.1 | 53.6 |

| 14:30 | CAD | Manufacturing PMI Dec | 54.9 | |||

| 14:45 | USD | Manufacturing PMI Dec F | 53.9 | 53.9 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals