Sterling rises broadly today and takes out key resistance against Dollar and Euro. UK has moved a big step in avoiding no-deal Brexit. Prime Minister Theresa May announced to hold three separate votes on Brexit deal, no-deal Brexit and delay. The key is, no-deal Brexit is no longer the default position on March 29. But it could only happen with explicit consent of the Parliament.

Staying in the currency markets, Yen follows as the second strongest and stock markets pare back trade optimism triggered gains. Commodity currencies are trading generally lower, as led by Australian Dollar. But Canadian Dollar is not far behind despite slight recovery in oil price. Dollar is mixed, awaiting Fed chair Jerome Powell’s testimony.

Technically, GBP/USD breaks 1.3173/3217 key resistance zone. A head and should bottom would be formed if GBP/USD can sustain above this zone, which confirms medium term bullish reversal. . EUR/GBP also broke key support level at 0.8617/20, resuming medium term decline for 0.8416 projection level. GBP/JPY is pressing medium term trend line. Sustained break will pave the way back to 150.

In Europe, currently, FTSE is down -0.76%, DAX is down -0.13%, CAC is down -0.15%. German 10-year yield is down -0.007 at 0.112. Earlier in Asia, Nikkei dropped -0.37%. Hong Kong HSI dropped -0.65%. China Shanghai SSE dropped -0.67%. Singapore Strait Times dropped -0.33%. Japan 10-year JGB yield rose 0.0089 to -0.027.

UK PM May: There’ll be a second vote on Brexit deal, a vote on no-deal, then a vote on extension

UK Prime Minister Theresa May announced today three additional commitments in the parliament regarding Brexit. Firstly, there will be a second meaningful vote on the withdrawal agreement by March 12. Secondly, If the government loses the meaningful vote, on March 13, there will be a vote on whether to leave without a deal. And UK will only leave EU on March 29 without a deal, with explicit consent of the House.

Then, if both the withdrawal agreement and no-deal Brexit are voted down, there will be another vote on a short, limited extension to Article 50 on March 14. If the parliament passes the motion, the government will seek to get that extension. Though, May insisted that she doesn’t not want to see Article 50 extension, and the focus is still on leaving on March 29.

BoE Carney: Short-term data volatility less of a signal about medium-term outlook

In the annual report to the Treasury Select Committee, BoE Governor Mark Carney said UK growth “slowed sharply in late 2018 and appears to have remained weak in early 2019”. The slowdown reflects both “softer activity abroad” and “greater effects from Brexit uncertainties”. Brexit uncertainties is “creating a series of tensions for business, households and in financial markets”. But that will only cause “short-term volatility in the economic data” and provide “less of a signal about the medium-term outlook”.

Carney added that the ” fundamentals of the UK economy are sound. The financial sector is resilient. Corporate balance sheets are strong. And the labour market is tight.” If the economic conditions evolve in line with BoE projections, which are conditioned on a smooth Brexit, “limited and gradual rate rises are likely to be needed to return inflation sustainably to target.”

BoE Vlieghe: Easing or extended pause in monetary policy more likely in case of no-deal Brexit

BoE MPC external member Gertjan Vlieghe reiterate his view that in case of no-deal Brexit, not all paths are equally likely. He said that “in the case of a no-deal scenario I judge that an easing or an extended pause in monetary policy is more likely to be the appropriate policy response than a tightening.”

Also, BoE “will have to judge in real time how well inflation expectations remain anchored, and how households and businesses are reacting to the disruptions.” And “even if the direction and scale of monetary policy changes are unknown beforehand, monetary policy will do what it needs to do to bring inflation back to target within a horizon that is consistent with our mandate.”

German GfK: Economic expectations continued steep downward spiral

Germany GfK consumer confidence for February was unchanged at 10.8. GfK noted that “mood of consumers paints a mixed picture. Income expectations remain stable. But propensity to buy lost ground again. Economic expectations continued their “steep downward spiral”. Economic expectation dropped -6.5 pts to 4.2. That’s the fifth decline in a row and the lowest reading since March 2016. Gfk said “Consumers feel that the risk of the German economy slipping into recession again has tangibly increased in recent weeks”. A technical recession was only “narrowly avoided” last year, with 0% growth in Q4.

And, “external factors are primarily responsible for the lack of momentum in the German economy.”. Gfk cited trade dispute between Europe, China and US is “causing growing uncertainty among consumers”. And, they ” worry that Germany, as a strongly export-oriented economy, would suffer negative consequences if this dispute led to trade barriers such as rising customs tariffs.” How and when Brexit will take place is far from certain and “This makes planning more difficult for companies on all sides.

BoJ Kuroda: Chinese economy to remain in doldrums in first half

BoJ Governor Haruhiko Kuroda told the parliament that China’s economy “slowed quite significantly in the latter half of last year”. And he predicts that it may “remain in the doldrums in the first half of this year.” Nevertheless, Kuroda expects Chinese even economy to “pick up thereafter, as authorities have taken fiscal and monetary stimulative action.”

Domestically, Kuroda expected that the net burden on households from this year’s scheduled sales tax hike to be smaller than previous hike in 2014. And he added that BOJ will be watching the impact of the sales tax hike on the economy. The impact could change depending on consumer sentiment, job and income conditions at that time.

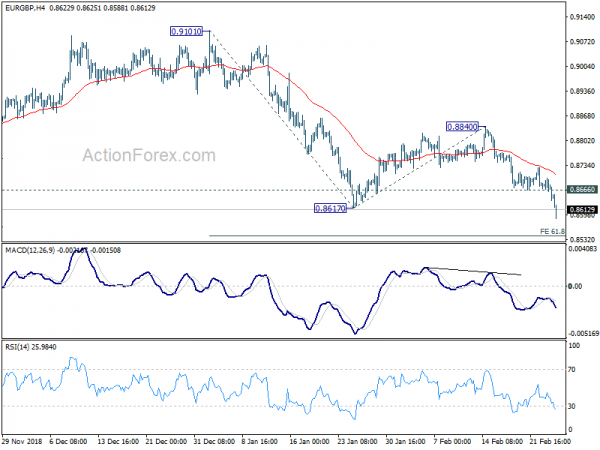

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8657; (P) 0.8679; (R1) 0.8696; More…

EUR/GBP drops sharply to as low as 0.8588 so far today. The break of 0.8617/20 key support zone suggests resumption of larger decline from 0.9305. Intraday bias stays on the downside. Next target will be 61.8% projection of 0.9101 to 0.8617 from 0.8840 at 0.8541. On the upside, break of 0.8666 minor resistance will turn intraday bias neutral first. But recovery should be limited well below 0.8840 resistance to bring another decline.

In the bigger picture, EUR/GBP is seen as staying in long term range pattern started at 0.9304 (2016 high). On the downside, decisive break of 0.8620 support will resume the falling leg from 0.9305 (2017 high) to 100% projection of 0.9305 to 0.8620 from 0.9101 at 0.8416. In that case, we’d expect strong support around 0.8312 to contain downside and bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 7:00 | EUR | German GfK Consumer Confidence Mar | 10.8 | 10.8 | 10.8 | |

| 10:00 | GBP | BoE Inflation Report Hearings | ||||

| 13:30 | USD | Housing Starts Dec | 1.25M | 1.26M | ||

| 13:30 | USD | Building Permits Dec | 1.29M | 1.32M | ||

| 14:00 | USD | House Price Index M/M Dec | 0.40% | 0.40% | ||

| 14:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Dec | 4.90% | 4.70% | ||

| 15:00 | USD | Consumer Confidence Feb | 124.1 | 120.2 | ||

| 15:00 | USD | Fed Powell testifies Before Senate Banking Panel |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals