Sterling reverses and dives sharply as Brexit turns into a mess again. The new assurances UK Prime Minister Theresa May got from EU provided some nervous hope earlier today. But legal advice from Attorney General Geoffrey Cox killed the chance of getting the Brexit deal through the meaningful vote today. Basically, the updated deal just reduces risks of being tied in the Irish backstop forever. But such risk is not eliminated.

Pound is now trading as the weakest one for today, despite strong January GDP data. Canadian Dollar follows as the second weakest. Dollar got not support from CPI inflation data, which slowed in February. The greenback is the third weakest. On the other hand, New Zealand Dollar is the weakest one, followed by Euro, and then Swiss Franc.

In other markets, FTSE is currently up 0.19%. CAC is down -0.14%. DAX is down -0.19%. German 10-year bund yield is up 0.002 at 0.063. Earlier in Asia, Nikkei rose 1.79%. China Shanghai SSE rose 1.10%. Hong Kong HSI rose 1.46%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield rose 0.003 to -0.032.

Just released, US headline CPI slowed to 1.5% yoy in February, down from 1.6% yoy and missed expectation of 1.6% yoy. Core CPI also slowed to 2.1% yoy, down from 2.2% yoy and missed expectation of 2.2%. yoy.

Attorney General Cox said risk of indefinite Irish backstop reduced, not eliminated

Sterling is knocked down sharply after UK Attorney General Geoffrey Cox published his updated legal advice up the new Brexit deal agreed by UK Prime Minister Theresa May and European Commission President Jean-Claude Juncker late Monday. In short, Cox said that he new documents “reduce the risk” the UK is trapped indefinitely in the Northern Ireland backstop. But such risk is not eliminated.

And most importantly, as Cox’s letter concluded: “the legal risk remains unchanged that if through no such demonstrable failure to either party, but simply because of intractable differences, that situation does arise, the United Kingdom would have, at least while the fundamental circumstances remained the same, no internationally lawful means of exiting the Protocol’s arrangements, save by agreement”.

In the Parliament, Cox said “the question for the house is whether, in the light of these improvements, as a political judgment, the house should now enter in to those arrangements” He added that his legal advice could only inform “what is essentially a political decision that each of us must make.”

May got new joint legally binding instrument and joint statement from EU Juncker

May got “legally binding” changes to the Brexit deal after meeting with Juncker in the European Parliament in Strasbourg, France late Monday. Two important agreements were agreed that could “strengthen and improve” both the withdrawal agrement. The most important one is a “joint legally binding instrument.” May believed it could be used to start a “formal dispute” against EU if it tried to keep UK into the backstop indefinitely. And under ruling of an arbitration panel, UK would have “the right to enact a unilateral, proportionate suspension of its obligations under the Withdrawal Agreement”

Secondly, there is another “joint statement” adding to the political declaration. A specific negotiating track would be established given both sides’ to work “at speed” on an agreement by end of 2020 to avoid triggering the Irish backstop. Thirdly, May will put forward a “unilateral declaration” to outline the UK’s position that there was nothing to prevent it from leaving the backstop arrangement if discussions on a future relationship with the EU break down and there is no prospect on an agreement.

UK GDP grew 0.5% mom in Jan, productions beat expectations

UK GDP grew strongly by 0.5% in January, well above expectation of 0.2% mom. Services rose 0.3%, production rose 0.6%, manufacturing rose 0.8% and construction jumped 2.8%. Though, agriculture dropped -1.3%. Rolling three-month growth was unchanged at 0.2% qoq.

ONS Head of GDP Rob Kent-Smith said: “Across the latest three months, growth remained weak with falls in manufacture of metal products, cars and construction repair work all dampening economic growth. These were offset by strong performances in wholesale, IT and health services. This sluggish growth came despite the economy bouncing back from a weak December.”

Also from UK, visible trade deficit widened to GBP -13.1B in January. Industrial production rose 0.6% mom, -0.9% yoy versus expectation of 0.2% mom, -1.3% yoy. Manufacturing production rose 0.8% mom, -1.1% yoy versus expectation o f0.2% mom, -1.9% yoy.

BoJ Amamiya: No debate on exit until price target in sight

BoJ Deputy Governor Masayoshi Amamiya reiterated to the parliament that the priority for the central bank is to achieve the 2% inflation target. He noted that it’s also “important and necessary for the BOJ to communicate to markets its strategy for exiting ultra-loose monetary policy”. However, “debate on an exit must begin only when achievement of our price target comes into sight.”

On the other hand, Finance Minister Taro Aso told the parliament that “I don’t think anyone in the general public is angry about the fact that inflation hasn’t reached 2 percent. And, BoJ “could be a bit more flexible: on the inflation target too.

Release from Japan, BSI large manufacturing index dropped to -7.3 in Q1.

Australia business conditions and confidence dropped, home loans contracted further

Australia NAB Business Conditions dropped to 4 in February, down from 7 and missed expectation of 5. Business Confidence dropped to 2, down from 4 and missed expectation of 3. Alan Oster, NAB Group Chief Economist said “conditions declined in February to below average levels – with profitability and trading now below average.” Employment index “remained resilient” but that is “likely reflecting that labour demand decisions typically lag economic activity.”

Forward looking indicates point to an “ongoing weakness in business conditions” And, “this may have important implications for both future investment and employment decisions of business.” The survey suggests “little improvement” in Q1 and “some further growing risks to our outlook for business investment in 2019”.

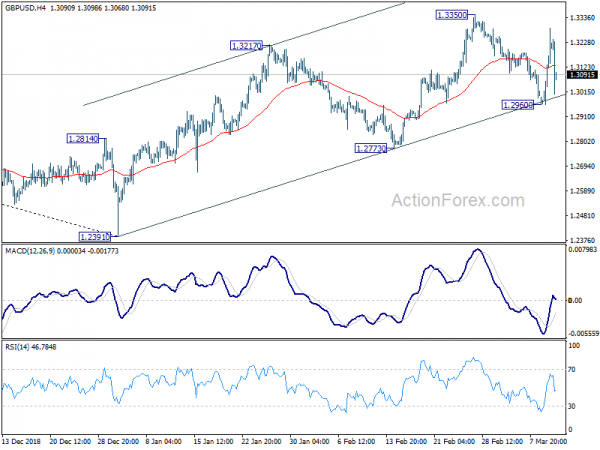

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3016; (P) 1.3094; (R1) 1.3227; More….

GBP/USD failed to break through 1.3350 resistance despite today’s strong rebound. Intraday bias is turned neutral with subsequent steep retreat. On the upside, Break of 1.3350 will resume the rebound from 1.2391 low to 61.8% retracement of 1.4376 to 1.2391 at 1.3618 next. On the downside, again, sustained break of trend line support will argue that rebound from 1.2391 has completed earlier than expected at 1.3350. Deeper fall would then be seen to 1.2773 support for confirmation.

In the bigger picture, medium term decline from 1.4376 (2018 high) should have completed at 1.2391. Rise from 1.2391 is now seen as the third leg of the corrective pattern from 1.1946 (2016 low). Further rise could be seen through 1.4376 in medium term. On the downside, though, break of 1.2773 support will dampen this view. Focus will be turned back to 1.2391 low and break will resume the fall from 1.4376 to 1.1946.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BSI Large Manufacturing Q/Q Q1 | -7.3 | 4.8 | 5.5 | |

| 00:30 | AUD | NAB Business Conditions Feb | 4 | 5 | 7 | |

| 00:30 | AUD | NAB Business Confidence Feb | 2 | 3 | 4 | |

| 00:30 | AUD | Home Loans M/M Jan | -2.60% | -2.00% | -8.20% | |

| 09:30 | GBP | GDP M/M Jan | 0.50% | 0.20% | -0.40% | |

| 09:30 | GBP | Index of Services 3M/3M Jan | 0.50% | 0.50% | 0.40% | |

| 09:30 | GBP | Visible Trade Balance (GBP) Jan | -13.1B | -12.11B | -12.10B | |

| 09:30 | GBP | Industrial Production M/M Jan | 0.60% | 0.20% | -0.50% | |

| 09:30 | GBP | Industrial Production Y/Y Jan | -0.90% | -1.30% | -0.90% | |

| 09:30 | GBP | Manufacturing Production M/M Jan | 0.80% | 0.20% | -0.70% | |

| 09:30 | GBP | Manufacturing Production Y/Y Jan | -1.10% | -1.90% | -2.10% | |

| 09:30 | GBP | Construction Output M/M Jan | 2.80% | 0.80% | -2.80% | |

| 12:30 | USD | CPI M/M Feb | 0.20% | 0.20% | 0.00% | |

| 12:30 | USD | CPI Y/Y Feb | 1.50% | 1.60% | 1.60% | |

| 12:30 | USD | CPI Core M/M Feb | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | CPI Core Y/Y Feb | 2.10% | 2.20% | 2.20% |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals