Strong rally in Chinese stocks is lifting Asian markets broadly higher today. Chinese president Xi Jinping is set to visit Italy, France and Monaco from March 21 to 26 this week. While there’s no detail on the visits yet, it’s believed that there could be signing of an agreement for Italy to join the Belt and Road infrastructure investment initiative. But while that might lift sentiments, the could look is still clouded by uncertainty in trade negotiations with the US. The highly anticipated Trump-Xi summit might only happen in April at the earliest, or in June alongside G20 summit in Japan, or might not happen at all.

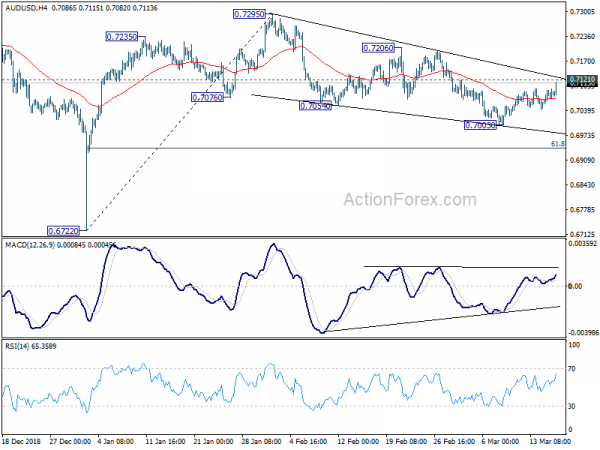

Nevertheless, the currency markets are following strong risk appetite with Australian Dollar leading other commodity currencies higher. Yen and Dollar are the weakest ones. Sterling is also sluggish ahead of another meaning vote on Brexit deal, most likely on Tuesday. Technically, an immediate focus is 0.7121 minor resistance in AUD/USD. Break will suggest that recent decline from 0.7295 has completed and further rise would likely be seen back to 0.7206 resistance at least.

In other markets, Nikkei is currently up 0.67%. Hong Kong HSI is up 0.73%. China Shanghai SSE is up 1.26%. Singapore Strait Times is up 0.41%. Japan 10-year JGB yield is down -0.0037 at 0.039.

UK Hammond: Significant number of colleagues changed minds and backed the Brexit deal

The UK Parliament will have meaningful vote on Prime Minister Theresa May’s Brexit deal for the third time this week. Ahead of that Chancellor of Exchequer Philip Hammond said a significant number of Conservatives have changed their mind last week to back the plan. And he expected more to come even though the government hasn’t had enough numbers yet. And, “it is a work in progress”.

Hammond said “What has happened since last Tuesday is that a significant number of colleagues, including some very prominent ones who have gone public, have changed their view on this and decided that the alternatives are so unpalatable to them that they on reflection think the prime minister’s deal is the best way to deliver Brexit,”

Last Tuesday, the Commons voted 391-242 to reject May’s “improved” deal. Back in January, the deal was voted down by 432-202.

BCC downgrades UK growth forecasts on Brexit and global slowdown

The British Chambers of Commerce (BCC) has downgraded UK growth forecast on “weaker outlook for business investment and trade amid continued Brexit uncertainty and slower expected global economic growth”. For 2019, growth forecast was downgraded from 1.3% to 1.2%. For 2020, growth forecasts was downgraded from 1.5% to 1.3%. in 2021, growth is projected to pick up slightly to 1.4%.

Also, BCC noted that business investment is projected to contract by -1.0% in 2019. And that would be the weakest outturn in a decade since the financial crisis in 2009. BCC blamed that “ongoing uncertainty over the UK’s future relationship with the EU is expected to continue to weigh on investment intentions.” And, “diversion of resources to prepare for no deal and the high upfront cost of doing business in the UK is also projected to limit the extent to which investment activity will bounce back over the near term.”

Looking ahead, three central banks to meet, two to release minutes

Three central banks will meet this week, including Fed, SNB and BoE. BoJ and RBA will release meeting minutes too. Fed is expected to keep federal funds rate unchanged at 2.25-2.50%. “Patience” will remain the central tone of the statement and other communications. Fed might also announce the plan to end the balance sheet roll-off and that could catch some attentions. But main focus will be on the new economic projections. Since late December, Fed officials have sung a chorus indicating they’re in no hurry to lift interest rates unchanged. They finally have a chance to tell the markets the reasons for the change in stance with concrete numbers.

SNB is expected to keep the sight deposit rate at -0.75%. The three-month Libor target range should be held at -1.25% to -0.25% too. The central bank should also maintain that it’s necessary to keep interest rate negative and pledge to intervene in the forex markets when needed. Such measures will keep the attractiveness of Swiss franc investments low and reduce upward pressure on the currency.

BoE is also expected to keep bank rate unchanged at 0.75%. The asset purchase target should be held at GBP 435B. BoE will also reiterate that the economic outlook will depend significantly on the nature of Brexit, hard or soft, abrupt or smooth. Also, it will be reiterated that the monetary path following Brexit will not be automatic and could be in either direction.

In addition to central bank activities, there are a number of economic data to watch too. Eurozone PMIs will give some hints on whether the slowdown in Eurozone has past its worst. UK CPI will also be watched but it’s likely to be overshadowed by Brexit vote and BoE. Downward surprises in Australian house price and job data will add to the case of two RBA rate cut this year. Canada CPI and retails sales could also be market moving.

- Monday: Japan trade balance; Eurozone trade balance; Canada foreign securities purchases; US NAHB housing index

- Tuesday: RBA minutes, Australia house price index; Swiss trade balance; UK employment; German ZEW; US factory orders

- Wednesday: BoJ minutes; German PPI; UK CPI, PPI, CBI orders; FOMC rate decision

- Thursday: New Zealand GDP; Australia employment; SNB rate decision; BoE rate decision; Canada wholesale sales; US Philly Fed survey, jobless claims

- Friday: Japan PMI manufacturing, national CPI core; Eurozone PMIs, current account; Canada CPI, retail sales; US PMIs, existing home sales, wholesale inventories

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7066; (P) 0.7082; (R1) 0.7102; More…

AUD/USD rises strongly today and focus is now on 0.7121 minor resistance. Firm break there will argue that decline from 0.7295 has completed at 0.7003. In that case, further rise should be seen to 0.7206 resistance to confirm. More importantly, in that case, corrective three wave structure of the fall fro 0.7296 to 0.7003 would suggest that rise from 0.6722 low is extending through 0.7295. On the downside, though, break of 0.7003 will extend the fall from 0.7295 to 61.8% retracement of 0.6722 to 0.7295 at 0.6941 and below.

In the bigger picture, as long as 0.7393 resistance holds, we’d treat fall from 0.8135 as resuming long term down trend from 1.1079 (2011 high). Decisive break of 0.6826 (2016 low) will confirm this bearish view and resume the down trend to 0.6008 (2008 low). However, firm break of 0.7393 will argue that fall from 0.8135 has completed. And corrective pattern from 0.6826 has started the third leg, targeting 0.8135 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance (JPY) Feb | 0.12T | 0.09T | -0.37T | -0.29T |

| 0:01 | GBP | Rightmove House Prices M/M Mar | 0.40% | 0.70% | ||

| 4:30 | JPY | Industrial Production M/M Jan F | -3.40% | -3.70% | -3.70% | |

| 10:00 | EUR | Eurozone Trade Balance (EUR) Jan | 17.2B | 15.6B | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jan | -18.96B | |||

| 14:00 | USD | NAHB Housing Market Index Mar | 63 | 62 |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals