The forex markets are relatively quiet as quarter end approaches. Sterling remains stuck in range as Brexit stalemate continues. The UK Parliament continued to tell the world what they don’t want regarding Brexit, but not they really want. Meanwhile, US-China trade talks are resuming in Beijing today. There are reports of unprecedented progress in the negotiations. Yet it remains uncertain when the deal would be reached, or whether it could be. Treasury yields extended recent decline with US 10-year yield firmly taken out 2.4 handle overnight. US yield curve inversion continue to worsen but there is no clear responses from the stock markets yet.

Technically, Euro will be an interest currency to watch today. Other than New Zealand Dollar, Euro’s weakness is most apparent. Recession worries, falling treasury yields and Brexit stalemate are all playing a part. EUR/CHF is now pressing key support level 2018 low at 1.1173 after recent extended decline. Decisive break there will resume larger down trend from 1.2004. EUR/JPY is pressing 123.82 minor support. Break will resume the fall from 127.50 and solidify near bearish reversal for 118.62 low. EUR/GBP recovered just ahead of 0.8474 support but looks vulnerable to break to resume medium term down trend. EUR/USD’s fall from 1.1448 is also in progress for 1.1176 low.

In Asia, Nikkei is currently down -1.37%. Hong Kong HSI is up 0.03%. China Shanghai SSE is down -0.26%. Singapore Strait Times is up 0.24%. Japan 10-year JGB yield is down -0.016 at -0.082. Overnight, DOW dropped -0.13%. S&P 500 dropped -0.46%. NASDAQ dropped -0.63%. 10-year yield dropped -0.040 to 2.374.

All Brexit alternatives voted down while May gains support for her deal

The UK Parliaments once again expressed what they don’t want about Brexit, without saying what they want. With April 12 cliff-edge looming, there is still no sign of a breakthrough.

All eight Brexit alternatives were defeated in the UK House of Commons on Wednesday. That means no majority emerged support any options including no deal, a referendum, a customs union and a Norway-style deal. The closet results was for a “permanent and comprehensive UK-wide customs union with the EU”, which was voted down by 264 to 272. The call for confirmatory referendum was voted down by 268 to 295.

Meanwhile, Prime Minister Theresa May offered to resign if her Brexit deal gets approved by the parliament in a third meaningful vote. She told the Conservative 1922 Committee that “I know there is a desire for a new approach – and new leadership – in the second phase of the Brexit negotiations, and I won’t stand in the way of that.” She added “I am prepared to leave this job earlier than I intended in order to do what is right for our country and our party.”

With May’s offer, more hard-line Brexiteers turned to support her deal. A key consideration is that the change in leadership for the most important of next phase in negotiations. Trade negotiations and futures relationship will be on the line, which Brexiteers would be eager to get a firmer control on. However, it remains uncertain how May could get enough votes as Northern Ireland’s DUP repeated its objection to the deal.

Fed George: More time and evidence needed to separate signal from noise

Kansas City Fed President Esther George said in a speech that weakness in Q1 growth could reflect “transitory factors” such as the government shutdown, financial volatility, an unusually harsh winter, and heightened policy uncertainty. But over the medium term, the “generally positive outlook” of the US economy has “several prominent downside risks”.

The biggest risks come from slower growth abroad, “particularly in China, the euro area, and the United Kingdom.” Together with waning fiscal and monetary stimulus, they “represent a stronger headwind” then George’s baseline forecast. Right now, she noted that “data are noisy” and more time and evidence are needed to “separate the signal from the noise”.

Unprecedented progress made on forced technology transfer as new round of US-China trade talks start

US Trade Representative Robert Lighthizer and Treasury Secretary Steven Mnuchin arrive in Beijing today for a new round of trade negotiations Ahead of that Reuters reported that there were unprecedented progress on a core issue in technology transfers.

Citing unnamed officials, it’s said that China’s proposals went further than in the past, which created hope for an eventual trade deal. The discussions on forced technology transfer covered areas that were not touched before, in terms of both scope and specifics.

Meanwhile, the texts of agreements moved forward in all areas even though they’re not where the US want to be. The areas are believed to include forced technology transfer and cyber theft, intellectual property rights, services, currency, agriculture and non-tariff barriers to trade.

Another official noted that some of the tariffs imposed since last year will stay even after a deal is made. And this will be an important issue to resolve, as an important part of the final deal. But for now, there is no clear timeline for completing the deal yet. And negotiations could drag on till June.

New Zealand ANZ business confidence dropped, RBNZ cut sooner rather than later

New Zealand ANZ Business Confidence dropped to -38 in March, down from -30.9. Activity Outlook also dropped to 6.3, down from 10.5. ANZ noted that GDP growth has moderated but is still respectable. However, leading indicators are suggesting that the economy is “running out of steam quite rapidly”.

In particular, export intentions dropped to levels lower than during the Asian Financial Crisis of 1998-9 and the Global Financial Crisis of 2008-9. Sharply lower export intentions despite a well-behaved exchange rate suggest global factors are a part of slowdown in momentum.

Overall, ANZ expects next move in RBNZ to be a cut, “with a growing risk that it is sooner rather than later.”

Looking ahead

Eurozone will release M3 money supply and confidence indicators. Germany will release March CPI flash. US will release Q4 GDP final, jobless claims and pending home sales.

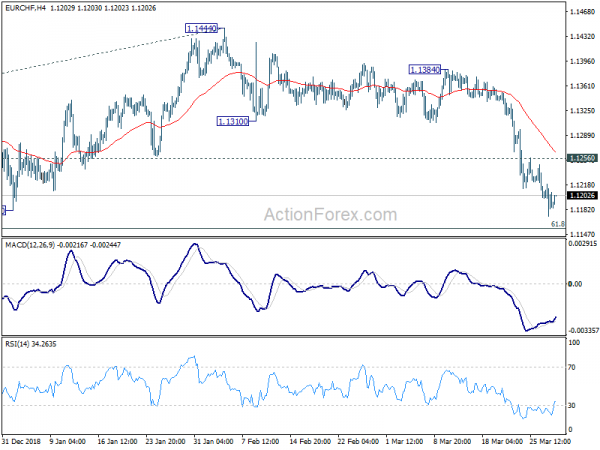

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1166; (P) 1.1194; (R1) 1.1214; More…

EUR/CHF drops to as low as 1.1173 so far and intraday bias remains on the downside. Decisive break of 1.1173 low (inside 1.1154/98 key support zone) will carry larger bearish implication and could trigger downside acceleration. Next downside target will be 61.8% projection of 1.2004 to 1.1173 from 1.1444 at 1.0930. On the upside, though, break of 1.1256 minor resistance will turn bias back to the upside for recovery to 1.1310 support turned resistance.

In the bigger picture, multiple rejection by 55 week EMA indicates medium term bearishness. Focus remains on 1.1154/98 support zone (2016 high and 61.8% retracement of 1.0629 to 1.2004 at 1.1154). Decisive break there will confirm resumption of whole down trend from 1.2004 and long term bearish reversal. EUR/CHF should then target 1.0629 support and below. This will now remain the favored case as long as 1.1444 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | NZD | ANZ Business Confidence Mar | -38 | -30.9 | ||

| 9:00 | EUR | Eurozone M3 Money Supply Y/Y Feb | 3.90% | 3.80% | ||

| 10:00 | EUR | Eurozone Business Climate Indicator Mar | 0.69 | 0.69 | ||

| 10:00 | EUR | Eurozone Economic Confidence Mar | 105.9 | 106.1 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Mar | -0.5 | -0.4 | ||

| 10:00 | EUR | Eurozone Services Confidence Mar | 12 | 12.1 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Mar F | -7.2 | -7.2 | ||

| 12:30 | USD | GDP Annualized Q4 F | 2.40% | 2.60% | ||

| 12:30 | USD | GDP Price Index Q4 F | 1.80% | 1.80% | ||

| 12:30 | USD | Initial Jobless Claims (MAR 23) | 220K | 221K | ||

| 13:00 | EUR | German CPI M/M Mar P | 0.60% | 0.40% | ||

| 13:00 | EUR | German CPI Y/Y Mar P | 1.50% | 1.50% | ||

| 14:00 | USD | Pending Home Sales M/M Feb | 0.00% | 4.60% | ||

| 14:30 | USD | Natural Gas Storage | -47B |

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals