Central bank policy meetings in Australia and New Zealand will be the main focus next week with investors anticipating a further dovish tilt. Out of all the central banks that have turned dovish this year, the Reserve Bank of New Zealand is the most likely to cut rates and analysts are predicting a move as early as next week. In terms of economic indicators, UK growth figures for the first quarter will be the most important release followed by US inflation, Canadian employment and Chinese trade numbers.

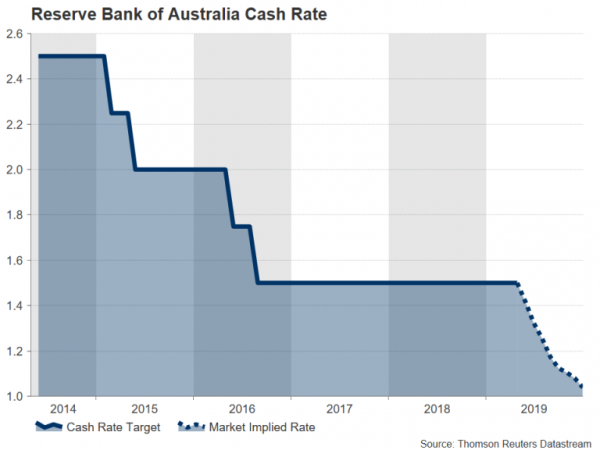

RBA meets; is a rate cut getting closer?

The Reserve Bank of Australia reluctantly dropped its tightening bias earlier this year and gave its clearest signal at the April policy meeting that a rate cut would be on the cards if inflation declines and unemployment picks up. The latest data on prices and the labour market have been mixed; inflation fell more than expected in the first quarter, but employment rose sharply in March.

However, markets clearly think the weakening inflation picture will be significant enough to force the RBA to slash rates over the coming months even if employment continues to rise at healthy levels. Interest rate futures imply a full 25 basis point rate reduction by July.

The Australian dollar has slipped in line with the market’s pricing of a rate cut and broke below the $70 level this week. These losses, however, make the aussie more susceptible to upside shocks should the RBA refrain from providing more explicit signals of a rate cut when it announces its latest policy decision on Tuesday. It’s more than possible the RBA will still not want to commit to lowering rates just yet, which would disappoint the aussie bears.

Meanwhile, March stats on retail sales and the trade balance will also be watched on Tuesday, a few hours before the RBA’s decision.

RBNZ could deliver first rate cut in 2½ years

Unlike the RBA, the Reserve Bank of New Zealand hasn’t been as hesitant in shifting to a dovish stance and flagged a rate cut at its last meeting in March. With both the latest CPI and jobs reports out of New Zealand coming in below expectations, there’s a high probability the RBNZ will lower its official cash rate by 25 bps to 1.50% on Wednesday. The RBNZ has a dual mandate of targeting both inflation and employment so weakness in both indicators would justify looser monetary policy.

With markets betting just under a 60% chance of a rate reduction next week, the New Zealand dollar has room to slide further, especially if any cut is accompanied by a dovish statement.

China to publish export data as trade talks enter endgame

Exports from China are expected to have moderated in April after surging by 14.2% in March. They are forecast to have risen by 2.3% year-on-year, though imports probably shrank again, falling by 3.6% according to consensus forecasts. The data is due on Wednesday and will be followed on Thursday by the consumer and producer price indices for April.

Better-than-expected numbers from China would be positive for risk sentiment, which has been somewhat subdued lately. But a bigger boost to risk appetite could come from the conclusion of trade talks between the United States and China, ending a year-long trade dispute that has seen tariffs between the two nations go up. There have been some reports this week hinting that a deal could be achievable by the end of next week.

Japan’s markets to reopen after long Golden Week break

Japanese traders will return to their desks after a 10-day holiday to celebrate the new Emperor’s ascension to the throne. However, the Japanese calendar is unlikely to create much excitement with only the Bank of Japan’s Summary of Opinions of the April meeting on Wednesday and household spending and pay growth numbers on Friday to look forward to. Household spending is forecast to have increased by 0.5% month-on-month in March, keeping the annual rate unchanged at 1.7%. Next month’s figures will be more interesting to watch as it’s hoped consumption would have been boosted by the extended Golden Week holiday.

For the coming week, however, there will be little out of Japan to move the yen, and so market sentiment will be the dominant driver of the safe-haven currency.

Quiet week for the Eurozone

There was some rare good news for the Eurozone economy this week after first quarter GDP beat expectations to grow by 0.4% over the quarter. The data gave the euro a modest lift, with many traders still cautious about the Eurozone’s growth prospects. German numbers due on Tuesday could reaffirm the need for caution. Industrial orders are expected to have rebounded by 0.8% m/m in March, following two months of sharp declines, but industrial production is forecast to have dropped by 0.7% m/m during the same period, reversing the prior month’s 0.7% gain.

For the euro area as a whole, the sentix index for May and retail sales for March could attract some attention on Monday. The European Central Bank’s minutes of the April policy meeting are unlikely to generate much reaction either on Wednesday. Given that policymakers did not discuss introducing a tiered system for the deposit rate and there were no new economic projections available, the minutes are anticipated to produce few surprises.

Norges Bank to hold rates

Much to the ECB’s envy, one central bank that has been in a position to raise interest rates is the Norges Bank. Norway’s central bank hiked rates back in March for the second time since September and will likely reiterate its plans to tighten policy further later this year. The Norges Bank will announce its policy decision on Thursday and is expected to keep rates unchanged this time. However, any changes to the bank’s projected rate path could cause sharp swings in the Norwegian Krone, particularly against the euro, which has rallied strongly over the past week versus the Nordic currencies.

UK to report Q1 GDP growth

It will be the UK’s turn on Friday to publish GDP data for the first quarter. The British economy is forecast to have expanded by 0.5% quarter-on-quarter in the first three months of the year. With estimates for China, the US and the Eurozone all impressing, a disappointing or a steady UK figure would leave Britain missing out on the growth rebound, with Brexit uncertainty no doubt being the potential culprit.

Friday will be a busy day as apart from the GDP estimates, monthly trade, industrial and manufacturing output numbers will also be published.

A broadly strong set of data would be positive for the pound, especially after Bank of England Governor Mark Carney told reporters this week that markets are under-pricing the chances of a rate hike this year. But unsurprisingly, Brexit could once again steal the show as next week could prove crucial for the government and the Labour party to find a common ground on Brexit in their ongoing talks. If no significant progress is made, the two sides may decide to abandon the talks, killing any hope of a quick end to the Brexit deadlock.

US inflation and Canadian jobs to be North American highlights

A not-so-dovish Fed Chairman lifted the US dollar from its lows this week and the greenback will probably find more support next week from the latest US consumer and producer inflation figures. The PPI numbers are out first on Thursday and the CPI data will be released on Friday. The headline rate of CPI is expected to edge higher from 1.9% to 2.1% y/y in April, while the core rate is also forecast to rise slightly to 2.1%.

Although the Fed pays more attention to the core PCE price index, which has been trending lower, any modest increase in the CPI rate would ease worries of a sustained downtrend in PCE inflation, hence supporting Chairman Powell’s remarks that the current weakness is transitory.

Across the border in Canada, the April employment report will be the loonie’s focal point. The Canadian dollar has seesawed during the past week as the Bank of Canada’s governor, Stephen Poloz, kept rate hike hopes alive in comments to parliament, reversing some of the bearish moves following last week’s dovish BoC meeting. The loonie could recover further if jobs figures on Friday point to a strong labour market.

Signal2forex review

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals