As the summer draws to a close, it will begin to get a little more heated in forex markets as a combination of central bank meetings, key releases and political risks look set to jump start the Autumn trading season. A raft of data out of Australia next week as well as an RBA policy meeting will keep aussie traders glued to their desks, though the Bank of Canada could steal the limelight as it ponders whether to make a dovish pivot. Other highlights will include the US nonfarm payrolls report and the latest Brexit storms brewing up in Westminster. The week might begin on a quiet note however, as North American markets will be closed on Monday for Labor Day.

RBA to stand pat but data could hold key to future policy

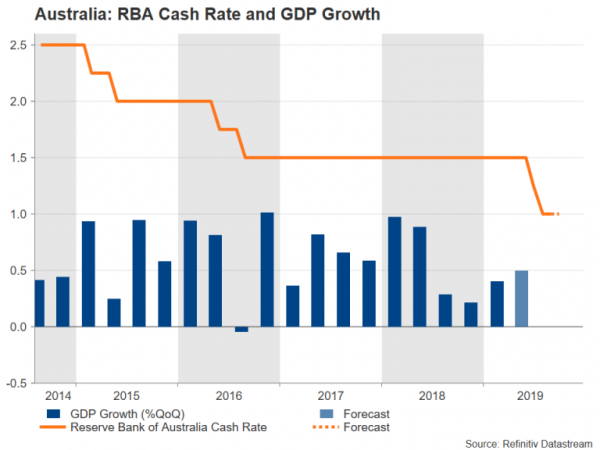

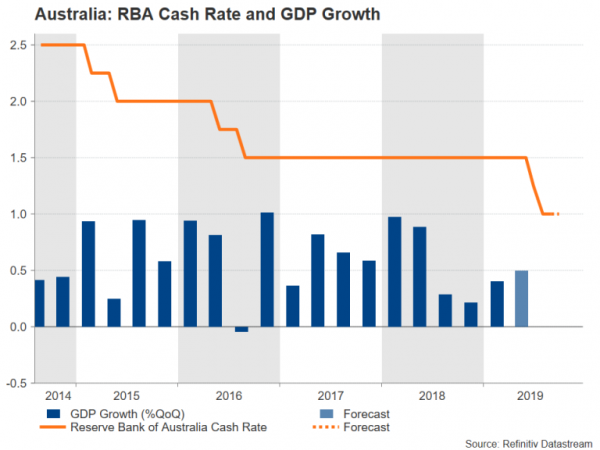

It’s going to be a packed week in Australia, as apart from the RBA’s monthly gathering, a host of economic releases will be watched for clues about the direction of Australian growth. Starting the week, the AIG manufacturing index is out first on Monday before attention turns to second quarter business inventories numbers. They will be followed by Q2 net exports contribution data and retail sales figures for July ahead of the RBA’s decision on Tuesday.

The business inventories and net exports numbers should be a good precursor to Wednesday’s GDP estimate for Q2. Australia’s economy is projected to have expanded by 0.5% on a quarterly basis in the second quarter, gaining speed marginally from the prior three months. The last vital indicator will be Thursday’s trade figures for July, which together with the retail sales data, will provide a somewhat more up-to-date picture of the Australian economy than the Q2 prints.

The upcoming data could prove more crucial for the Australian dollar than the RBA meeting as policymakers are expected to keep interest rates steady in September following two cuts earlier in the summer. Hence, any unexpected weakness in next week’s releases would suggest that another cut is more likely than not in the RBA’s remaining meetings for 2019.

Trade tensions keep aussie and kiwi on slippery slope

Trade headlines are also bound to keep the aussie under the spotlight as well as manufacturing PMIs out of China. The official manufacturing PMI is due over the weekend, while the Caixin/Markit manufacturing gauge is out on Monday. Analysts are forecasting no change in the government’s index but a slight dip in the Caixin/Markit PMI to 49.8 for August. Meanwhile, the aussie is heading back towards its 10-year lows as global recession risks refuse to recede.

Another currency that has been feeling the strain of the trade war is the New Zealand dollar, which slipped to four-year lows this week. Recent economic pointers out of New Zealand have been lacklustre and while investors will have to wait until September 19 to get the full GDP reading for Q2, Monday’s terms of trade report should shed some light as to how the economy performed during the period.

Bank of Canada ready to make dovish turn?

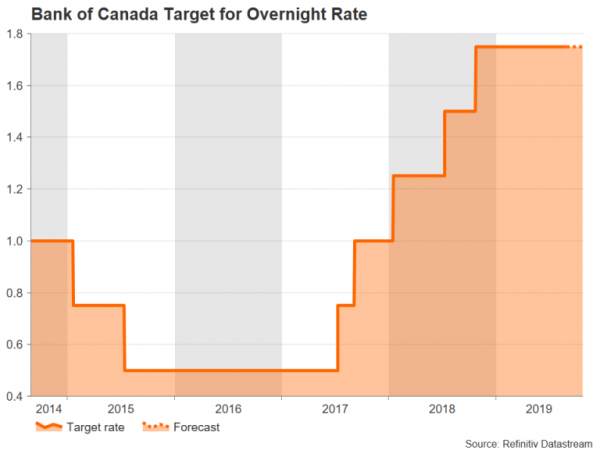

The Bank of Canada will announce its decision one day after the RBA, and although it too is anticipated to leave policy unchanged, the language of its statement will be significant as speculation grows about whether the Bank is on the verge of switching to an easing bias. Also due on Wednesday are July trade figures. PMI surveys on Tuesday and Friday may attract some attention too. But the main data to keep an eye on will be Friday’s employment report. Employment has fallen in the previous two months so another decline in August would raise concerns that the Canadian economy is losing steam.

However, the Canadian dollar will take its cue mostly from the BoC meeting as any hint of a rate cut is likely to place the loonie under renewed pressure against the US dollar.

Euro unlikely to be swayed by Eurozone data

The Eurozone calendar will consist mostly of second tier releases in the lead up to the European Central Bank’s September 12 policy meeting. The incoming data till then will therefore struggle to make much of a mark on the euro. The main releases next week are producer prices on Tuesday, retail sales on Wednesday, and second quarter employment numbers as well as the third estimate of Q2 GDP growth on Friday.

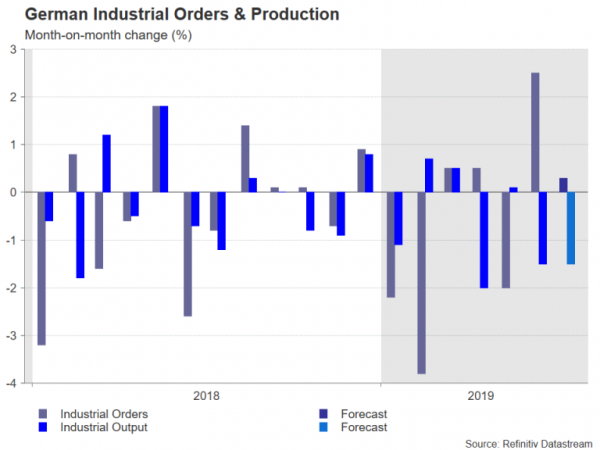

German industrial orders and output figures for July on Thursday and Friday, respectively, will probably generate more interest as fears grow that Europe’s largest economy is already in recession.

The euro has been drifting lower in the past week and is on track to revisit its 2019 low of $1.1025 in anticipation of a major stimulus announcement by the ECB later in September. However, the single currency has been on the up versus the Swedish krona and could extend those gains if the Riksbank drops its tightening bias. Sweden’s central bank, which raised rates for the first time since 2011 in December, is forecast to hold rates at its policy meeting on Thursday but could shift to a more dovish policy stance following the deterioration in the global growth outlook and in response to the expected easing by the ECB.

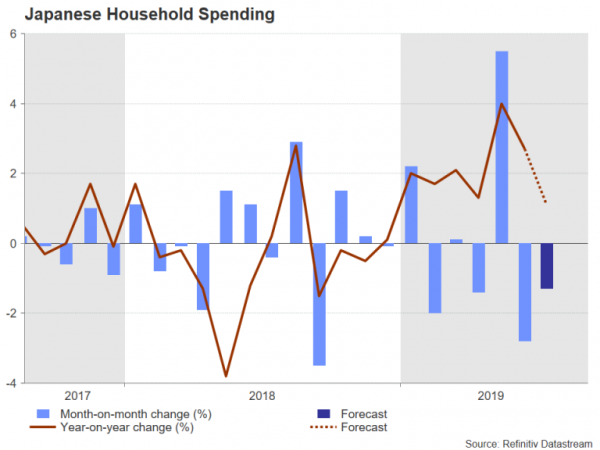

Japanese wage and spending figures to be watched

As growth in many parts of the world has floundered, the sustained economic expansion in Japan has allowed the Bank of Japan to put off a decision on the need for additional stimulus. Signs of divisions within the BoJ board has also left investors sceptical about whether the central bank can deliver a sizeable monetary boost.

One factor that’s kept the Japanese economy from slipping into negative growth is rising household spending. But that trend is at risk from poor wage growth. The latest numbers on household spending and nominal and real earnings are due on Friday. Also important will be the revised estimate of capital expenditure for Q2 on Monday. Typically, the data is expected to have little impact on the yen, which continues to be led mostly by safe-haven flows.

Pound on edge as battle lines drawn in Parliament

British MPs return from their summer recess on September 3 and following the Prime Minister’s controversial decision to prorogue Parliament, all eyes will be on whether the opposition Labour party decides to call a vote of no-confidence in the Johnson government. The chances of Labour going ahead with such a motion are high as Boris Johnson’s attempts to curtail the amount of time MPs will get to legislate a bill blocking a no-deal Brexit before the October 31 deadline has outraged lawmakers from all parties, including Tory Remainers.

If Labour decides against a vote of no-confidence motion, there could still be a cross-party effort to force an extension of the Brexit deadline.

The pound is likely to receive a major boost should the opposition win a no-confidence vote and trigger an election. However, traders should be wary of a big pound rally as Johnson’s recent actions suggest he is also readying for an election and could call one himself if it starts to look like many of his own party’s MPs would join forces with the opposition to block a no-deal Brexit.

In the meantime, economic indicators are likely to continue being side-lined by politics and that includes the UK Markit/CIPS PMIs due next week. The manufacturing, construction and services PMIs for August are out on Monday, Tuesday and Wednesday, respectively.

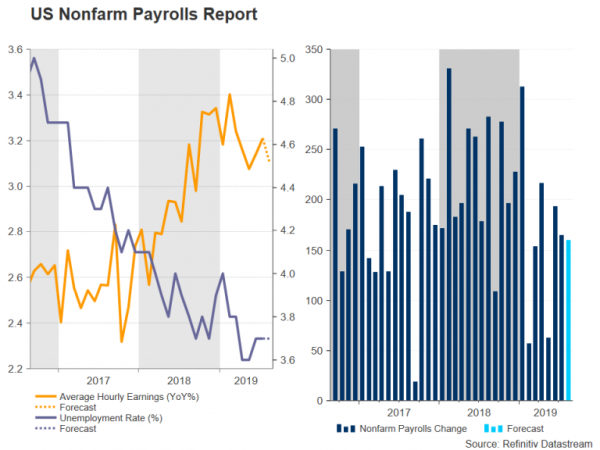

US jobs report in focus as recession fears persist

After Powell & Co disappointed markets at the Jackson Hole symposium by not flagging a more aggressive policy easing, investors will be looking at key gauges of the US economy next week to assess the chances of a further dovish tilt by Fed policymakers. First up on the radar is the ISM manufacturing PMI. The index fell to a near three-year low in July and is forecast to edge lower by another 0.2 points to 51.0 in August. July trade figures will follow on Wednesday before things get into full swing on Thursday.

The ADP employment report will lead the pack, which will also comprise of factory orders and the ISM non-manufacturing PMI. The private survey by ADP – seen as a good guide to Friday’s official jobs numbers – is expected to show a gain of 150k jobs in August, slightly down on July. Factory orders are forecast to have risen for a second straight month in July. But the biggest impact from Thursday’s data could come from the ISM non-manufacturing PMI, which had unexpectedly slumped in July. The non-manufacturing PMI, which makes up the biggest chunk of the US economy, is forecast to inch up to 53.8 in August.

On Friday, investors will be hoping to get more direction from the August jobs report as it could be the deciding factor for some FOMC members in voting for or against a rate cut at the Fed’s September policy meeting. The US labour market is expected to have added 159k jobs in August, signalling that although the pace of job creation has slowed, there’s still plenty of momentum in the economy. The unemployment rate is forecast to stay at 3.7%, while average hourly earnings are projected to have increased by 3.1% year-on-year in August.

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals