Sterling drops sharply today as after poor manufacturing data. Also, political and Brexit uncertainties remain in UK. There are “very strong” rumors that a general election could be called this week that could take place before Brexit date of October 31. Australian Dollar follows as the second weakest for now, then Euro. On the other hand, Dollar rises broadly even though new tariffs between US and China finally took effect over the weekend. Yen is the second strongest as markets turn mixed in quiet trading, with holiday in US and Canada.

Technically, USD/CAD’s break of 1.3345 finally suggests resumption of choppy rise from 1.3016. Further rally could then be seen back to 1.3432/3564 resistance zone. EUR/USD is on track to 1.0683 projection level as medium term down trend extends. 0.6677 support will be a level to watch to confirm Dollar strength. On the other hand, GBP/USD is targeting 1.2014 low and break will resume larger down trend for 1.1946 low. 0.9157 resistance in EUR/GBP and 126.54 in GBP/JPY will need to be broken, though, to confirm underlying selloff in the Pound.

In other markets, currently, FTSE is up 1.30%. DAX is up 0.20%. CAC is up 0.23%. German 10-year yield is up 0.0045 at -0.694. Earlier in Asia, Nikkei dropped -0.41%. Hong Kong HSI dropped -0.38%. China Shanghai SSE rose 1.31%. Singapore Strait Times dropped -0.76%. Japan 10-year JGB yield rose 0.0139 to -0.263.

UK PMI manufacturing dropped to 47.4, 7-year low

UK PMI Manufacturing dropped to 47.4 in August, down from 48.0 and missed expectation of 49.5. That’s also the lowest level in more than 7 years. Markit also noted that new orders contracted as fastest pace in over seven years too. Business confidence dropped to series-record low.

Rob Dobson, Director at IHS Markit said: “High levels of economic and political uncertainty alongside ongoing global trade tensions stifled the performance of UK manufacturers in August. Business conditions deteriorated to the greatest extent in seven years, as companies scaled back production in response to the steepest drop in new order intakes since mid- 2012.

“Based on its historical relationship against official ONS data, the latest PMI Output Index is consistent with a quarterly pace of contraction close to 2%. The outlook also weakened as the multiple headwinds buffeting the sector saw business optimism slump to a series-record low.”

“The current high degree of market uncertainty, both at home and abroad, and currency volatility will need to reduce significantly if UK manufacturing is to make any positive strides towards recovery in the coming months.”

Eurozone PMI manufacturing finalized at 47.0, Germany in steepest decline, Franc bucks the trend

Eurozone PMI Manufacturing was finalized at 47.0 in August, unrevised. That was slightly higher than July’s final reading of 46.5. Markit noted that production and new orders continued to fall as confidence hits lowest since November 2012. Also, employment declined for the fourth month running during August.

Among the states, improvement were generally seen but readings stayed dismal. Germany was revised slightly lower to 43.5, well below 50. Australia was at 48.6. Italy was at 48.7. Spain was at 48.8. Ireland even fell to 76-month low at 48.6. France (51.1), the Netherlands (51.6) and Greece (54.9) were the brighter spots.

Chris Williamson, Chief Business Economist at IHS Markit said: “Eurozone producers are suffering as the summer slump in factory production persisted into August. Although up on July, August’s manufacturing PMI was the second-lowest since early 2013, and a marked deterioration in optimism about the year ahead suggests companies are expecting worse to come.”

“Trade wars and tariffs remain the biggest concerns among producers, and the escalation of global trade war tensions in August encouraged further risk aversion… “Germany is suffering the steepest decline, in part reflecting slumping global demand for autos and business machinery. While France bucked a wider downturn trend, even here growth was only very modest.”

Also released, Swiss retail sales rose 1.4% yoy in July, above expectation of 0.9% yoy. Swiss PMI Manufacturing rose 0.2 to 48.7, slightly above expectation of 48.6.

China Caixin PMI Manufacturing rose to 50.4, but overall demand didn’t improve

China Caixin PMI Manufacturing rose to 50.4 in August, up from 49.9 and beat expectation of 49.8. Caixin note marginal expansion of output. New orders were broadly stable despite further decline in export sales. However, output charges fell at quickest rate since December 2015.

Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “China’s manufacturing sector showed a recovery in August, mainly due to improved production activity. However, overall demand didn’t improve, and foreign demand declined notably, leading product inventories to grow. There was no sign of an improvement in companies’ willingness to replenish inventories of inputs or in their confidence. Industrial prices trended down. China’s economy showed signs of a short-term recovery, but downward pressure remains a long-term problem. Amid unstable Sino-American relations, China needs to step up countercyclical policies.”

Japan PMI manufacturing finalized at 49.3, difficult to envisage any near-term improvements

Japan PMI Manufacturing was finalized at 49.3 in August, revised down from 49.5, slightly down from July’s 49.3. Markit noted sluggish demand conditions persisted in August. Output continued to decline while business confidence was subdued. Also, firmed reduced output charges to stimulate sales.

Joe Hayes, Economist at IHS Markit, said Japanese goods producers continued to “signal difficult conditions during August”, reflecting the broader regional tone within the APAC manufacturing economy. Softer growth across Asia, particularly in China, was reported to have dented export opportunities. Also, “escalation of tensions with Korea merely adds extra downside risk to an already fragile environment.:” “With external and domestic headwinds aplenty, it is difficult to envisage any near-term improvements in Japan’s manufacturing sector.”

Also from Japan, capital spending rose 1.9% in Q2, above expectation of 1.9%.

Australia AiG PMI rose to 53.1, manufacturing conditions improved

Australia AiG Performance of Manufacturing Index rose to 53.1 in August, up from 51.3. AiG noted that “manufacturing conditions improved in August, with increasing levels of production and rising exports”. And “overseas demand for Australian manufactured products remains strong, particularly for consumable manufacturing products.”

Also from Australia, TD securities inflation rose 0.0% mom in August. Company operating profits rose 4.5% qoq in Q2, much higher than expectation of 1.7% qoq.

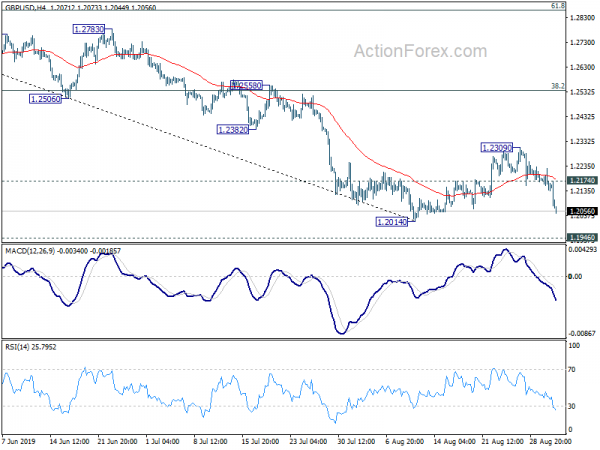

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2129; (P) 1.2178; (R1) 1.2215; More….

GBP/USD’s fall from 1.2309 extends further today. Intraday bias remains on the downside for 1.2014 support. Break will resume larger down trend to 1.1946 low next. On the upside, above 1.2174 minor resistance will turn intraday bias neutral again. IN case of another rise as consolidation from 1.2014 extends, upside should be limited by 38.2% retracement of 1.3381 to 1.2014 at 1.2536 to bring down trend resumption eventually.

In the bigger picture, down trend from 1.4376 (2018 high) is extending towards 1.1946 low. We’d be cautious on bottoming there. But decisive break will resume down trend from 2.1161 (2007 high) to 61.8% projection of 1.7190 to 1.1946 from 1.4376 at 1.1135. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Aug | 53.1 | 51.3 | ||

| 22:45 | NZD | Terms of Trade Index Q/Q Q2 | 1.60% | 1.00% | 1.00% | |

| 23:50 | JPY | Capital Spending Q2 | 1.90% | 1.80% | 6.10% | |

| 0:30 | JPY | PMI Manufacturing Aug F | 49.3 | 49.5 | 49.5 | |

| 1:00 | AUD | TD Securities Inflation M/M Aug | 0.00% | 0.30% | ||

| 1:30 | AUD | Company Operating Profit Q/Q Q2 | 4.50% | 2.10% | 1.70% | |

| 1:45 | CNY | Caixin PMI Manufacturing Aug | 50.4 | 49.8 | 49.9 | |

| 6:30 | CHF | Retail Sales Real Y/Y Jul | 1.40% | 0.90% | 0.70% | |

| 7:30 | CHF | PMI Manufacturing Aug | 47.2 | 45.7 | 44.7 | |

| 7:45 | EUR | Italy Manufacturing PMI Aug | 48.7 | 48.6 | 48.5 | |

| 7:50 | EUR | France Manufacturing PMI Aug F | 51.1 | 51 | 51 | |

| 7:55 | EUR | Germany Manufacturing PMI Aug F | 43.5 | 43.6 | 43.6 | |

| 8:00 | EUR | Eurozone Manufacturing PMI Aug F | 47 | 47 | 47 | |

| 8:30 | GBP | PMI Manufacturing Aug | 47.4 | 49.5 | 48 |

Signal2forex.com - Best Forex robots and signals

Signal2forex.com - Best Forex robots and signals